Recent data from the Insurance Council of Texas indicates that approximately 8.3% of Texas motorists are entirely uninsured, a figure that often spikes in high-density corridors like Houston and Dallas. You probably understand that riding in a major Texas metro area requires more than just mechanical skill; it demands a calculated approach to risk management. High premiums in Harris County and the technical nuances of guest passenger liability laws can make securing the right motorcycle insurance feel like an unnecessary burden on your time and resources.

We've designed this 2026 guide to provide the professional clarity you need to master Texas legal requirements while ensuring your financial stability remains intact. You'll learn how to secure comprehensive protection that guards against theft and underinsured drivers on busy interstate highways. We'll analyze mandatory liability limits, evaluate the practical necessity of personal injury protection, and offer expert strategies to optimize your coverage costs without sacrificing safety.

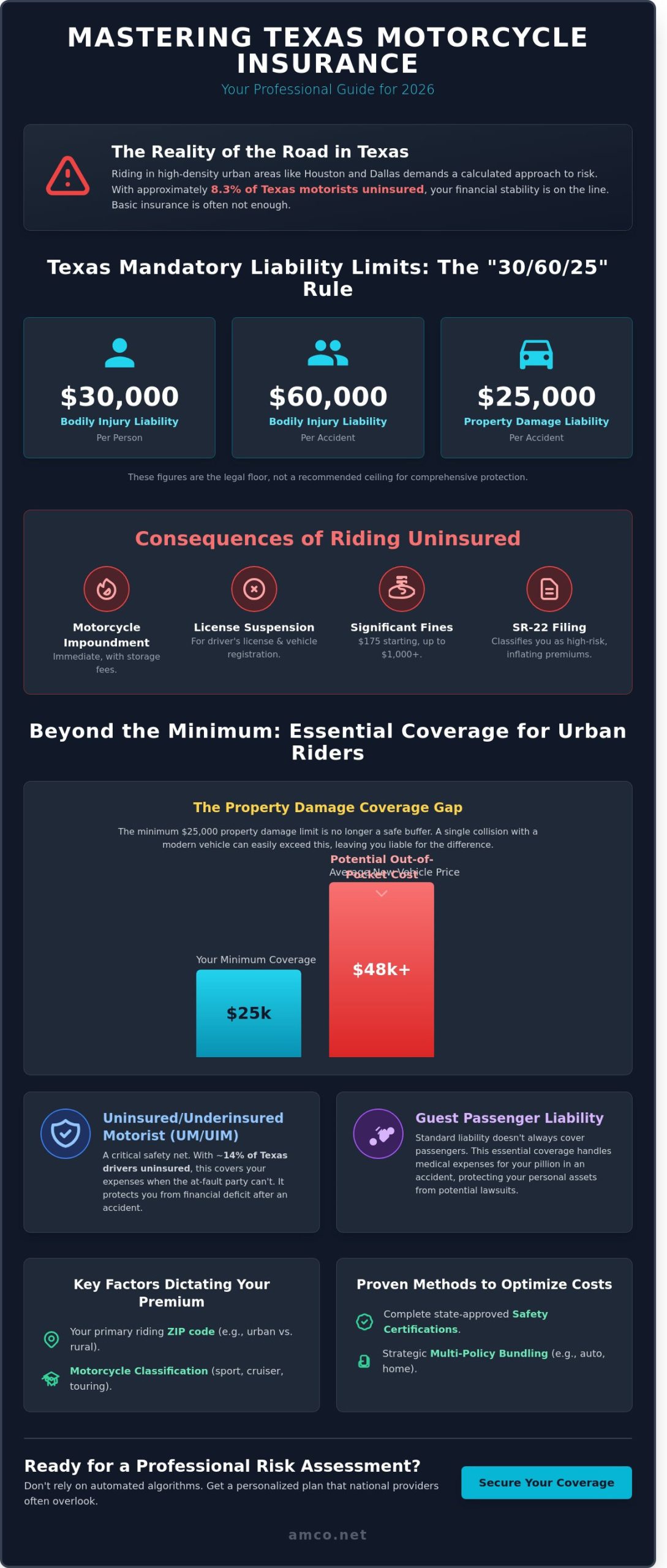

In Texas, vehicle insurance operates as a rigid financial contract that transfers the burden of liability from the rider to the insurance provider. For the 2026 calendar year, the state continues to enforce the 30/60/25 minimum liability limits. This specific framework requires your Motorcycle Insurance policy to cover $30,000 for bodily injury per person, $60,000 for total bodily injury per incident, and $25,000 for property damage. These figures represent the absolute floor of legal compliance, not a recommended ceiling for comprehensive protection.

While these minimums satisfy the law, they're often insufficient for the realities of riding in Houston. The city's high traffic density and the rising cost of vehicle repairs mean that a single incident can quickly exhaust basic policy limits. If your coverage is capped at $25,000 and you're involved in a collision with a modern SUV, you'll likely face out-of-pocket expenses for the remaining balance. The Texas Department of Insurance (TDI) has moved toward stricter real-time monitoring in 2026, ensuring that any lapse in coverage is identified almost immediately through the TexasSure database.

Operating a motorcycle without the required coverage leads to significant legal and financial friction. Penalties for riding uninsured in Texas include:

Bodily injury liability is your primary defense against third-party claims. It covers medical bills, rehabilitation costs, and lost income for others if you're found at fault. Property damage liability covers the cost of repairing or replacing vehicles and stationary objects like fences or storefronts. In 2026, the cost-optimization of your Motorcycle Insurance should focus on increasing these limits. A $25,000 property damage limit is no longer a safe buffer when the average price of a new vehicle in the United States stays above $48,000. Higher limits provide the long-term stability needed to protect your personal assets from litigation. For a broader perspective on managing all your coverage needs in the region, our comprehensive guide to insurance in Houston outlines the 2026 landscape for personal and commercial policies alike.

Texas law maintains a specific distinction between the rider and the passenger. Many riders assume that standard liability covers everyone on the bike, but this isn't always the case. You must verify that your policy includes guest passenger liability. This coverage is essential if you carry a pillion, as it handles the medical expenses for your passenger if an accident occurs. Without this specific election, a passenger could legally pursue your personal assets to cover their medical recovery. Integrating this into your overall strategy ensures your risk management is thorough and professional.

The legal minimum liability requirements in Texas serve as a baseline, but they rarely provide the technical depth needed for high-traffic environments like Houston, Dallas, or San Antonio. Urban riding involves navigating complex intersections and high-speed tollways where the margin for error is slim. Relying solely on basic 30/60/25 coverage leaves significant financial gaps, especially when considering the rising costs of medical care and specialized mechanical repairs. Establishing a robust Motorcycle Insurance portfolio requires a methodical assessment of regional risks, from heavy congestion to unpredictable environmental factors.

Data from the Insurance Research Council suggests that approximately 14% of Texas drivers operate vehicles without any insurance coverage. In densely populated metro areas, this percentage can fluctuate, increasing the risk of a financial deficit following an accident. Uninsured/Underinsured Motorist (UM/UIM) coverage is a critical component of risk mitigation for any serious rider. It functions as a secondary layer of protection that activates when the at-fault party lacks the policy limits to cover your damages. Analyzing NHTSA motorcycle safety data reveals that multi-vehicle collisions in urban settings often result in significant medical expenses that quickly exceed minimum liability thresholds. UM/UIM also provides essential protection in hit-and-run scenarios, which occur frequently in congested city centers where drivers might flee the scene to avoid accountability.

Distinguishing between Personal Injury Protection (PIP) and Medical Payments (MedPay) is another vital step in policy optimization. Texas law requires insurers to offer PIP, which covers not only medical bills but also 80% of lost wages and the cost of essential services you can't perform due to injury. MedPay is more restrictive, focusing solely on direct medical costs. For professionals who rely on their physical presence for income, PIP offers a more thorough level of financial continuity. Choosing the right Motorcycle Insurance involves more than comparing premiums; it requires a calculated look at how different coverage layers interact to secure your financial future on the road. Texas riders who also own recreational vehicles should be aware that similar coverage gaps exist for larger assets, making it equally important to review your RV Insurance policy to ensure your motorhome or towable is fully protected against weather events and liability risks.

Determining the cost of Motorcycle Insurance involves a precise analysis of technical and behavioral variables. Insurance providers utilize actuarial data to establish a baseline risk profile for every policyholder. This process isn't arbitrary; it relies on historical data points that correlate specific rider behaviors and vehicle types with the probability of a claim. In the Texas market, where environmental factors and infrastructure vary significantly between regions, these calculations become increasingly complex. Riders seeking a full picture of how rising premiums affect all policy types in the region will find valuable context in this detailed overview of insurance houston trends heading into 2026.

Your primary riding location serves as the most significant baseline for your premium. Actuarial tables reveal stark contrasts between Texas metropolitan areas. Houston's high volume of registered vehicles on the I-10 and 610 Loop increases collision probability compared to rural ZIP codes. Midland's industrial routes involve heavy machinery and commercial traffic, presenting unique environmental hazards that differ from the congested residential streets of San Antonio.

Experience level remains a primary metric for risk assessment. A 40-year-old rider with a decade of documented experience generally pays less than a 19-year-old novice, as 2024 safety data indicates that newer riders have a higher frequency of single-vehicle incidents. Your Texas driving record, including speeding citations or non-motorcycle related infractions, also impacts your eligibility for preferred rates.

Usage patterns further refine the quote. Daily commuting through Dallas traffic involves repetitive exposure to peak-hour risks and higher annual mileage. Conversely, weekend riding in the Texas Hill Country usually results in fewer hours on the road, which can lead to lower premiums. Insurers look for consistency and safety, rewarding riders who maintain a clean record and utilize their vehicles in lower-risk environments.

Reducing the total cost of Motorcycle Insurance requires a methodical approach to risk management and policy optimization. In the 2026 Texas market, premiums are influenced by a rider's proactive steps toward safety and asset protection. Completing a Texas-approved motorcycle safety course is one of the most effective ways to secure a lower rate. Most carriers offer a 10% discount on liability and collision coverage for riders who present a certificate from a course approved by the Texas Department of Public Safety. This initial investment in education typically pays for itself through premium savings within the first twelve months.

Professional training remains a cornerstone of long-term cost control. Riders located in College Station and Odessa have access to several MSF-approved training centers that provide the necessary certification for premium credits. Obtaining a formal motorcycle endorsement on your Texas license is not just a legal requirement; it is a signal to insurers that you meet the state's rigorous safety standards. Investing in advanced rider training offers a high ROI by reducing the statistical likelihood of accidents, which keeps your Motorcycle Insurance rates stable over the long term. Data from safety organizations indicates that riders with formal training have significantly fewer claims than self-taught operators.

Optimizing your policy involves more than just finding the lowest price; it requires a strategic alignment of coverage and discounts. Contact our expert advisors today to review your current policy and identify every available saving for the 2026 riding season.

Selecting Motorcycle Insurance requires more than a digital transaction; it demands an understanding of the specific risks present on Texas roadways. National brands often rely on generalized algorithms that fail to account for the unique traffic density of the I-10 corridor or the seasonal weather patterns in the Gulf Coast region. AMCO has operated within the Texas market for over 35 years, providing a level of stability and technical expertise that automated systems cannot replicate. Since 1987, our firm has focused on delivering reliable risk management solutions that prioritize the rider's long-term financial health.

The core advantage of the brokerage model lies in its flexibility. AMCO identifies the optimal fit for your specific riding profile by comparing established Texas carriers. This process eliminates the limitations of captive agencies that only offer a single suite of products. Our team manages the technical details of policy integration, ensuring that your coverage complies with current Texas laws regarding liability and medical payments. We don't just sell a policy; we build a protective framework tailored to your assets.

Our consultants act as intermediaries between you and the insurance carrier. If a claim arises, you speak with a professional who understands the local environment, not a call center operative in a different time zone. This local presence serves as a critical fail-safe for your financial security and provides peace of mind that national algorithms can't offer.

To provide an accurate Texas quote, we require specific technical data. You should have your Vehicle Identification Number (VIN), proof of any advanced rider safety courses completed within the last 36 months, and your primary storage zip code ready for review. These details allow us to apply all eligible discounts for mature riders or multi-policy holders immediately. Transitioning from research to active protection is a straightforward process when guided by a specialist who understands the 2026 market requirements. Comprehensive Motorcycle Insurance is the primary mechanism for preserving your personal assets against the unpredictable variables of the open road.

Navigating the evolving landscape of Texas roads requires more than just meeting basic legal mandates. As urban density in major hubs continues to rise, selecting comprehensive coverage that accounts for high-traffic risks is a strategic necessity for your long-term financial security. Since 1987, AMCO has provided riders with technical advice to optimize their policies for both performance and cost. We operate local offices in Houston, Dallas, and San Antonio, ensuring you have access to regional expertise that national providers often overlook. As an A+ rated independent agency, we represent top-tier carriers to identify the specific safety and storage discounts you qualify for today. Protecting your investment with the right Motorcycle Insurance ensures you can focus on the open road instead of potential liabilities. Our team leverages decades of industry experience to help you navigate 2026 requirements with precision and professional insight. It's time to ensure your policy matches the demands of the modern Texas environment.

Get a Professional Motorcycle Insurance Quote from AMCO Today

Ride with the confidence that comes from having a stable, experienced partner protecting every mile of your journey.

Yes, Texas law requires all riders to carry liability insurance under the Texas Transportation Code § 601.051. You're required to maintain minimum coverage limits of $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. Operating a motorcycle without proof of financial responsibility results in fines between $175 and $350 for a first offense.

Monthly costs for motorcycle insurance in Houston vary based on your profile, but the 2024 Texas average for full coverage is approximately $58 per month. High-traffic urban areas like Harris County often see rates 10% higher than the state average due to increased accident density. Your specific premium depends on your age, driving record, and the displacement of your bike's engine.

No, your standard Texas auto policy doesn't provide any coverage while you're operating a motorcycle. Most personal auto insurance contracts contain specific exclusions for two-wheeled vehicles. You must secure a dedicated motorcycle insurance policy to ensure you're legally compliant and protected against liability claims while riding on public roadways.

Texas law requires you to carry guest passenger liability insurance if your motorcycle is equipped with a seat for an additional rider. This coverage protects you if a passenger is injured in an accident where you're at fault. While some policies include this automatically, others require a specific endorsement to meet the legal standards set by the Texas Department of Insurance.

Yes, completing a Texas Department of Public Safety approved safety course typically qualifies you for a 10% premium discount. Most major insurers apply this discount for three years following the completion of the Basic RiderCourse. In cities like Dallas, where traffic complexity is high, these certifications serve as empirical evidence of risk mitigation for insurance underwriters.

You won't receive any compensation from your insurer if your bike is stolen and you only carry liability coverage. Liability insurance only pays for damages or injuries you cause to third parties. According to 2023 National Insurance Crime Bureau data, San Antonio ranks high for vehicle thefts; therefore, adding comprehensive coverage is a necessary technical step to protect your asset.

Yes, Texas requires insurance for any scooter or moped that is operated on public roadways. If the vehicle has an engine displacement exceeding 50cc or travels faster than 30 miles per hour, it falls under the same financial responsibility requirements as a standard motorcycle. You'll need to provide proof of insurance to register the vehicle with the Texas Department of Motor Vehicles.

You can add a motorcycle to your portfolio by contacting an AMCO advisor to initiate a policy endorsement. Our process involves a technical review of your bike's specifications and your existing coverage limits to ensure a seamless integration. This consolidated approach simplifies your administrative overhead and may qualify your account for multi-policy bundling advantages based on our current underwriting guidelines.