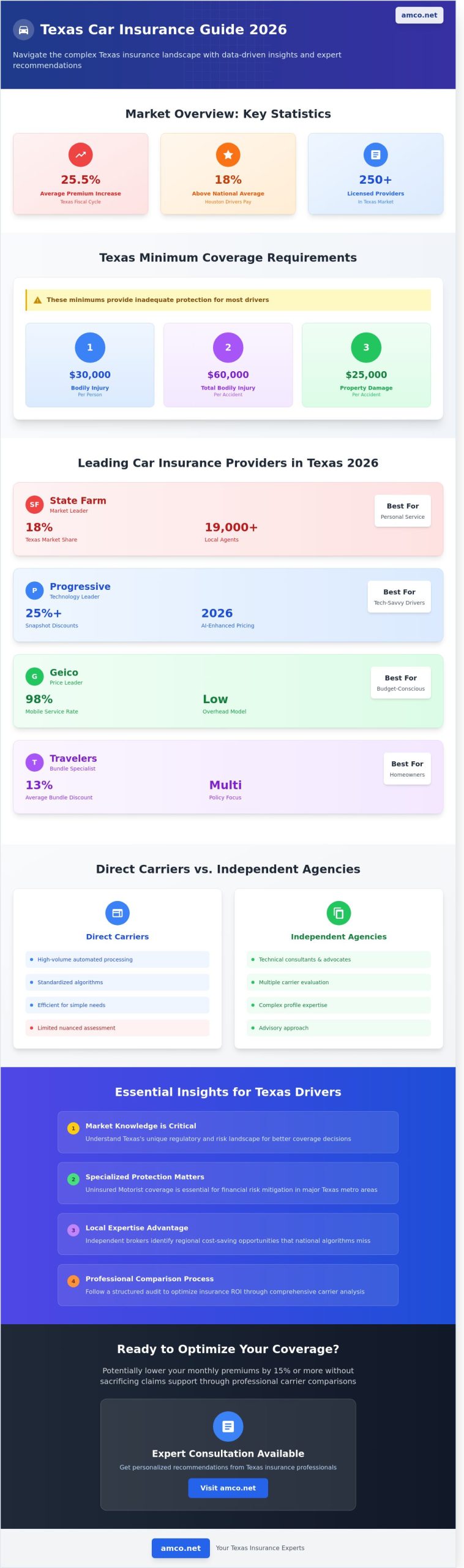

Did you know that Texas drivers faced an average premium increase of 25.5% over the last fiscal cycle, according to recent industry reports? In Houston, motorists are currently paying 18% more than the national average, making the search for reliable car insurance providers a critical financial priority for 2026. You're likely tired of seeing "cheap" online quotes that suddenly double once you reach the final payment screen. It's frustrating to navigate confusing policy jargon when your primary goal is simply securing your vehicle and your savings.

We're here to provide clarity through a data-driven comparison of the leading carriers serving the Lone Star State. This guide will show you how to identify the best car insurance providers for your specific needs, helping you potentially lower your monthly premiums by 15% or more without sacrificing claims support. We'll analyze the top performers in the Texas market and provide a professional framework for evaluating coverage options so you can make an informed, cost-effective decision.

In the insurance industry, car insurance providers are the carriers that underwrite your specific risk and maintain the capital reserves necessary to pay out claims. These entities aren't merely billing platforms; they're the financial backbones of your road safety strategy. The Texas market remains one of the most complex in the United States due to its size and diverse environmental risks. According to the Texas Department of Insurance (TDI) 2023 annual report, there are over 250 companies licensed to provide private passenger auto insurance in the state, creating a highly competitive but often confusing environment for consumers.

The TDI plays a critical role in regulating these car insurance providers, ensuring they remain solvent and follow fair claims practices. Regulation is vital because Texas drivers face unique variables, from Gulf Coast hurricanes to West Texas hailstorms. Location significantly impacts your overhead. Data from 2024 indicates that drivers in Houston and San Antonio pay approximately 18% more for premiums than those in rural areas like Brewster County. This discrepancy stems from higher population density, increased accident frequency on major arteries, and elevated rates of vehicle theft in urban centers.

Direct-to-consumer giants like Geico and Progressive focus on high-volume, automated transactions. They use standardized algorithms to process thousands of applications daily. While efficient for simple needs, this model often lacks the nuanced risk assessment required for complex profiles. Independent agencies like AMCO.NET serve as technical consultants and advocates. Instead of representing a single brand, they evaluate multiple car insurance providers to find a solution that balances cost-efficiency with comprehensive protection. This advisory approach ensures that your coverage evolves alongside your assets, providing a level of stability that automated call centers rarely match.

Texas law operates under the 30/60/25 rule for liability coverage. This translates to the following mandatory minimums:

Relying on these minimums is a significant financial risk for anyone commuting on the I-10 or the 610 Loop. A 2025 mid-sized SUV can easily cost over $45,000, meaning a standard 30/60/25 policy wouldn't even cover the replacement of a single vehicle in a multi-car collision. Professional risk management suggests significantly higher limits to protect personal assets from litigation. In the context of Texas road hazards, full coverage is a strategic combination of liability, collision, and comprehensive insurance that protects the policyholder against both traffic accidents and environmental events like flash flooding or hailstorms.

Selecting from the available car insurance providers in 2026 requires a balance between financial stability and regional service capabilities. State Farm continues to lead the Texas market with a 18% market share, supported by a network of over 19,000 agents. This massive physical presence allows for a personalized advisory approach that digital-only platforms cannot replicate. For Houston residents, having a local agent who understands the specific flood risks and urban traffic patterns of the Gulf Coast provides a layer of security that goes beyond a standard policy document.

Progressive remains the primary choice for drivers who prioritize technological integration. Their "Name Your Price" tool has evolved by 2026 to incorporate real-time economic data, allowing users to adjust coverage limits dynamically. Their Snapshot telematics program now uses advanced sensor data to reward safe driving with discounts that often exceed 25% for low-risk operators. This data-centric model appeals to the modern driver looking for transparency in how their premiums are calculated.

Geico maintains its position as a price leader by utilizing a low-overhead, direct-to-consumer model. While they lack the extensive local office support found with State Farm, their mobile platform handles 98% of routine service requests. For drivers in 2026 who prefer self-service, Geico offers some of the most competitive rates in the Houston metro area. Travelers serves as a strategic option for established households, offering bundling discounts that average 13% when auto policies are combined with homeowners or umbrella coverage. This focus on multi-policy synergy makes them a reliable partner for long-term asset protection.

The 2025 J.D. Power U.S. Auto Insurance Study indicates that top-tier car insurance providers in the Texas region now achieve an average satisfaction score of 847 out of 1,000. Financial stability is equally critical; an AM Best rating of A++ or A+ confirms a carrier's capacity to pay out claims even after large-scale regional disasters. In 2026, mobile app functionality has become a primary differentiator, with top-rated apps now offering integrated roadside assistance and instant digital claim filing with 3D damage estimation. Evaluating these metrics ensures your chosen provider offers comprehensive solutions for your long-term protection needs.

Texas drivers requiring SR-22 filings or those with non-standard insurance needs often find the best terms through Progressive or specialized carriers like Dairyland. These providers offer streamlined digital filing with the Texas Department of Public Safety, often completing the process within 24 hours. For individuals using personal vehicles for gig work, bridging the gap between personal and commercial coverage is essential. Many 2026 policies now include "hired and non-owned" endorsements to protect drivers during delivery or rideshare gaps, ensuring no lapse in liability during professional use.

Selecting the right policy requires a technical analysis of how specific coverages mitigate local risks. In Texas, data from the Texas Department of Insurance indicates that approximately 14% of drivers operate without any coverage. This reality makes Uninsured/Underinsured Motorist (UM/UIM) protection a non-negotiable component for any driver in Houston. Professional car insurance providers focus on these high-risk variables, ensuring that a policyholder's financial stability isn't compromised by another driver's lack of compliance or financial means.

Efficiency in 2026 is defined by AI-integrated claims processing. Leading car insurance providers now use computer vision to analyze damage photos, often providing repair estimates within 120 minutes. Telematics programs have matured, offering discounts up to 30% for safe driving habits. While these programs provide significant savings, they require a transparent exchange of data that some users find intrusive. Most claims are now settled via direct deposit, which has reduced the average payout timeline from seven days to just 48 hours for approved repairs.

The math behind multi-line discounts shows a clear path to economic efficiency. Policyholders who combine their auto coverage with Renters Insurance or homeowners policies save an average of 22% annually. Local agencies offer more flexibility than single-carrier captive agents because they can pivot between providers to maintain these discounts as market rates fluctuate. This localized expertise is particularly valuable in Houston, where neighborhood-specific flood risks require precise policy adjustments to ensure full protection and long-term reliability.

Many drivers believe purchasing a policy directly from national car insurance providers saves money by removing intermediary fees. This assumption frequently leads to higher premiums. Insurance carriers often provide independent brokers with access to wholesale rates or regional discounts that aren't visible on public-facing websites. Brokers act as consultants who analyze your specific risk profile against dozens of carrier algorithms simultaneously.

AMCO.NET has operated in Houston since 1987. This 37-year history creates a "risk-radar" that generic online tools lack. We understand how local factors, such as the 2024 flood map updates or the high-theft rates in specific Harris County zip codes, affect your premiums. A broker provides a single point of contact for your entire portfolio, ensuring your personal vehicles and business assets have seamless coverage without expensive overlaps. Understanding why local auto insurance expertise beats online apps in 2026 becomes crucial when automated systems fail to account for Houston's unique Gulf Coast weather patterns and regional risk factors. When searching for an insurance company near me with specialized Texas expertise, the difference between generic national algorithms and local market knowledge becomes evident in both premium costs and claims handling efficiency.

Texas drivers facing a suspended license must follow a precise legal protocol to regain their driving privileges. First, you must secure a policy that meets the state's minimum liability requirements. Second, you must request that your carrier files an SR-22 form with the Texas Department of Public Safety. An SR-22 is a certificate of financial responsibility, not a type of insurance.

Houston's status as a global shipping hub means many residents are also owner-operators. Standard car insurance providers typically exclude vehicles used for commercial hauling, leaving drivers vulnerable during a claim. If you operate near the Port of Houston or the I-10 corridor, your risk profile is fundamentally different from a standard commuter. Professional drivers require specialized Commercial Trucking Insurance Houston solutions that cover cargo, liability, and physical damage under one commercial umbrella. This separation protects your personal assets if a business-related accident occurs. For fleet operators managing multiple vehicles, evaluating the top trucking insurance companies for Texas fleets ensures access to A-rated carriers that understand the state's unique regulatory environment and provide the local expertise needed to optimize long-term costs.

Don't settle for a generic algorithm's estimate. Contact our Houston experts today for a comprehensive policy review that identifies every available regional discount.

Selecting the right coverage among various car insurance providers in the Houston market requires a systematic approach to risk management. It isn't just about finding the lowest premium. It's about ensuring long-term financial continuity and asset protection. At AMCO, we treat your personal insurance with the same technical rigor as a commercial contract. Our methodology follows a five step process designed to eliminate coverage gaps and optimize your annual spend.

We utilize proprietary software to scan the Texas insurance market, filtering through dozens of car insurance providers in under three minutes. This technological advantage ensures we capture real-time rate fluctuations. Our selection criteria remain rigorous; we actively reject insurers with claims to settlement ratios falling below 85% or those with consistent negative feedback regarding litigation delays. Transparency is our priority. If a smaller, regional carrier offers superior terms over a household name, we provide the data to prove why they're the better choice for your specific profile.

Efficiency is critical in 2026. You can initiate a quote via our mobile application or website in approximately five minutes. However, the initial purchase is only the beginning of our partnership. Market volatility in the Houston metro area makes a "Policy Check-Up" every 12 months essential. Rates in Harris County fluctuated by 14% between 2024 and 2025. A policy that was competitive last year might no longer serve your financial interests today. We monitor these shifts so you don't have to.

Navigating the 2026 landscape of car insurance providers requires more than a surface-level search. You need a partner who understands the specific risks of Houston's infrastructure and the evolving regulatory environment in Texas. Since 1987, AMCO has provided this stability by connecting drivers with dozens of top-rated carriers. Our approach focuses on long-term cost optimization rather than temporary fixes. We ensure you aren't just buying a policy; you're securing a comprehensive risk management solution tailored to your specific vehicle and driving history.

Our local Houston office provides bilingual support to ensure every technical detail remains clear. Whether you're comparing national giants or specialized regional firms, our 39 years of market experience serves as your primary advantage. Efficiency and reliability aren't just goals for us. They're the standards we've maintained since our founding. You deserve a strategy that balances premium costs with robust protection. We're here to facilitate that transition with precision and professional integrity.

Get a Personalized Quote from Multiple Providers Now

Take the next step toward a more secure and cost-effective driving experience today.

State Farm currently ranks as the leading choice for Houston motorists due to its 18% market share and extensive network of local agents. While Geico offers competitive digital platforms, State Farm's physical presence in Harris County provides a measurable advantage for claims processing speed. Recent 2025 JD Power surveys indicate a regional satisfaction score of 882 out of 1,000 for their Texas operations.

Yes, you can obtain coverage with an SR-22 requirement through specialized car insurance providers like Progressive or Dairyland. These companies electronically file the Form SR-22 with the Texas Department of Public Safety to certify your financial responsibility. Expect premiums to increase by an average of 45% compared to standard policies because of the high-risk designation attached to your driving record.

Buying through an insurance broker is typically more cost-effective for complex risk profiles because they compare 15 to 20 different carriers simultaneously. Direct purchases from a provider's website might save the 10% to 15% commission fee but often limit your options to a single brand's underwriting criteria. Data shows that 62% of Texas drivers find better long-term value through independent agents who manage annual renewals.

Texas law for 2026 requires 30/60/25 liability coverage limits. This means your policy must provide $30,000 for each injured person, $60,000 total per accident, and $25,000 for property damage. Drivers failing to maintain these specific thresholds face fines up to $350 for a first offense and potential vehicle impoundment under the Texas Financial Responsibility Act.

San Antonio drivers pay an average of $1,840 annually, while Dallas motorists face higher premiums averaging $2,150 per year. This $310 difference stems from higher theft rates and traffic density statistics recorded in the DFW metroplex. Actuarial data from the Texas Department of Insurance suggests that Dallas zip codes carry a 14% higher risk profile than those in Bexar County.

The Texas Property and Casualty Insurance Guaranty Association (TPCIGA) protects policyholders if a licensed insurer becomes insolvent. This state-mandated entity covers outstanding claims up to $300,000 per policy and refunds unearned premiums up to $25,000. It ensures that your legal and financial protection remains intact even during a corporate bankruptcy or liquidation process.

Most car insurance providers allow you to bundle commercial truck insurance with personal policies through a multi-policy discount program. Combining these coverages under one carrier like Travelers or Liberty Mutual often results in a 12% reduction in total premium costs. This structured approach simplifies administrative oversight and ensures there aren't gaps between business and personal liability limits.

You switch providers by securing a new policy with an effective date that matches your current policy's expiration date exactly. Always receive a written confirmation of the new coverage before sending a formal cancellation notice to your previous insurer. A single day of lapsed coverage can trigger a 15% premium hike in future years and lead to a $175 administrative penalty from the state. For a comprehensive walkthrough of how to evaluate and transition to a better auto insurance company in Houston and Texas, reviewing the key metrics for claims-processing efficiency and local risk assessment can help ensure you make the most informed decision possible.