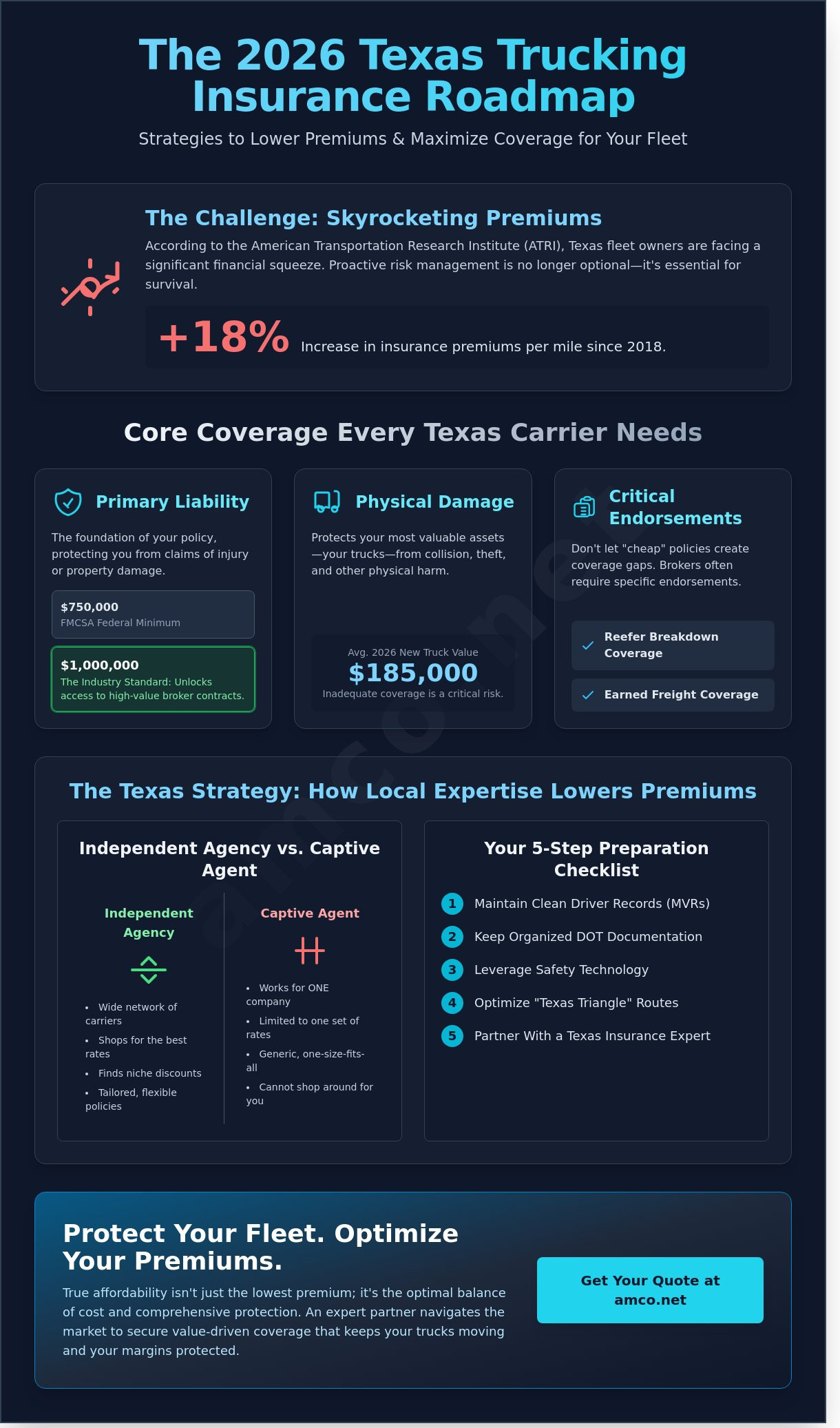

According to the American Transportation Research Institute (ATRI) 2023 report, insurance premiums per mile have increased by over 18% since 2018. For Texas fleet owners, this data confirms what you already feel every time you review your quarterly profit and loss statements. You know that maintaining a lean operation is impossible when fixed costs like coverage keep climbing, yet you can't afford the risk of a budget policy that fails to provide a valid certificate of insurance (COI) when a high-value broker demands it.

This guide provides a professional roadmap to securing affordable trucking insurance that satisfies both your bottom line and your legal obligations. We'll show you how to optimize your risk profile to access the most competitive rates in the Houston market without compromising on the critical protections your drivers need. You'll learn our specific 2026 framework for managing Texas-specific filings and streamlining digital documentation to keep your trucks moving and your margins protected. By applying these expert strategies, you can ensure your fleet remains compliant and fully covered while eliminating the waste that typically inflates commercial premiums.

In the 2026 Texas logistics sector, securing affordable trucking insurance requires a shift from simple price-chasing to strategic risk management. True affordability represents the optimal equilibrium between monthly premium outlays and the robustness of financial protection. As Texas faces a 4.2% projected increase in operational costs due to inflationary pressures on vehicle parts and labor, a policy that seems inexpensive at first glance can quickly become a liability. Professional fleet managers recognize that the premium is only one component of the financial equation.

The 2026 regulatory environment in Texas has introduced stricter oversight on commercial auto insurance, making it vital for owner-operators to understand their coverage limits. Choosing a policy based solely on the lowest quote often results in gaps that leave a business vulnerable to litigation or cargo loss. When a claim occurs, the out-of-pocket expenses from an inadequate policy can exceed several years' worth of premium savings. This makes a balanced approach essential for long-term survival in the competitive Houston and San Antonio markets.

To better understand how these costs and coverages interact, watch this helpful video:

Cheap policies often strip away essential endorsements like Reefer Breakdown or Earned Freight coverage. Major brokers in Houston and Dallas frequently require specific policy language before they'll sign a contract with a carrier. If your policy doesn't meet these standards, you lose revenue opportunities. Using A-rated carriers ensures that the insurer has the financial liquidity to pay out claims during economic downturns. Total cost of risk is the sum of premiums, deductibles, and uninsured losses.

Captive agents work for one company; they can't shop around when rates rise. Independent brokers like AMCO operate differently by maintaining access to a broad network of specialized carriers. This model allows for the identification of niche discounts based on specific safety tech or route history. For fleets in San Antonio or Houston, this personalized approach means policies are tailored to actual usage rather than a generic template. AMCO leverages these industry relationships to secure terms that captive agents simply can't access. This expertise is critical when seeking affordable trucking insurance that doesn't compromise on the quality of the carrier or the speed of claims processing.

Texas carriers operate within a complex regulatory framework that demands strict adherence to both state and federal mandates. To maintain your operating authority, your policy must align with the Federal insurance requirements set by the FMCSA, alongside the specific mandates of the Texas Department of Insurance (TDI). These regulations aren't merely administrative hurdles; they serve as the primary defense for your business assets against catastrophic litigation. For a detailed breakdown of local compliance, consult our Commercial Trucking Insurance Houston pillar article.

Primary liability is the foundation of your policy. While the federal government sets a baseline of $750,000 for general freight, the 2026 industry standard for most brokers and shippers is a $1 million limit. Carriers opting for $2 million limits often see higher premiums, but they gain access to exclusive, high-paying contracts that smaller fleets cannot touch. Physical damage coverage is equally vital, particularly as the market value for new high-efficiency diesel and electric trucks has stabilized at approximately $185,000 in early 2026. Adjusting your deductible is a direct lever for cost control. Moving from a $1,000 to a $2,500 deductible can significantly lower your fixed costs, helping you maintain affordable trucking insurance while protecting your equipment's actual cash value.

Cargo insurance receives the highest level of scrutiny from shippers at the Port of Houston. With the port reporting a 12% increase in high-value electronics and machinery transit in 2025, cargo limits must be precise. Most Houston-based contracts now require a minimum of $100,000 in cargo coverage, though specialized haulers often carry much more. For a comprehensive breakdown of how this coverage works and what it protects, review our detailed guide on motor truck cargo insurance for Houston carriers. For owner-operators, Non-Trucking Liability (NTL) is a critical addition. It provides protection when the tractor is used for non-business purposes, such as driving home after a drop-off. You can explore the nuances of these policies in our Semi Truck Insurance guide. Selecting the right balance of these components is essential for maintaining affordable trucking insurance without leaving your business exposed to gaps in coverage. Operators running lighter commercial vehicles should also review our dedicated box truck insurance guide for Houston and Texas to ensure their specific vehicle class and cargo requirements are properly addressed.

Understanding these core components allows you to build a resilient safety net that satisfies both legal requirements and the expectations of your most profitable clients. A well-structured policy is the first step toward a more stable and predictable logistics operation in the competitive Texas market.

Many owner-operators and fleet managers operate under the misconception that insurance is a rigid, fixed cost. This perspective overlooks the technical variables that underwriters use to calculate risk profiles. Since 1987, AMCO has leveraged 39 years of Texas-specific data to challenge this "fixed cost" myth. By analyzing the unique traffic patterns within the Houston-Dallas-San Antonio "Texas Triangle," we identify specific risk-reduction opportunities that standard national brokers often miss. For instance, freight moving through the Laredo border crossing requires specialized international liability considerations; however, it also offers a chance to demonstrate superior safety protocols to carriers. Our deep history in the state allows us to present your fleet's data in a way that highlights stability and professional oversight.

Limiting operations to "Intrastate" routes within Texas boundaries can frequently result in lower premium tiers compared to interstate hauling. Underwriters scrutinize high-volume corridors like I-10, I-35, and I-45 due to their dense commercial traffic and accident frequency. According to the American Trucking Associations, proactive safety management is the most effective way to stabilize long-term operational costs. To secure affordable trucking insurance, fleets should implement these documentation strategies to satisfy underwriter queries:

By 2026, the integration of ELD data and AI-powered dashcams has become the primary driver for premium credits. Modern insurance carriers now rely on a "Safety Score" generated from real-time telemetry rather than historical averages alone. This data-centric approach is particularly vital for fleets operating in Midland and Odessa. The high-traffic oil field routes in the Permian Basin present extreme risks, but telematics allow companies to prove their drivers maintain safe speeds and following distances despite difficult conditions. Utilizing these technological tools doesn't just improve safety; it provides the empirical evidence needed to negotiate for affordable trucking insurance. This transition from reactive to predictive risk management ensures that your fleet's technological investments translate directly into long-term financial returns and operational continuity.

Securing affordable trucking insurance requires a methodical approach that begins at least 90 days before your current policy expires. This window allows for a thorough market analysis without the pressure of a looming deadline. You'll need your Motor Carrier (MC) number and Department of Transportation (DOT) data ready for review. Brokers use this information to pull your safety history and operational radius, which are the primary drivers of your risk profile. Starting early ensures you aren't forced into a high-rate policy because you ran out of time to negotiate. For a detailed technical framework on this process, our guide to obtaining accurate commercial truck insurance quotes in Houston and Texas walks through every step from FMCSA filing verification to final policy issuance.

A formal safety manual isn't just a binder on a shelf; it's a financial asset. Presenting documented driver training programs and telematics data shows underwriters that you manage risk proactively. This transparency often leads to lower premiums because it reduces the perceived likelihood of future claims. Your Compliance, Safety, Accountability (CSA) scores act as a public report card. Carriers typically reserve their most competitive rates for fleets with scores below the 65% threshold in categories like Unsafe Driving or HOS Compliance. You must also provide loss runs, which are official reports from your previous insurers detailing all claims filed over the last 3 to 5 years. These records prove your historical performance and are mandatory for any credible quote.

Every driver in your fleet must maintain a clean Motor Vehicle Record (MVR). A single moving violation can increase a driver's individual premium by 15% to 25% depending on the severity of the infraction. Ensuring your team meets strict hiring standards is the most direct way to maintain eligibility for "preferred" insurance tiers. It's not just about the fleet's history, but the individual records of the people behind the wheel.

Consolidating your coverage through a single agency creates significant cost-optimization opportunities. Bundling your primary auto liability with general liability or workers compensation can trigger multi-policy discounts that reduce total spend by 5% to 10%. For owner-operators, AMCO can also manage Homeowners Insurance to provide a comprehensive protection package. Centralizing your business and personal needs under one roof simplifies administrative tasks and ensures there are no gaps in your coverage. This professional synergy allows your broker to advocate more effectively on your behalf during annual renewals.

To speed up the application process and ensure accuracy, have the following documents prepared:

By organizing these details in advance, you present your business as a low-risk, professional operation. This preparation is the foundation for finding affordable trucking insurance that doesn't compromise on essential coverage limits. Efficient documentation reflects an efficient business, which is exactly what underwriters look for when calculating rates.

Contact our specialists to optimize your trucking insurance portfolio today.

AMCO has served the Texas transportation sector since 1987. We don't just sell policies; we provide technical risk management solutions designed for the B2B market. Our team understands that finding affordable trucking insurance is a priority for owner-operators and fleet managers alike. We've built our reputation on three decades of stability and regional expertise. With physical locations in Houston, Laredo, and San Antonio, we stay connected to the local market conditions that affect your premiums. Our presence in these major shipping hubs allows us to offer insights that national, digital-only providers often miss.

Efficiency is the core of our service model. The AMCO mobile app allows you to handle payments and policy adjustments directly from your cab. This technology reduces administrative friction, allowing you to focus on delivery timelines rather than office logistics. We've streamlined our internal processes to match the pace of the modern logistics industry.

In the logistics industry, time is a quantifiable cost. A carrier waiting four hours for a COI might lose a high-value contract to a competitor who was ready in minutes. We've seen these delays result in significant revenue losses for small fleets. AMCO provides 24/7 digital access to your insurance documents through our secure portal. This rapid response is vital for specialized sectors like Hot Shot Trucking Insurance, where load boards move at a frantic pace. Our system ensures you're always ready to bid on the next job without technical interruptions.

The first year of a new trucking authority is the most difficult period for securing competitive rates. Many providers see new businesses as high-risk, but AMCO takes a consultative approach. We help you navigate the initial regulatory hurdles and safety requirements that impact your long-term costs. We're interested in your growth over the next decade, not just a single premium payment. If you prefer a local touch, you can visit an insurance company near me at one of our Texas branches to discuss your specific fleet needs with a specialist.

Our commitment to the Texas trucking community is based on reliability and professional depth. Get a quote today and secure the affordable trucking insurance your business needs to stay competitive in the 2026 market. We're ready to show you why experience matters when protecting your livelihood on the road.

Navigating the 2026 Texas logistics landscape requires a strategy that balances rigorous Houston port requirements with sustainable cost-optimization. Since 1987, AMCO has supported Texas carriers by providing direct access to a curated network of top-rated national and regional insurance providers. We handle the technical complexities of Texas-specific filings so your fleet stays on the road without administrative delays. Finding affordable trucking insurance isn't about reducing your protection; it's about utilizing nearly four decades of local market data to secure a risk profile that fits your specific operation. Our consultants focus on long-term ROI and operational safety, ensuring your coverage meets the evolving standards of the Texas Department of Insurance. We understand the unique pressures of the Gulf Coast corridors and provide the professional stability required for large-scale logistics. You don't have to navigate these regulatory shifts alone. Partner with a team that prioritizes your fleet's technical continuity and financial security. Get Your Affordable Texas Trucking Insurance Quote Today

Your business deserves a partner that understands the road ahead. Let's build a secure foundation for your 2026 growth.

Commercial truck insurance in Texas for 2026 typically ranges from $9,000 to $16,000 per power unit for established fleets with clean safety records. New authorities often face higher premiums, with initial annual costs frequently exceeding $21,000. These figures depend on your specific radius of operation and the commodities you haul. Accurate budgeting requires a technical evaluation of your fleet's risk profile to identify specific cost drivers.

The FMCSA requires a minimum of $750,000 in primary liability coverage for interstate carriers hauling non-hazardous general freight. However, 98 percent of brokers and shippers in the Texas market require a $1,000,000 limit before they'll provide a load. If you're hauling hazardous materials, the federal requirement increases to $5,000,000. Operating below these industry standards significantly limits your ability to secure profitable freight contracts.

Securing affordable trucking insurance with a high CSA score is difficult because underwriters use BASIC percentiles to predict future claim frequency. Carriers with scores exceeding the 65 percent intervention threshold in categories like Unsafe Driving often see premium surcharges of 25 percent or more. You can stabilize costs by implementing a formal safety management plan and documenting corrective actions for every violation recorded in the last 24 months.

AMCO provides specialized insurance solutions for hot shot trucking operations located in the Houston area and across Southeast Texas. Our policies address the unique risks of Class 3 through 5 vehicles, including specific cargo coverage for industrial equipment and oilfield supplies. We focus on technical precision to ensure your coverage meets the strict requirements of Houston's diverse shipping hubs while maintaining your operational budget.

You can lower your premium immediately by increasing your physical damage deductible from $1,000 to $2,500 or $5,000. This adjustment often yields a 7 to 12 percent reduction in your monthly costs. Implementing ELD-integrated telematics and forward-facing cameras also allows us to negotiate safety credits with underwriters. Maintaining a consistent focus on driver MVRs remains the most effective way to secure affordable trucking insurance over the long term.

You need your DOT number, a current Motor Vehicle Report (MVR) for all drivers, and 3 years of verified loss runs to receive an accurate quote. Providing a detailed equipment list with VINs and current market values ensures the technical accuracy of the proposal. For new ventures, a summary of the owner's previous CDL experience can help underwriters assess risk more favorably, potentially leading to faster approval times.

Bobtail insurance and non-trucking liability (NTL) are distinct coverages that serve different operational functions. Bobtail insurance provides liability protection whenever a tractor is operated without a trailer, regardless of whether the driver is under dispatch. NTL only applies when the truck is used for personal, non-business purposes. Selecting the wrong coverage can lead to a total claim denial, so it's vital to align your policy with your specific lease agreement.

Most insurance providers in Texas offer monthly installment plans that typically require an upfront down payment of 15 to 25 percent. These plans allow carriers to preserve working capital for fuel and maintenance rather than paying the full annual premium at once. We work with premium finance companies to structure these payments logically. This approach ensures your cash flow remains stable while you maintain the necessary coverage for your operations.