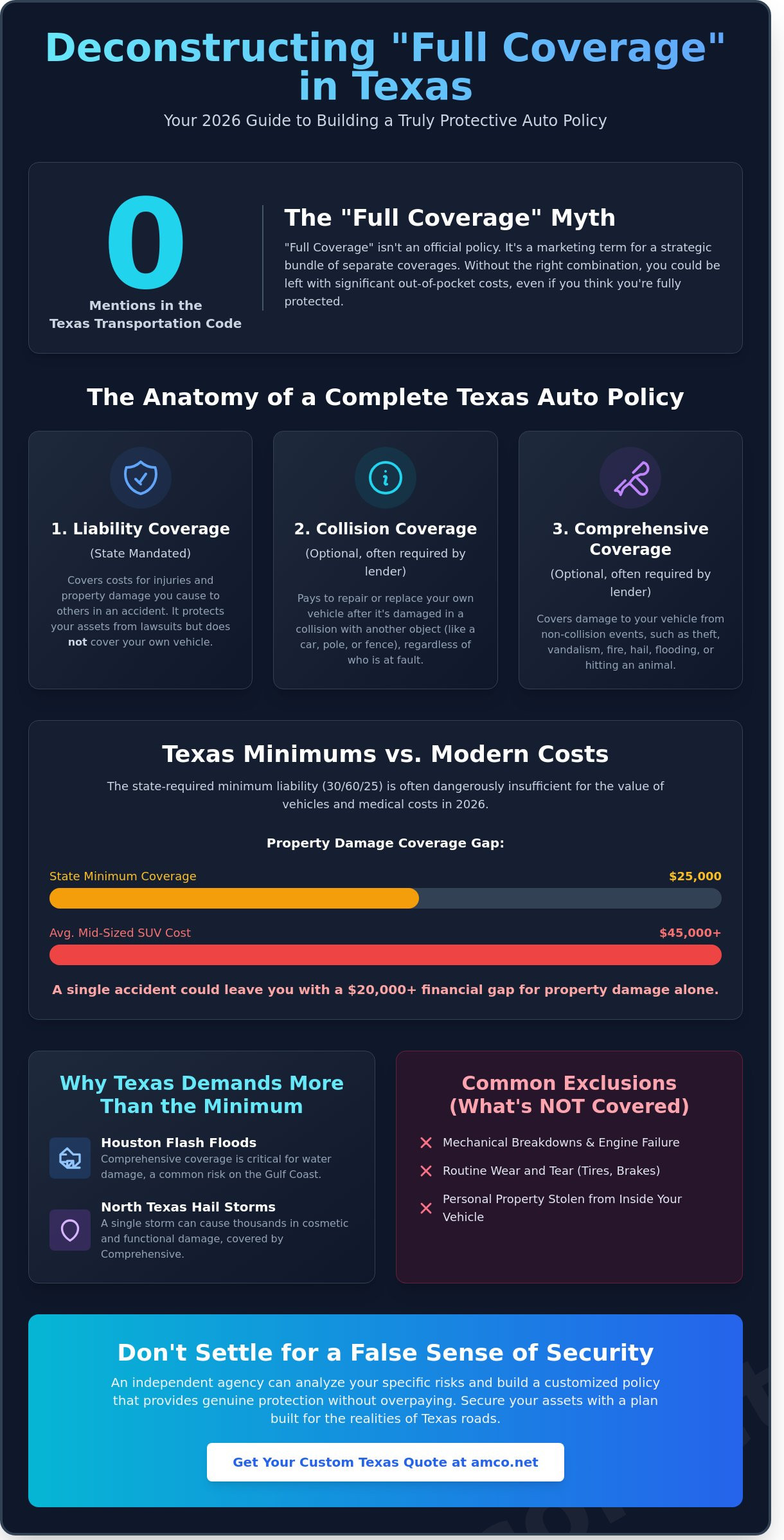

Did you know that the term "full coverage" appears zero times in the Texas Transportation Code? It's a common marketing shorthand that leaves many of the 18 million licensed drivers in the Lone Star State vulnerable to unexpected costs after a collision. While you might assume your full coverage car insurance policy protects you against every possible scenario, the reality is often a patchwork of liability, collision, and comprehensive layers. If these aren't calibrated correctly, you could still face significant financial exposure despite paying your premiums on time.

It's understandable if you feel frustrated by rising costs in metros like Houston, where insurance rates climbed by an average of 7% in 2025 alone. You want the security of a robust policy, but you shouldn't have to overpay for protection that doesn't fit your specific risk profile. This guide provides a professional breakdown of how to structure your 2026 policy to safeguard your assets while maintaining a lean, efficient budget. We'll examine specific deductible strategies, Texas-specific coverage gaps, and the precise components required to build a truly comprehensive safety net for your vehicle.

Understanding the technical nuances of full coverage car insurance is essential for maintaining financial stability on Texas roads. While the term is common in the industry, it's not a specific policy type you'll find in a legal contract. Instead, it describes a comprehensive strategy that bundles different protections to minimize risk. According to the standard definitions of Vehicle insurance in the United States, these bundles are designed to protect both the driver's assets and the vehicle's value. This approach ensures that a single incident doesn't lead to a total loss of investment.

In 2026, the complexity of Houston and Dallas traffic requires a more sophisticated approach than simple compliance. Repair costs for modern electric vehicles and advanced driver-assistance systems (ADAS) have increased by 22% since 2023. Relying on state minimums in these high-traffic corridors often leaves drivers exposed to significant debt after an accident. Additionally, the 2026 climate projections for the Gulf Coast suggest a higher frequency of severe weather events, making the protections included in a broader plan more valuable than ever.

To gain a clearer perspective on how these components function together, watch this technical breakdown:

Many drivers mistakenly believe that a "full" policy protects against every possible scenario. It doesn't. Standard agreements exclude mechanical breakdowns, routine wear and tear, and personal property stolen from the vehicle's interior. Texas law mandates a 30/60/25 limit, which covers $30,000 per injured person, $60,000 per accident, and $25,000 for property damage. These figures are often insufficient for 2026 vehicle values, where a mid-sized SUV can easily exceed $45,000. Full coverage car insurance is the strategic combination of liability, collision, and comprehensive coverage. This trio addresses damage to others, damage to your own vehicle from a crash, and non-collision events like hail or theft.

Texas law strictly requires liability insurance to ensure you can pay for the damages you cause to other parties. The Texas Department of Insurance (TDI) oversees these policies, regulating how companies set rates and handle claims to maintain market stability. For drivers who have had their license suspended or have multiple infractions, integrating SR-22 insurance Texas requirements into their plan is a legal necessity. This certificate serves as a verified proof of financial responsibility. While the state only demands liability, lenders usually require the addition of collision and comprehensive components to protect their collateral until the loan is finalized.

A robust insurance portfolio in Houston requires more than the state-mandated minimums. While many drivers use the term full coverage car insurance, this actually refers to a specific assembly of policy components designed to mitigate physical and financial risk. A complete policy integrates collision, comprehensive, and liability protections to ensure operational continuity for the vehicle owner. By combining these elements, you create a shield against the high-cost variables of urban driving.

These two coverages function as the primary defense for your vehicle's physical integrity. Collision coverage addresses damage resulting from impact with another vehicle or a stationary object, such as a utility pole or a highway median. In contrast, comprehensive coverage provides a safety net against non-collision events. This includes theft, vandalism, and environmental hazards like hail or fallen trees. For those operating a financed or leased vehicle, these coverages are mandatory to protect the lender's equity in the asset.

Valuations in 2026 continue to fluctuate based on Actual Cash Value (ACV). This metric calculates the replacement cost minus depreciation at the exact time of the loss; it dictates the maximum payout for a total loss claim. Understanding ACV is critical for maintaining long-term asset security, as it ensures your expectations align with market realities during an appraisal.

Data from the insurance industry indicates that a significant percentage of drivers in Houston and San Antonio operate vehicles without valid insurance. Uninsured/Underinsured Motorist (UM/UIM) coverage is a technical necessity in these high-density environments. It bridges the gap when a third party lacks sufficient limits to cover your medical bills or repair costs. Detailed requirements for these protections are outlined in the Texas Department of Insurance auto insurance guide, which serves as the regulatory benchmark for state coverage standards.

UM/UIM provides broad protection that extends beyond the driver's seat. This coverage protects you even if you are a pedestrian or cyclist involved in an accident with an uninsured vehicle. To build a truly full coverage car insurance plan, you should also consider the following medical components:

Selecting the right balance between PIP and MedPay depends on your existing health insurance and disability coverage. PIP remains a preferred choice for many because it offers a layer of financial stability during a recovery period that MedPay does not provide. Integrating these specific layers ensures that your policy is not just a legal requirement, but a comprehensive risk management tool.

Drivers often claim that full coverage car insurance exceeds their monthly budget. This perspective focuses on immediate premiums rather than the long-term fiscal stability required in high-risk environments. In 2026, the average cost of a total vehicle loss in Texas has risen significantly due to inflation and vehicle complexity. For anyone operating a leased or financed vehicle, this coverage isn't optional. Lenders strictly mandate comprehensive and collision protections to safeguard their assets. Understanding What Is Full Coverage Car Insurance? helps clarify that this is a strategic combination of policies designed to prevent catastrophic out-of-pocket expenses after an accident or environmental event.

Houston drivers face atmospheric challenges that standard liability policies simply don't address. During the 2026 hurricane season, localized flash flooding remains a primary cause of total vehicle loss in Harris County. If a vehicle is submerged, only comprehensive coverage allows the owner to recover its actual cash value. In North Texas and parts of Austin, the risks shift toward "Hail Alley." A single 15-minute storm can cause $6,500 in exterior damage. Without full coverage car insurance, these environmental repairs become a direct personal liability that can disrupt a household's financial continuity.

Texas freeways like I-10, I-45, and I-35 are characterized by high-speed traffic and high-density congestion. By 2026, even mid-range sedans are equipped with sophisticated LiDAR and ultrasonic sensor arrays. A minor rear-end collision that previously cost $1,500 now often exceeds $4,000 because of the precision recalibration required for these safety systems. The Texas state minimum of 30/60/25 is frequently exhausted in a three-car pileup on the Katy Freeway. When these limits are reached, the driver is personally responsible for the remaining balance. For a detailed breakdown of local coverage needs, our Car Insurance in Houston, TX guide provides specific data on how to scale your policy for metropolitan risks. Choosing higher limits isn't about luxury; it's about professional risk management in an increasingly expensive automotive market.

Determining the economic viability of full coverage car insurance requires a calculated approach similar to asset management. For vehicles older than 10 years or those with high mileage, the annual premium combined with the deductible often approaches the vehicle's actual cash value. A standard industry benchmark suggests that if your annual premium exceeds 10% of your car's total market value, it's time to evaluate your risk exposure. Geography also dictates these costs. A driver in Laredo or Midland often pays lower premiums than someone in Houston's 77002 ZIP code due to lower traffic density and reduced flood risks. For a comprehensive overview of how statewide requirements and localized risk factors shape your premium, the Texas auto insurance guide for 2026 provides a detailed analysis of mandatory and optional protections across the state.

Texas drivers can optimize their ROI through several discount structures:

Selecting a deductible is a liquidity decision. Shifting from a $500 to a $1,000 deductible can lower your annual collision premium by approximately 20%. However, you must pass the "Out-of-Pocket" test. If an accident occurs tomorrow, can you immediately clear a $1,000 expense without disrupting your financial stability? For newer vehicles, higher deductibles maximize long-term savings; for older assets, lower deductibles ensure the payout remains meaningful after a total loss.

Texas insurance providers utilize credit-based insurance scores to forecast risk. Data from the Texas Department of Insurance shows that credit history significantly correlates with claim frequency. Drivers with poor credit may pay 50% more than those with excellent scores. Your claims history also functions as a primary performance metric. Avoiding small claims prevents premium spikes that often outweigh the initial payout.

You can explore finding cheap car insurance in Houston by auditing your current policy for redundant add-ons. Strategic adjustments to your coverage limits ensure you aren't over-insured for a depreciating asset. Maintaining professional oversight of your policy details is the most reliable way to ensure long-term cost efficiency. When you're ready to compare options, reviewing car insurance quotes Houston drivers use to benchmark competitive rates can help you identify where your current policy may be costing you more than necessary.

Consult our specialists at amco.net to optimize your insurance strategy and secure your financial assets.

Selecting the right insurance policy requires a strategy that goes beyond standard templates. Most drivers are familiar with captive carriers, which are restricted to selling products from a single insurance company. AMCO.NET LLC operates as an independent agency, providing a distinct structural advantage. We don't work for one specific brand; we work for the policyholder. This independence allows our agents to scan a broad network of carriers to find the most efficient full coverage car insurance options available in the current market.

With over 35 years of experience serving the Houston and San Antonio regions, AMCO.NET LLC has developed a deep understanding of the Texas insurance landscape. Since its founding in 1987, AMCO.NET LLC has focused on a consultative approach that prioritizes technical accuracy and long term reliability. We utilize high speed digital quoting tools to provide immediate results, yet we maintain a human element in every transaction. Our experts review the data to ensure the policy limits align with your actual risk exposure, combining modern efficiency with professional oversight.

Texas road conditions are not uniform, and a one-size-fits-all policy often fails when a claim is filed. Our team understands the specific environmental and traffic risks across Houston, San Antonio, Dallas, Austin, and the Rio Grande Valley. Whether you are navigating the heavy industrial traffic in Midland or the high-density commuter routes of Bryan and College Station, we tailor your full coverage car insurance to meet those localized challenges. Local agents recognize regional patterns, such as flash flooding risks or high uninsured motorist rates, which national call centers frequently ignore.

The process of upgrading your protection is designed to be seamless and transparent. We begin by evaluating your existing policy to find hidden vulnerabilities that could lead to out-of-pocket expenses. Our goal is to optimize your coverage so you aren't paying for unnecessary add-ons while ensuring your core assets are fully protected. If you are looking for a partner who values professional integrity and technical precision, get a fast and affordable car insurance quote from AMCO.NET LLC. Secure a policy that provides genuine peace of mind for 2026 and beyond.

Texas roads require more than just the state-mandated minimums to ensure long-term financial stability. Choosing full coverage car insurance provides the necessary technical barrier against non-collision events and underinsured motorists. Since 1987, our agency has focused on providing this level of professional depth and risk mitigation for drivers in Houston, San Antonio, and throughout the state. We don't simply offer generic policies; we systematically analyze 20+ different carriers to identify the specific configuration that matches your unique risk profile. This data-centered approach removes the guesswork from policy selection.

Our bilingual specialists offer the expert support needed to navigate complex insurance specifications with precision. This methodical strategy helps you maintain continuity, ensuring that an unexpected incident doesn't disrupt your professional or personal momentum. By leveraging our decades of market experience, you gain a partner dedicated to your protection and operational security. We focus on creating a stable environment for your vehicle assets through rigorous comparison and expert consultation.

Get Your Free Full Coverage Quote from AMCO Today

You can rely on our established history and professional expertise to keep your journey secure and predictable.

Texas law doesn't require full coverage car insurance; it only mandates minimum liability limits of 30/60/25. This means every driver must carry $30,000 for individual bodily injury, $60,000 per accident, and $25,000 for property damage. While the state doesn't demand comprehensive or collision protection, most Houston lienholders and leasing companies mandate these coverages as a condition of your financing contract to protect their asset.

Projecting costs for 2026 suggests Houston drivers will pay approximately $2,720 annually for a standard policy. This estimate builds upon the 2024 Bankrate average of $2,467 for Texas, accounting for the 5% annual inflation rate observed in regional automotive repair and labor costs. Your specific premium depends on your ZIP code, as rates in 77002 often differ from those in 77084 due to local accident frequency data and litigation trends. To see how your current rate compares to the market, reviewing car insurance quotes Houston residents are receiving in 2026 can provide a useful benchmark for evaluating your existing policy.

Full coverage doesn't automatically include a rental car unless you specifically add rental reimbursement coverage to your policy. Most standard Houston policies categorize this as an optional endorsement rather than a core component of comprehensive or collision protection. If you've selected a typical $30 per day limit, your insurer pays for a replacement vehicle while a licensed facility repairs your primary car following a covered loss.

Liability insurance only pays for the other driver's medical bills and property damage if you're at fault in an accident. In contrast, full coverage car insurance adds collision and comprehensive layers that protect your own vehicle assets. This combination ensures that 100% of the vehicle's actual cash value is protected against incidents like multi-car collisions, floods, or vandalism, minus your chosen deductible amount.

Comprehensive insurance covers vehicle theft regardless of whether it happens in Dallas, San Antonio, or Houston. According to the Texas Department of Public Safety, vehicle theft rates fluctuate by city, but your policy's geographic scope remains consistent across the state. If your car is stolen, the insurer pays the actual cash value of the vehicle after you pay the deductible, provided you've filed a police report within 24 hours of the incident.

You can obtain full coverage car insurance even if the Texas Department of Public Safety requires an SR-22 filing on your record. The SR-22 isn't a type of insurance but a certificate your carrier sends to the state to prove you're maintaining the legal minimums. Carriers specializing in high-risk drivers provide these filings alongside comprehensive and collision options to ensure you meet both state mandates and lender requirements simultaneously.

Full coverage typically refers to vehicle protection and doesn't inherently cover your medical expenses unless you've included Personal Injury Protection (PIP) or Medical Payments coverage. Texas law requires insurers to offer at least $2,500 in PIP coverage, which you must decline in writing if you don't want it. PIP pays for your hospital bills and 80% of lost wages, filling the gap that collision and comprehensive insurance leave behind.