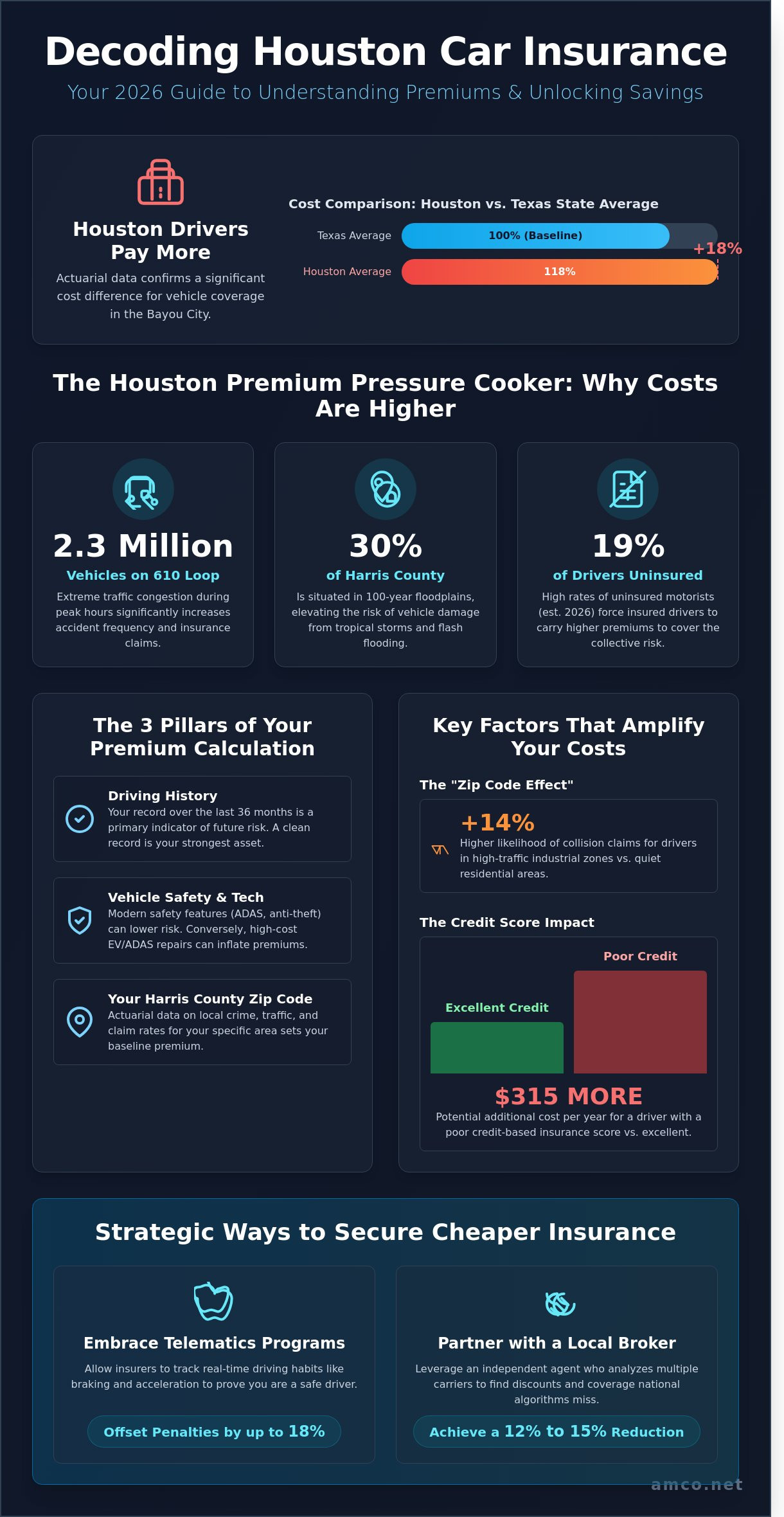

Recent 2025 actuarial data confirms that Houston motorists pay 18% more for vehicle coverage than the Texas state average, primarily due to the 2.3 million vehicles that congest the 610 Loop during peak hours. You've likely noticed your premiums increasing as carriers adjust for regional flood risks and the administrative complexities of SR-22 filings. It's frustrating when large, impersonal insurers fail to provide the transparency required to make an informed financial decision regarding your safety and legal compliance.

This strategic guide offers a technical framework for securing cheap car insurance houston without compromising the structural integrity of your liability protection. We'll demonstrate how to leverage specific 2026 local discounts and long-term cost-optimization methods that national algorithms often overlook. By the end of this analysis, you'll understand how to partner with a reliable local agency to achieve a 12% to 15% reduction in annual costs while maintaining a comprehensive safety net for your assets.

Finding cheap car insurance houston in 2026 requires a shift in perspective. It's no longer just about identifying the lowest monthly quote. In the current Texas economy, "cheap" represents the optimal intersection of minimum state requirements and the actual cost of risk mitigation. The Texas Department of Insurance (TDI) sets strict benchmarks for solvency and coverage, meaning any policy you purchase must provide a baseline level of security. While national algorithms often rely on broad zip code data, they frequently fail to account for the micro-economic shifts occurring within Harris County.

Understanding the U.S. auto insurance system is essential for any driver trying to balance a budget with legal obligations. Local expertise provides a distinct advantage here. A Houston-based advisor understands how a block-by-block risk assessment differs from the generic models used by massive out-of-state providers. They recognize that a driver in the Heights faces different environmental and traffic risks than one in Clear Lake, even if their credit profiles are identical.

Geography dictates costs in the Bayou City. With over 30% of Harris County situated within 100-year floodplains, comprehensive coverage rates reflect the perennial risk of tropical storms and flash flooding. Traffic density adds another layer of complexity. Data from late 2025 indicates that the I-10 and 610 Loop corridor remains one of the most accident-prone stretches in the country; average daily traffic counts now exceed 295,000 vehicles. Texas also faces a persistent challenge with uninsured motorists. Estimates for 2026 suggest that 19% of drivers on the East Freeway lack active policies, forcing insured drivers to carry higher premiums to offset the collective risk.

Legislative updates from the 89th Texas Legislature in 2025 have reshaped how insurers calculate risk based on credit scores and prior claims history. These changes aim to increase transparency, yet they've also led to a 12% average increase in base rates across the state. Inflation continues to impact the sector; the cost of specialized EV components and ADAS sensors rose by 14% between 2024 and 2026, which directly inflates repair estimates. A premium is the balance between transferred risk and monthly affordability. Achieving cheap car insurance houston means looking beyond the sticker price to ensure the policy's structural integrity matches your specific industrial or personal needs. For a broader statewide perspective on how these trends affect drivers across the region, our Texas auto insurance guide for 2026 provides a detailed analysis of requirements, costs, and localized risk factors.

Securing cheap car insurance houston isn't a matter of luck; it's a calculation based on specific risk variables that carriers analyze with mathematical precision. In 2026, insurers prioritize three primary pillars: your driving history over the last 36 months, the safety technology integrated into your vehicle, and the actuarial data tied to your specific zip code. While a clean record is the strongest asset for any driver, the geographic nuances of Harris County often dictate the baseline of your quote before you even get behind the wheel.

Location acts as a massive multiplier in the Houston market. For instance, a policyholder living in The Heights (77008) may see significantly different rates than one in Pasadena (77502). This discrepancy stems from local crime statistics and the density of industrial traffic. Data from 2025 indicates that drivers in high-traffic industrial zones face a 14% higher likelihood of collision claims compared to those in quieter residential pockets. Additionally, Texas insurers heavily weight credit-based insurance scores. Under current Texas auto insurance regulations, carriers use your credit history to forecast future risk. A driver with a "Poor" credit rating might pay $315 more annually than a driver with "Excellent" credit, regardless of their actual driving performance.

Houston's demographic shift toward a younger workforce affects the city's collective risk profile. With a median age of 33.7, the city has a high concentration of drivers in age brackets that insurers traditionally view as volatile. If you live in a high-density area like Downtown or Midtown, your "Zip Code Effect" includes elevated risks of vehicle theft and vandalism. To mitigate these "commuter risk" premiums, many residents are now opting for telematics programs. These systems track real-time braking and acceleration, potentially offsetting the geographic penalty by up to 18% for disciplined drivers. Much like how a business might seek specialized industrial reliability to protect its assets, Houston drivers must leverage technology to prove their individual safety standards to skeptical insurers.

The type of machine you navigate through the 610 Loop changes your financial liability. While the Ford F-150 remains a staple of Texas roads, its repair costs in 2026 have risen by 11% due to advanced sensor arrays, making it more expensive to insure than a standard sedan. Electric vehicles (EVs) present a unique challenge; while they offer fuel savings, their specialized battery components often result in premiums that are 22% higher than internal combustion counterparts. You can find savings by accurately reporting your vehicle usage. Categorizing your car for "Pleasure" use instead of a 20-mile daily "Commute" to the Energy Corridor can reduce your annual premium by approximately $195. It's a simple administrative adjustment that reflects a lower probability of peak-hour accidents.

Texas law mandates specific baseline coverage, often referred to as 30/60/25. These figures represent $30,000 for injuries per person, $60,000 total per accident, and $25,000 for property damage. While this meets the legal Texas auto insurance requirements, it rarely provides sufficient protection in a high-traffic metro like Houston. Full coverage isn't a single policy but a strategic combination of liability, collision, and comprehensive protections designed to safeguard your financial stability against unpredictable road conditions. To understand exactly how these layers work together, our detailed breakdown of full coverage car insurance in Texas explains how to calibrate each component for your specific risk profile.

Finding cheap car insurance houston residents can rely on involves balancing the monthly premium against the potential for catastrophic loss. In a city where vehicle values and medical costs continue to rise, the gap between a "cheap" policy and a "sufficient" one is often where financial ruin resides. A professional approach to insurance requires looking past the sticker price to evaluate the long term ROI of your coverage levels.

Low limits create significant exposure. Imagine a multi-car collision on the Sam Houston Tollway involving a 2026 luxury SUV valued at $85,000. If you're at fault and carry only the $25,000 state minimum for property damage, you're personally responsible for the $60,000 deficit. This is the "penny wise, pound foolish" trap. When your policy limits are exhausted, claimants can pursue your personal assets, including savings accounts and future wage garnishments. Relying on the absolute cheap car insurance houston offers without considering these tail risks is a gamble that few professionals can afford to take.

Houston drivers face unique environmental threats, specifically localized flooding and hurricane-related debris. Comprehensive coverage protects against these "acts of God," while collision coverage ensures your own vehicle is repaired or replaced after an accident. For those with financed vehicles, gap insurance is a critical component; it covers the difference between your remaining loan balance and the car's actual cash value after a total loss.

Cheap insurance is only cheap if it pays out when you need it.

Securing cheap car insurance houston requires a methodical approach to policy optimization rather than simply selecting the lowest quote. One of the most effective methods involves bundling multiple lines of coverage. Data from 2025 indicates that combining auto insurance with a homeowners or renters policy can reduce annual premiums by approximately 15% to 22% depending on the carrier's specific risk appetite.

For the 22% of Houston's workforce now engaged in remote or hybrid roles, telematics programs offer a data-driven path to savings. These systems monitor driving habits and mileage in real-time. If you drive fewer than 8,000 miles per year, a pay-per-mile structure often results in a 30% reduction compared to traditional fixed-rate policies. Your professional designation also serves as a critical risk indicator. Carriers frequently offer a 5% to 8% discount to engineers, educators, and healthcare professionals because statistical models link these roles to lower claim frequencies.

Security enhancements provide another layer of cost control. Vehicles equipped with GPS tracking systems or advanced anti-theft technology often see a reduction in the comprehensive portion of their premium. This is particularly relevant in high-traffic urban areas where theft rates are statistically higher than in rural districts. Before committing to any single carrier, comparing car insurance quotes houston drivers can access through local brokers is one of the most effective ways to ensure you're not overpaying for your specific risk profile.

Families residing in suburban hubs like Conroe or Pearland can leverage multi-car discounts, which often provide a 20% price break per vehicle on the policy. Academic performance also yields dividends. Students at the University of Houston or Rice University maintaining a 3.0 GPA typically qualify for "Good Student" discounts. Completing a state-approved 6-hour defensive driving course is another reliable tactic; it secures a 10% discount for a full 3-year period for drivers of all ages.

An SR-22 isn't insurance; it's a certificate of financial responsibility filed with the Texas Department of Public Safety. While it indicates higher risk, you can still find cheap car insurance houston by shopping with specialized non-standard carriers. Drivers without a dedicated vehicle should utilize "Non-Owner" policies to maintain continuous coverage history. Following a violation, most drivers can return to standard risk pools after 36 months of clean driving, which significantly lowers long-term costs. For detailed guidance on navigating these requirements, our comprehensive SR-22 insurance Texas filing guide provides step-by-step instructions for Houston drivers.

Selecting the right insurance partner requires a focus on long term stability and cost optimization. Most drivers encounter captive agents who represent a single insurance corporation. These agents are restricted to one set of underwriting guidelines and one price point. If that company's algorithm decides your ZIP code or vehicle type is high risk, your premium will reflect that bias without alternative options. AMCO operates as an independent broker, which shifts the power back to the consumer. Instead of defending one brand's rates, we analyze your specific risk profile against a network of 20+ different carriers.

Our role is consultative. We act as a technical bridge between complex insurance markets and your personal budget. This independence allows us to provide cheap car insurance houston drivers can actually rely on during a crisis. When a claim occurs on the busy streets of Houston, having a local advocate who understands the specific legal and repair environment of Southeast Texas is a significant operational advantage. We don't just sell a policy; we manage your financial protection through every stage of the contract life cycle.

Large national brands often rely on massive advertising budgets to drive volume, but these costs are frequently passed down to policyholders. Their rigid algorithms often penalize Houston residents for regional factors like flood risks or high traffic density on I-10. An independent broker bypasses these "Big Brand" hurdles by accessing niche carriers. These companies often skip expensive television commercials to maintain lower overhead, passing those savings directly to you. By submitting a single application through AMCO, you receive a comparative analysis of 10 or more quotes simultaneously. This method ensures you find the highest efficiency for your premium dollar without the manual labor of visiting dozens of websites.

AMCO has maintained a continuous presence in the Houston community since 1987. For over 30 years, our office on the East Fwy has served as a hub for reliable, expert advice. We've optimized our internal processes to eliminate the corporate red tape that often slows down policy changes or proof of insurance requests. Our commitment to technological continuity means you can manage your account through the AMCO mobile app, providing instant access to digital ID cards and payment portals while you're on the move. We combine this modern efficiency with the stability of a firm that has navigated the Houston market for decades. If you're ready to stop overpaying for basic coverage, it's time to leverage our experience.

Take the next step in your financial planning: Get your fast and cheap car insurance quote from AMCO today. Our experts are ready to build a policy that fits your specific needs and budget.

Navigating the 2026 insurance landscape requires more than just a quick online search. It demands a methodical approach to risk management and cost optimization. You've seen how balancing minimum liability with comprehensive protection is essential for long term financial stability. Finding cheap car insurance houston isn't about cutting corners; it's about leveraging professional partnerships that understand the local market's specific challenges. AMCO has served Houston drivers since 1987, providing the stability and technical expertise needed to secure competitive rates without sacrificing coverage quality.

Our bilingual agents analyze options from 20+ top-rated insurance carriers to ensure your policy aligns with current 2026 economic conditions. This data driven selection process removes the guesswork from your insurance planning. Don't leave your protection to chance when professional consultation is readily available. We're here to help you optimize your premiums today. Our team understands the complexities of the Texas market and works to ensure you're never overpaying for essential coverage.

Secure Your Affordable Houston Car Insurance Quote Now

You're now equipped to make an informed decision that protects both your vehicle and your bottom line on every Texas road.

The absolute cheapest car insurance allowed is a state minimum liability policy. Texas law requires a 30/60/25 coverage limit, which provides $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. As of January 2026, these policies serve as the baseline for legal operation. While this meets the legal mandate, it doesn't provide any financial protection for your own vehicle repairs after an accident.

Houston rates are 15% higher than the Texas state average because of extreme traffic density and regional weather risks. Data from 2025 shows that Houston drivers spend an average of 74 hours per year in congestion, which directly increases collision frequency. Additionally, the 2024 flood events led to an 8% spike in comprehensive claims across the metro area. These local environmental factors force insurers to adjust their risk models upward. For a comprehensive analysis of these cost factors, review our detailed car insurance houston guide for 2026.

You can obtain cheap car insurance houston even with a poor driving record by targeting non-standard insurance carriers. Companies like Bristol West or Dairyland specialize in high-risk profiles, including drivers with multiple speeding tickets or at-fault accidents. While your premium might be 45% higher than a clean-record driver, maintaining a 36 month period without new infractions will eventually qualify you for standard market rates and lower costs.

An SR-22 certificate typically involves a one-time filing fee between $15 and $25, but the underlying insurance premium often rises by 30% to 50%. This document isn't a separate policy; it's a state-mandated proof of financial responsibility. If your license was suspended in 2025, you'll likely need to maintain this filing for three consecutive years to satisfy Texas Department of Public Safety requirements and keep your driving privileges active. Understanding the complete process is essential, which is why we recommend reviewing our detailed guide on SR-22 insurance Texas requirements and costs.

Your credit score plays a significant role in determining your premium because Texas law permits the use of credit-based insurance scores. According to 2025 industry reports, a driver with a "Poor" credit score pays approximately $1,200 more per year than someone with "Excellent" credit for the same coverage. Insurers use this data to predict the likelihood of future claims, treating financial stability as a statistical proxy for road safety and responsibility.

Drivers who work from home can access significant savings through low-mileage discounts or usage-based insurance programs. If you drive fewer than 7,500 miles annually, you could reduce your premium by 10% to 15% compared to a standard commuter. Telematics programs like Allstate's Drivewise or State Farm's Steer Clear track your actual mileage and braking habits. These programs provide a data-driven way to secure cheap car insurance houston for remote professionals. To understand how statewide Texas auto insurance requirements and costs affect these savings opportunities, our 2026 guide offers a complete breakdown for drivers across the region.

You can lower your initial car insurance deposit by opting for an Electronic Funds Transfer (EFT) setup or paying your six-month premium in full. Paying the total amount upfront often eliminates the $50 to $100 start-up fees associated with monthly billing cycles. Setting up automatic withdrawals reduces the insurer's administrative risk; this frequently results in a 5% discount on the total policy cost and a smaller initial payment at the agency.

Choosing between a local agency and a national website depends on whether you prioritize personalized risk consulting or digital convenience. Local Houston agents understand specific neighborhood risks, such as the 100-year flood plains in Meyerland or traffic patterns on the 610 Loop. National websites offer 24/7 claims processing and mobile app integration. For complex needs, a local expert provides a professional layer of security that automated algorithms often miss.