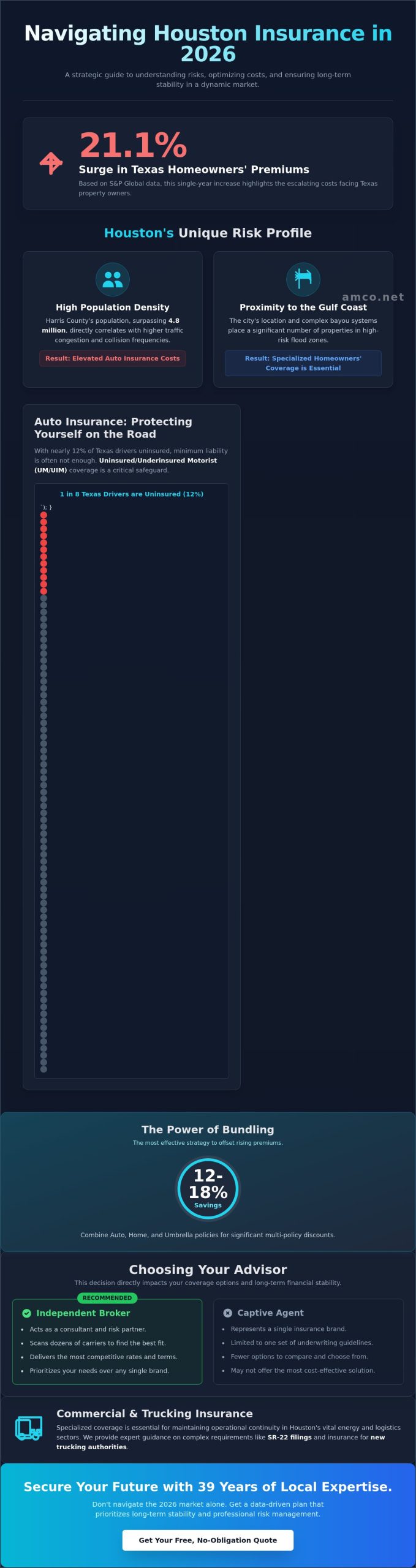

Did you know that average homeowners' premiums in Texas surged by 21.1% in a single year according to 2023 S&P Global data? This trend hasn't slowed as we head into 2026. It makes the search for reliable insurance houston a top priority for residents and business owners alike. You've probably noticed your monthly statements climbing even if you haven't filed a claim in years. It's a difficult reality to accept when you're trying to maintain a stable budget in an unpredictable market.

We believe that professional guidance should focus on cost optimization and long term stability rather than just selling a policy. This guide offers the technical insights you need to manage Texas-specific requirements like SR-22 filings and specialized trucking insurance for new authorities. You'll learn how to leverage local expertise to lower your monthly premiums while ensuring full legal compliance. We'll break down the 2026 landscape for personal, commercial, and specialty coverage to help you make data-driven decisions for your future.

Houston's insurance market in 2026 functions as a complex ecosystem where high-density urban living meets massive industrial operations. This landscape demands a sophisticated approach to risk, balancing the needs of individual homeowners with the heavy liability requirements of the energy and manufacturing sectors. As a firm with a 39-year legacy in the Greater Houston area, AMCO understands that local coverage isn't a one-size-fits-all commodity. It's a strategic asset for financial stability.

Regulatory oversight remains a critical factor for any policyholder. The Texas Department of Insurance (TDI) provides the framework for these operations, ensuring that carriers maintain the solvency needed to handle the region's unique challenges. Understanding these regulations helps businesses and residents anticipate shifts in the 2026 market.

To better understand the specific challenges of the local market, watch this helpful video:

Houston's premiums often outpace those in Austin or Dallas due to several fixed variables. Population density in Harris County, which surpassed 4.8 million residents by 2025, directly correlates with higher collision frequencies. This density elevates auto insurance costs significantly compared to less populated Texas hubs. Geographic exposure is the other primary driver. Proximity to the Gulf Coast and the city's complex bayou systems place many properties in high-risk flood zones. Houston insurance is a specialized risk management field that requires hyper-local data to price accurately.

Choosing between a captive agent and an independent broker is a decision that impacts long-term financial continuity. Captive agents represent a single brand, limiting your options to one set of underwriting guidelines. Independent brokers operate as consultants, scanning dozens of carriers to find the most competitive rates. This model is how savvy consumers secure cheap car insurance without sacrificing necessary coverage limits. For B2B clients, a broker acts as a risk partner, ensuring that insurance houston serves as a tool for operational resilience rather than just an unavoidable expense. Our 39 years of experience allows us to identify the most stable carriers in a volatile 2026 market.

Houston's economic landscape in 2026 demands a strategic approach to risk management for every household. With the cost of living in Harris County rising, insurance expenditures have become a significant portion of the family budget. Families often find that securing comprehensive insurance houston requires more than just meeting minimum legal requirements. Bundling auto, home, and umbrella policies remains the most effective strategy to mitigate rising premiums, often resulting in multi-policy discounts ranging from 12% to 18% depending on the carrier's risk appetite.

Driving in the Greater Houston area involves navigating some of the most congested corridors in the United States. While many drivers search for "cheap car insurance Houston" to lower monthly costs, prioritizing price over protection can lead to severe financial exposure. Standard policies include Liability, Collision, and Comprehensive coverages, but these are often insufficient in a high-traffic environment. According to 2024 data, nearly 12% of Texas drivers operate vehicles without active coverage, making Uninsured/Underinsured Motorist (UM/UIM) protection a critical necessity for local residents. This coverage ensures that your medical bills and repair costs are covered even if the at-fault party lacks adequate insurance. For a detailed breakdown of local requirements, refer to this car insurance in Houston guide.

To remain compliant with official Texas insurance regulations, motorists must maintain minimum liability limits, yet professional advisors suggest increasing these limits to at least $100,000 per person and $300,000 per accident to protect personal assets from litigation.

Whether you own a property in the Heights or rent an apartment in Midtown, protecting your dwelling requires specific attention to Houston's unique climate risks. Renters insurance is frequently overlooked by the 46% of Houstonians who lease their homes, yet it provides vital liability protection and coverage for personal belongings that a landlord's policy will not touch. For property owners, a standard policy is only the starting point. You must evaluate this Homeowners Insurance resource to understand how localized risks affect your premiums.

In 2026, a robust property policy in Houston should be evaluated against the following checklist:

Maintaining a secure household requires a partner who understands these technical nuances and offers stable, long-term insurance houston solutions. If you are looking to optimize your current coverage, you can explore comprehensive protection strategies that align with your specific risk profile.

Houston operates as the primary energy and logistics gateway for the United States. The Port of Houston consistently ranks first in the nation in foreign waterborne tonnage, handling over 284 million tons of cargo annually. This massive volume of trade necessitates a robust framework for insurance houston providers to support the thousands of carriers moving goods through the region. For owner-operators and fleet managers, managing risk isn't just a legal requirement; it's a vital component of operational efficiency. Maintaining technological continuity in a supply chain that moves billions of dollars in petrochemicals and consumer goods requires precise, data-driven coverage.

Texas remains unique as the only state that doesn't mandate Workers Compensation Insurance for private employers. However, for Houston businesses, going without this protection exposes the company to unlimited legal liability in personal injury lawsuits. Consulting the Texas Department of Insurance helps business owners understand the regulatory nuances of being a nonsubscriber, though most industrial firms opt for standard policies to ensure long-term fiscal stability. This proactive approach to safety and liability helps maintain the professional distance and trust required in large-scale B2B environments.

Launching a trucking business in Texas presents steep initial hurdles. New authorities often face higher premiums during their first 24 months of operation due to a lack of historical safety data. Carriers operating near the Port of Houston must secure specific endorsements to meet terminal requirements and federal FMCSA mandates. A standard policy must distinguish between primary liability, which covers third-party damage, and cargo insurance, which protects the specific freight being hauled. Detailed planning for commercial trucking insurance Houston ensures that new carriers remain compliant while protecting their capital investment in heavy equipment.

From the high-density Energy Corridor to the revitalized industrial spaces in EaDo, Houston small businesses require a foundation of General Liability (GL). This coverage protects against common risks like third-party bodily injury or property damage. Commercial Property insurance goes further, shielding physical assets from the Gulf Coast's unpredictable weather patterns. AMCO applies a technical, B2B risk assessment approach to these policies. We analyze the specific manufacturing or service workflows of a business to identify gaps where standard policies might fail. This methodical evaluation helps in achieving cost-optimization without sacrificing the safety of the enterprise. Using insurance houston experts allows business owners to focus on production while we handle the complexities of risk mitigation.

Texas law mandates specific liability limits for every driver, but adhering strictly to the state minimum of 30/60/25 is a risky strategy for residents. In a metropolitan area where the average cost of a new vehicle exceeded $48,000 in 2024, a $25,000 property damage limit often fails to cover even a moderate multi-car collision. Houston's legal landscape is notably aggressive; local data from 2023 indicates a higher-than-average rate of personal injury lawsuits following traffic incidents. If you rely on basic insurance houston coverage, you're personally liable for any costs exceeding your policy limits. This financial exposure can jeopardize your savings or business assets.

Drivers often find themselves confused by the term SR-22, frequently mistaking it for a specific type of policy. It's actually a financial responsibility certificate (Form SR-22) that your insurance carrier files directly with the Texas Department of Public Safety (DPS). "An SR-22 is a state-mandated filing that proves a driver carries the minimum required liability insurance."

The DPS typically requires this filing for two years following a license suspension due to a DUI, multiple at-fault accidents, or driving without valid coverage. To reinstate your driving privileges, you must find a carrier willing to issue the certificate. Not all companies provide this service, so it's essential to work with an agency that understands the electronic filing process to avoid delays in your license reinstatement.

For contractors and commercial entities in Harris County, licensing often hinges on securing financial guarantees rather than just standard liability coverage. While typical insurance protects your own interests, Surety Bonds function as a three-party agreement that protects the client or the state. If a contractor fails to meet the terms of a city permit or a private contract, the bond ensures the project is completed or damages are paid.

Securing the right insurance houston involves more than just selecting a policy; it requires a strategic approach to local mandates and risk management. Whether you're navigating a license reinstatement or securing a commercial bid, professional guidance ensures you don't leave your assets vulnerable to Texas's unique legal requirements.

To ensure your business meets all local compliance standards and remains protected, consult with our expert team today.

Selecting the right insurance Houston residents can trust involves more than comparing monthly premiums on a screen. It requires a partnership with a firm that understands the specific environmental and economic pressures of the Gulf Coast. AMCO has served as a professional anchor in the Texas market since 1987, providing the kind of stability that only decades of experience can foster. Local expertise acts as a primary tool for cost optimization. By identifying specific regional risks, such as local flood zones or specific neighborhood crime statistics, a local agent prevents the financial waste of over-insurance while ensuring no critical gaps remain in your coverage.

Professional risk management is about long-term stability rather than short-term savings. An agent who lives and works in the same community as you can offer insights that a national call center simply cannot. This consultant-led approach ensures that your policy isn't just a generic template, but a calculated response to your actual liabilities. Whether you are protecting a small business or a family home, the institutional knowledge AMCO has built over 37 years provides a measurable advantage in securing the best possible terms.

Modern insurance management requires a balance between digital speed and human reliability. AMCO bridges this gap by offering a dedicated mobile app designed for policy management, instant document access, and streamlined payments. This digital infrastructure allows for technical precision and efficiency. However, the brand maintains its core identity through the availability of real people in physical offices. You can manage your policy on your phone, but you can also sit down with a professional in a Houston office whenever your situation requires a more nuanced discussion.

The commitment to local service extends beyond the Houston metro area. AMCO maintains a strategic presence across the state, with established locations in San Antonio, Dallas, and Austin. This Texas-wide network ensures that the agency understands the broader state regulatory environment while maintaining the granular, local focus necessary for effective insurance houston services. It's a system where high-tech tools support, rather than replace, high-touch professional consultation.

Securing an accurate quote for the 2026 fiscal year requires a methodical gathering of data. To ensure the most precise rate, you should have your vehicle identification numbers (VINs), property structural details, and a comprehensive five-year claims history ready for review. AMCO operates as a brokerage, meaning they don't represent a single carrier. They analyze options from multiple A-rated insurance providers to find the most competitive rates available in the current market. This objective, data-driven process allows for a transparent comparison of coverage limits and deductibles.

Starting the process is straightforward through the website or the mobile app. Once the initial data is submitted, an agent performs a comprehensive risk review to ensure every discount and credit is applied to your profile. This professional oversight is what differentiates a standard quote from a customized protection plan.

Navigating the 2026 risk landscape requires a precise understanding of evolving Texas mandates and regional climate factors. Whether you're managing a commercial fleet or protecting a family home, local expertise remains the most critical asset for effective risk mitigation. Since 1987, our team has provided stable coverage solutions through A+ Rated carriers as designated by AM Best, ensuring long-term operational continuity for residents and business owners alike. Maintaining physical offices in Houston, Dallas, San Antonio, and Austin allows us to provide a direct pulse on the local regulatory environment that out-of-state providers often overlook. Selecting the right insurance houston provider isn't just about a policy; it's about establishing a partnership that prioritizes technical accuracy and long-term stability.

We've seen the market shift over 39 years and understand how to navigate these complexities for your specific needs. Our focus remains on data-driven solutions that protect your assets without unnecessary overhead. Take the next step toward securing your professional and personal interests with a team that values precision and reliability. You can trust our experience to guide your coverage decisions in an ever-changing economy.

Get a Fast & Affordable Houston Insurance Quote Now

Average car insurance in Houston is projected to exceed $2,600 per year for full coverage by 2026, based on a 5% annual growth trend from 2024 Bankrate data. This rise stems from increased vehicle technology costs and local climate risks. Your specific rate depends on your driving record and the vehicle's safety features. Most drivers in Harris County see higher premiums than the state average due to high traffic density and frequent weather claims.

Yes, Texas law requires all drivers to maintain financial responsibility for any accidents they cause. The Texas Department of Insurance mandates that motorists carry at least the minimum liability coverage to operate a vehicle legally on public roads. Failure to provide proof of insurance can result in fines starting at $175 for a first offense. Repeat offenders face fines up to $1,000 and vehicle impoundment under state law.

An independent agent represents multiple insurance companies, while a direct insurer sells policies directly to consumers from a single brand. Independent agents provide a consultative approach by comparing rates from 10 or more carriers to find the best value for insurance houston needs. This model offers a broader range of coverage options and customized risk assessments. Direct insurers handle all claims through their own proprietary systems, which might limit your options during renewal.

You can obtain an SR-22 filing immediately by contacting an authorized insurance provider to add the certificate to your policy. Most carriers transmit the filing electronically to the Texas Department of Public Safety within 24 hours. If you don't own a vehicle, you must purchase a non-owner policy to satisfy the state's financial responsibility requirement. This document is typically required for two years following a license suspension or a major traffic conviction.

No, standard homeowners policies in Texas exclude damage caused by rising surface water or flooding. Residents must purchase separate coverage through the National Flood Insurance Program (NFIP) or a private insurer. Data from FEMA shows that 20% of flood claims come from properties outside high-risk zones. Given that Houston received over 40 inches of rain during specific 2017 events, securing this additional policy is a fundamental step for long term asset protection.

Starting a hot shot business requires a minimum of $750,000 in primary liability insurance as mandated by the Federal Motor Carrier Safety Administration (FMCSA). You also need cargo insurance, typically starting at $100,000, and physical damage coverage for your truck and trailer. These requirements ensure compliance with Texas Department of Motor Vehicles regulations. Professional operators often add general liability and umbrella policies to protect their business assets from litigation and large scale losses.

You can manage your AMCO policy through our secure digital portal 24 hours a day. The platform allows you to download certificates of insurance, update vehicle rosters, and review policy limits without calling an office. This system provides the technological continuity required for modern business operations. It's designed to offer a transparent view of your coverage, allowing for quick adjustments as your industrial or logistical needs evolve throughout the year.

The current Texas minimum requirements, often called 30/60/25 coverage, include $30,000 for injuries per person, $60,000 for total injuries per accident, and $25,000 for property damage. These limits represent the baseline for insurance houston drivers to stay legal. However, 45% of accidents in urban areas exceed these limits. We recommend increasing these amounts to ensure your personal savings aren't targeted after a major collision on local highways.