On October 14, 2025, a Houston-based construction firm discovered that misidentifying a permit requirement as a standard insurance policy could stall a project for twenty-one days. It's a common frustration for professionals across Texas who find the distinction between insurance and Surety Bonds needlessly complex. You probably recognize the stress of a tight permit deadline or the concern that a fluctuating credit score might inflate your operational costs beyond your initial budget projections.

You'll master the regulatory framework of the Texas bonding market and identify exactly how to minimize your expenses while maintaining full legal compliance. We've structured this 2026 guide to provide a technical roadmap for businesses operating in Houston, Dallas, and San Antonio. This analysis details the precise factors influencing your rates, the specific obligations required by the State of Texas, and the most efficient methods to secure your documentation through a local partner who understands the regional industrial landscape.

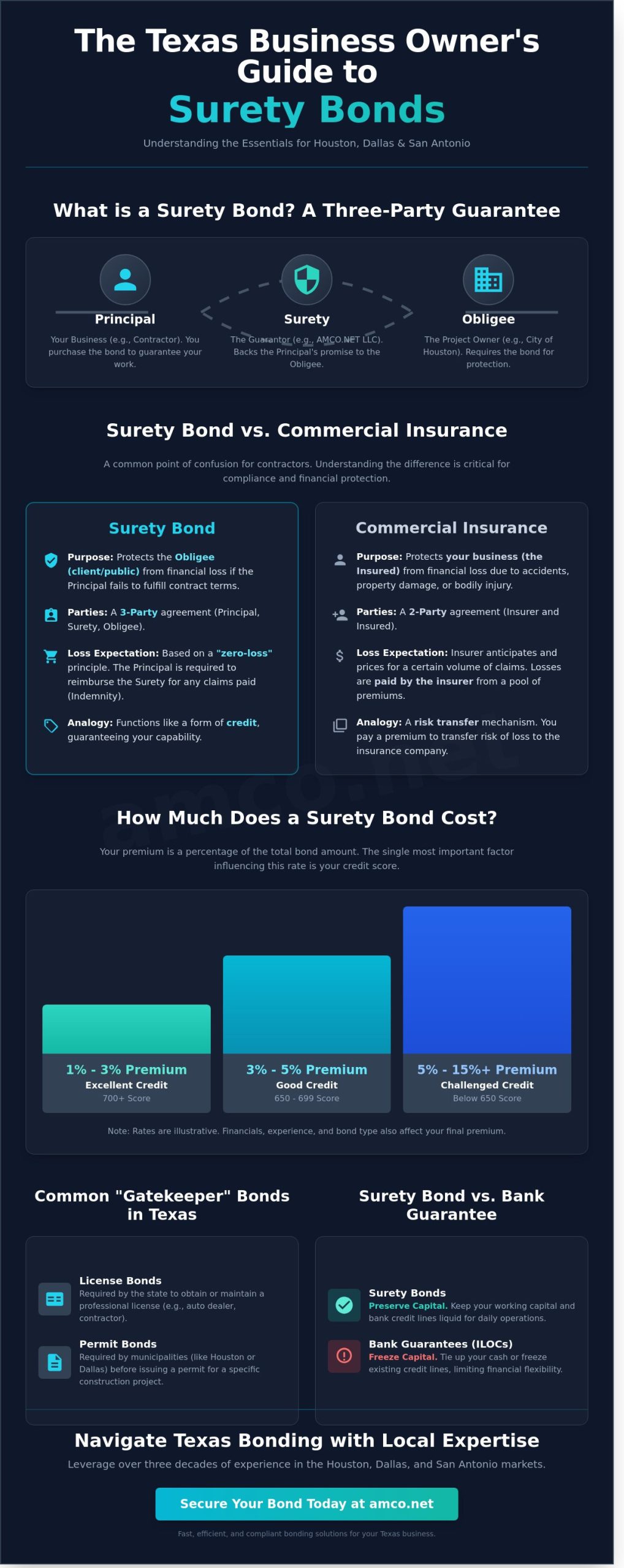

For Houston contractors, understanding the legal framework of What is a surety bond? is the first step toward securing municipal projects. It isn't insurance for your business. Instead, it's a three-party contract that guarantees you'll fulfill your professional obligations. If a contractor fails to meet the terms of a project in Harris County, the bond ensures the public doesn't bear the financial burden. The Texas Department of Insurance (TDI) regulates these instruments under the Texas Insurance Code to maintain market stability. This oversight ensures that companies like AMCO.NET LLC maintain the capital reserves necessary to back their promises. Without this regulation, the 140,000 licensed contractors in Texas would face a marketplace with no standardized financial protection for project owners.

To better understand this concept, watch this helpful video:

The structure of a bond relies on three distinct roles that create a cycle of accountability. The Principal is your business; your obligation is to perform the work as specified or pay the required fees. The Obligee is the Texas entity, like the City of Dallas or a Houston municipal department, that requires this guarantee before you can pull a permit or start a job. Finally, the Surety is the professional partner, such as AMCO.NET LLC, that backs your promise. We evaluate your financial health and past performance to tell the Obligee that you're capable of finishing the work. This relationship shifts the risk of project failure from the taxpayer to the surety company.

Choosing between Surety Bonds and bank guarantees often comes down to capital efficiency. Bank guarantees or Irrevocable Letters of Credit (ILOC) usually tie up your cash. They freeze your existing credit lines, which limits your ability to buy materials or meet payroll for other jobs. Bonds are different. They don't affect your bank borrowing capacity because they're off-balance sheet instruments. This allows you to keep your working capital liquid for daily operations. A surety is a financial guarantor of professional conduct. By using bonds, you maintain the financial flexibility needed to scale your operations without the restrictive collateral requirements common in traditional banking.

Contractors often mistake Surety Bonds for a variation of professional insurance. This misunderstanding can lead to financial friction during the bonding process. Traditional insurance is a two-party agreement where the carrier pays for losses on your behalf. In contrast, a bond is a three-party guarantee. It protects the project owner, known as the obligee, not the contractor. The bond acts as a financial backstop to ensure that a project reaches completion according to the contract terms.

The underwriting process reflects this distinction. Insurance companies use actuarial data to predict a certain volume of claims. Bonding companies operate on a "zero-loss" expectation. They only issue a bond if they believe the contractor is fully capable of completing the work without default. This makes the process feel more like a line of credit than an insurance policy. For smaller firms, SBA surety bond guarantees provide a pathway to secure larger projects by reducing the risk for the surety provider. These guarantees helped small businesses win over $6.3 billion in contracts during the 2023 fiscal year.

Even with robust bonding, you must maintain your General Liability Insurance. Bonds don't cover property damage or bodily injury. They ensure contractual performance and payment. While a bond protects the client from your potential failure, liability insurance protects your business assets from accidents and legal claims. Texas employers in the construction sector should also ensure they have a comprehensive understanding of Workers Compensation Insurance in Texas to protect their workforce and shield their operations from uncapped personal injury lawsuits.

An indemnity agreement is the core of the bonding relationship. If a claim occurs and the surety pays the obligee, you're legally obligated to reimburse the surety for every dollar spent. This differs from insurance, where the carrier absorbs the loss after you pay a deductible. This makes a bond a significant financial commitment. It requires a high level of professional accountability and transparency in your business operations. You're essentially putting your corporate and sometimes personal assets on the line to prove your reliability.

Insurance premiums are typically fixed based on industry risk categories. Bond premiums fluctuate based on your credit score, work history, and liquid assets. In Texas, multi-year bond terms are common for municipal projects, while smaller permit bonds may require annual renewals. Managing your overall risk profile is essential. For instance, maintaining a stable personal financial history, including your Homeowners Insurance, can indirectly influence your business's perceived stability during the underwriting phase. If you're looking to optimize your business's risk management strategy, you can consult with our technical advisors to find the right solutions for your specific operational needs.

Construction and contract bonds serve a different purpose, primarily protecting the financial integrity of public and private projects. This category includes:

Commercial bonds address specific operational risks outside the construction sector. For instance, the Texas Department of Motor Vehicles requires auto dealer bonds to protect consumers from fraud. Janitorial bonds provide peace of mind for cleaning services entering private offices, while utility bonds act as a deposit alternative for high-volume energy users. In legal settings, court and probate bonds are essential. These are required for fiduciaries, such as executors or guardians, to ensure they manage estates and legal proceedings with financial integrity as dictated by Texas probate courts.

The City of Houston Public Works department enforces strict bonding mandates for any work involving city-owned infrastructure or utility taps. Contractors in San Antonio must navigate different requirements, specifically securing Right-of-Way and Sidewalk bonds for projects that impact public thoroughfares. Dallas maintains its own standards, requiring specialized permit bonds for electrical and plumbing contractors to ensure all installations meet the 2023 National Electrical Code and local safety amendments.

Logistics professionals must prioritize the BMC-84 Freight Broker bond to maintain their operating authority. By the start of 2026, updated federal regulations will implement more rigorous financial scrutiny on these instruments to combat industry fraud. These Surety Bonds aren't a replacement for standard coverage; they work in tandem with your Commercial Trucking Insurance in Houston to create a comprehensive security framework. For carriers seeking new trucking authority from the FMCSA, securing the correct bond is the final, critical step in the registration process.

When you seek Surety Bonds in the Houston market, you're not paying the face value of the bond. You're paying a premium. This premium is a small percentage of the total coverage required by the obligee. For example, a $50,000 performance bond doesn't require a $50,000 check; instead, you pay a calculated fee to the surety company to guarantee that amount.

Your personal credit score acts as the primary lever for this cost. Applicants with scores above 700 typically secure rates near 1% of the bond amount. If your score falls below 600, rates can climb toward 15%. AMCO.NET LLC specializes in assisting Texas business owners who face credit challenges. We utilize our established relationships with underwriters to find competitive paths for those who might be rejected elsewhere. Our 24-hour bonding process ensures that your project timeline remains intact. We move from initial application to digital bond delivery within a single business day.

Three main variables dictate your final premium:

The transition to digital-first underwriting makes the process more efficient. In 2026, digital submissions are 60% faster than traditional paper methods. First, gather your Tax IDs and the specific requirements from your obligee. Most Houston municipal projects have unique bond forms you must use to be compliant.

Second, complete the online application. Once approved, you'll sign the indemnity agreement. This is a legal promise to reimburse the surety if a claim occurs. After payment, we provide your digital bond with an electronic seal. This allows you to submit your bid or permit application immediately without waiting for courier services.

If you're ready to stabilize your project pipeline with reliable financial guarantees, contact our expert advisors

Since 1987, AMCO has provided specialized financial security to contractors throughout Houston, Dallas, and San Antonio. We don't just process paperwork; we serve as a long-term risk management partner for firms that require stability to win larger contracts. Choosing an independent Insurance Company Near Me ensures you receive objective advice tailored to the specific regulatory demands of the Texas market. Our agents are real people based in Texas who understand that a bond delay can stall a project start date.

Managing your commercial auto, general liability insurance for Texas business owners, and Surety Bonds in a single, cohesive portfolio simplifies your administrative burden. By centralizing these essential coverages, you eliminate the gaps that often occur when using multiple disconnected providers. We prioritize technical precision in every filing, ensuring your business remains compliant with both state statutes and local municipal codes. You won't deal with automated web bots or offshore call centers here. Every consultation is handled by a professional who understands the local construction landscape.

We leverage our 37 years of industry relationships to shop multiple A-rated carriers, which allows us to secure the lowest possible rates for Texas contractors. Our team maintains a deep library of local municipal bond forms, from Houston permit bonds to specialized Dallas district requirements. This local knowledge prevents the common filing errors that lead to rejected permits. As your business scales, we provide ongoing support to increase your bond limits, ensuring your bonding capacity grows alongside your revenue and project ambitions. Protecting your physical assets is equally critical; our Commercial Property Insurance in Houston and Texas guide details how to safeguard your business locations against the region's significant weather-related risks.

Securing your Surety Bonds shouldn't be a bottleneck for your operations. We offer fast online quotes for standard needs in Houston and the surrounding areas, while providing high-level expert consultation for complex construction bonding requirements. Whether you are bidding on a public works project or need a simple license bond, our methodical approach ensures you get the right coverage without unnecessary delays. Our consultants analyze your specific project needs to recommend the most cost-effective bonding structure available today.

Ready to move forward with a partner who understands the Texas construction industry? Secure your Texas Surety Bond with AMCO today!

Navigating the regulatory landscape requires a strategic approach to risk management. You now understand that Surety Bonds act as a vital financial guarantee, differing significantly from standard commercial insurance. Whether you're based in Houston or San Antonio, selecting the correct bond ensures your projects stay compliant and on schedule. Since 1987, AMCO has provided the technical expertise necessary to handle these complex requirements with precision. We partner with A+ rated carriers to deliver the stability your business needs to thrive in a competitive market. Our process prioritizes efficiency, offering instant digital bond delivery so you don't face unnecessary downtime. We've spent nearly four decades focusing on the long-term success of our partners, moving beyond simple transactions to provide genuine industrial solutions. For a broader perspective on managing all your coverage needs in the region, our comprehensive guide to insurance in Houston, TX covers the full 2026 landscape for personal and commercial policies. Take the next step toward securing your professional obligations today.

Get Your Free Texas Surety Bond Quote in Minutes

We look forward to supporting your continued growth and operational excellence.

No, a surety bond isn't insurance. While insurance protects your business from financial loss, a surety bond protects the project owner or the City of Houston from your failure to perform. It's a three-party agreement that functions more like a line of credit. You're legally responsible for repaying the surety company for any claims they pay out on your behalf.

A $50,000 bond typically costs between 1% and 3% of the total bond amount for contractors with strong financial profiles. This means you'll likely pay an annual premium ranging from $500 to $1,500. Rates depend heavily on your credit score and business history. Applicants with lower credit scores might see rates increase to 5% or 10% of the bond's face value based on industry standard risk assessments.

Yes, you can still obtain surety bonds in Houston even if your credit score is below 650. Many specialized providers offer high-risk bonding programs designed for contractors in transition. You'll likely face higher premiums, often ranging from 5% to 15% of the bond amount. Providing updated financial statements or proof of 3 successfully completed projects can help secure approval in these cases.

Most standard license and permit bonds are approved within 24 hours of submitting your application. If you're applying for a complex performance bond for a City of Houston public works project, the process usually takes 5 to 10 business days. This longer timeframe allows the underwriter to review your company's financial health and past project performance thoroughly. Precision in your documentation speeds up this process.

The surety company first investigates the claim to determine its validity. If the claim is verified, the surety pays the claimant up to the bond's limit to resolve the issue. However, your obligations don't end there. You must reimburse the surety for every dollar paid out, including legal fees. This financial responsibility distinguishes surety bonds from traditional insurance policies where the carrier absorbs the loss.

Surety bond premiums are generally non-refundable once the bond has been filed with the obligee. Most carriers consider the premium fully earned after the first 90 days of the term. If you cancel within the first 30 days, you might receive a pro-rated refund. The surety often retains a minimum earned premium of $100 to cover administrative costs and filing fees.

You often need separate bonds because Texas doesn't have a single statewide contractor license bond. Houston requires specific bonds for various trades, such as the $10,000 Sidewalk and Driveway bond. If you expand your operations to Pearland or Sugar Land, you must check their local ordinances. Each municipality sets its own bond amounts and language requirements to protect its specific infrastructure and residents.

An indemnity agreement is a legally binding contract that requires you to compensate the surety company for any losses they incur due to your bond. This document often requires personal signatures from business owners and their spouses to provide additional security. It ensures the surety has a clear legal path to recover funds if they pay a claim. This agreement serves as the foundation of the trust between your business and the bonding company.