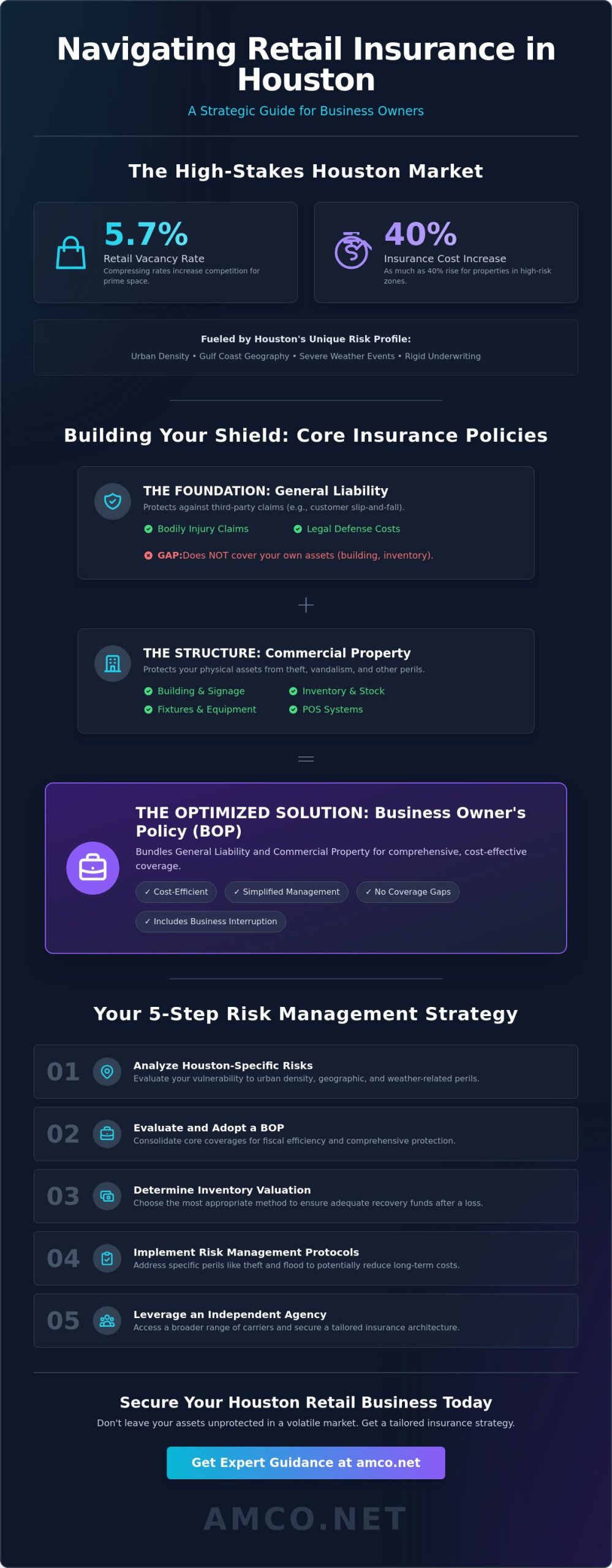

With Houston's retail vacancy rate compressing to 5.7 percent, the competition for prime space is high, yet the cost of protecting that space has risen by as much as 40 percent in high-risk zones. You've likely noticed that securing retail store insurance Houston isn't just a standard administrative task anymore; it's a complex strategic hurdle. Professional concern is a logical response to these market shifts, especially as underwriting guidelines for roof age and flood risk become increasingly rigid.

This guide provides a clear path to balancing comprehensive protection with fiscal responsibility. You'll learn how to leverage 2026 regulatory changes, such as House Bill 2067, to gain more transparency from carriers and optimize your risk management strategy. We'll examine the technical benefits of a Business Owners Policy (BOP), identify the critical gaps in standard property coverage, and outline how a local expert can help you maintain operational continuity in a volatile market.

Retail insurance functions as a multi-layered defensive system designed to mitigate the financial impact of operational disruptions and legal claims. For those seeking retail store insurance Houston, this coverage is rarely a single policy but rather a strategic combination of protections tailored to the specific demands of the Gulf Coast retail environment. It addresses the dual reality of maintaining physical assets while managing the public's presence on your premises. For inventory-heavy businesses, this framework acts as a critical financial safety net, ensuring that capital tied up in stock isn't wiped out by a single unforeseen event.

Houston's retail market, characterized by its high urban density and significant foot traffic, presents a unique risk profile. In a city where vacancy rates have tightened to 5.7 percent, the physical concentration of value in retail corridors increases the potential for high-impact accidents or theft. While certain insurance elements may be mandated by lease agreements or state law, others fall into the "should-have" category of asset protection. Distinguishing between these requirements is the first step in building a resilient business model that can withstand local market volatility.

To better understand how these property risks and premiums are managed in the local area, watch this helpful video:

General liability serves as the primary shield against third-party claims, specifically those involving bodily injury or property damage occurring at your place of business. In Houston, where sudden weather shifts can lead to hazardous walkway conditions, slip-and-fall incidents are a frequent concern for store owners. This coverage is essential for managing legal defense and settlement costs, but it's vital to recognize its limitations. Liability alone fails to protect your actual store contents, your building, or your specialized equipment. It's a foundational piece of retail store insurance Houston, yet it doesn't account for the loss of your own property.

Protecting the physical components of your enterprise requires robust Commercial Property Insurance. This coverage extends beyond the four walls of your storefront to include your exterior signage, specialized fixtures, and point-of-sale systems. It provides the necessary recovery funds if your location is targeted by theft or vandalism, which are persistent risks in high-density urban areas. Many small to mid-sized businesses choose to bundle these protections into a Business Owner's Policy (BOP) to ensure no gaps exist between liability and property coverage. This consolidated approach ensures that your inventory, from apparel to high-end electronics, remains a protected asset from the moment it enters your warehouse until it reaches the customer's hands.

The Business Owners Policy, or BOP, represents the most efficient structural framework for managing retail store insurance Houston. By integrating General Liability and Commercial Property insurance into a single package, businesses achieve a level of administrative and financial optimization that separate policies cannot match. While the federal government requires certain types of coverage depending on your business structure and location, the BOP is a voluntary but vital standard for the retail sector. It doesn't just simplify billing; it ensures that your legal defense and physical assets are managed under a unified risk strategy.

Efficiency is the primary driver for this bundle. Most Houston retailers find that the premium for a BOP is lower than the combined cost of purchasing standalone policies. This cost-efficiency allows owners to reallocate capital toward growth or inventory while maintaining high coverage limits. Beyond the basics, a BOP often includes Business Interruption insurance, which serves as a critical stabilization tool when external factors force your doors to close. You might also consider optional endorsements like cyber liability for your point-of-sale systems or equipment breakdown coverage for specialized climate control units.

In the Gulf Coast region, operational continuity is frequently threatened by extreme weather. Business Interruption coverage replaces lost net income and covers ongoing expenses, such as rent and payroll, when a store must close for repairs. Whether the disruption is caused by a prolonged power outage after a storm or civil unrest preventing access to your district, this policy prevents a temporary closure from becoming a permanent failure. It's the mechanism that keeps your cash flow steady when your sales floor is silent, providing the liquidity needed to survive a crisis.

Texas is unique because it doesn't mandate Workers Compensation Insurance for most private employers. However, for retail stores with warehouse staff or high-volume sales floors, opting into this coverage is a prudent risk management decision. It protects employees from workplace injuries while shielding the business from costly litigation. Additionally, if your store manages deliveries, supply runs, or mobile pop-ups, you'll need commercial auto coverage. Texas law requires minimum liability limits of 30/60/25 for business vehicles, ensuring you're protected during every trip. If you're looking to optimize your overhead, evaluating your current policy limits with a specialist can help you identify where you're over-insured or dangerously exposed.

A boutique in The Heights faces a fundamentally different risk profile than a hardware store in Pasadena. While the boutique may prioritize high liability limits to protect against claims from an affluent customer base, the hardware store requires extensive property coverage for high-value machinery and hazardous materials. Customizing your retail store insurance Houston ensures that you aren't paying for superfluous protections while leaving critical vulnerabilities exposed. This strategic alignment is a hallmark of professional risk management, moving beyond generic packages to address the operational realities of your specific trade.

Inventory valuation represents one of the most significant decisions in this tailoring process. Retailers must choose between Actual Cash Value (ACV) and Replacement Cost. ACV factors in depreciation, which might lower premiums but often leaves a shortfall during a total loss. Conversely, Replacement Cost provides the funds necessary to purchase new inventory at current market prices. For businesses with high-target items prone to theft, such as designer apparel or high-end tools, the choice of valuation can determine whether a business survives a major burglary. As noted in the Small Business Administration guide on business insurance, selecting the right coverage type is essential for long-term stability.

Product Liability is another essential consideration for retailers who private-label their goods or perform minor manufacturing. If a product you sell causes injury or damage, the legal responsibility often rests with the retailer if the original manufacturer cannot be reached. This is especially relevant for Houston's growing craft and artisan sectors, where "retailer" and "maker" often overlap. This extra layer of protection ensures that a single defective batch doesn't lead to catastrophic legal expenses.

Retailers dealing in jewelry or electronics require specialized inland marine insurance to protect high-value assets while in transit or on display. Insurance carriers often mandate specific security protocols, such as UL-rated safes or 24/7 monitored alarm systems, as a condition of coverage. If your store also provides repair services, professional liability is necessary to cover damage to a customer's property while it’s in your care. These technical details ensure that your highest-margin items don't become your greatest financial liability.

For grocery stores and wine boutiques, Houston's power grid stability remains a top concern. Spoilage coverage is a vital endorsement that replaces lost inventory following a refrigeration failure caused by a grid outage. Additionally, any store selling alcohol must maintain Liquor Liability insurance to protect against claims arising from the actions of intoxicated patrons. Maintaining strict health and safety compliance not only protects your customers but also serves as a primary factor in securing favorable premium rates from underwriters. It's a methodical approach to safety that pays dividends in both reputation and reduced insurance costs.

Finding the right balance between monthly premiums and out-of-pocket risk often comes down to your deductible structure. Deductibles for wind and hail damage are trending upward across the state, shifting more financial responsibility to the policyholder in the event of a claim. Consulting an insurance company near me allows you to access regional discounts that national carriers might overlook. These local experts understand the nuances of the Houston market, including the specific zip code data published by the Texas Department of Insurance under the 2026 transparency regulations.

A common misconception among new business owners is that standard property insurance covers all weather-related events. It's critical to understand that standard commercial policies in Texas do not cover flood damage. Given that a significant number of flood claims originate from properties outside of designated high-risk zones, securing a separate flood insurance policy is a fundamental requirement for Houston retailers. Additionally, windstorm and hail coverage often involve a separate, percentage-based deductible. Preparing your retail space with storm-resistant glass or reinforced roofing can mitigate potential damage and potentially lead to more favorable underwriting terms.

Several operational variables influence the final cost of your retail store insurance Houston. Underwriters examine your annual revenue and the total square footage of your retail space to estimate potential liability exposure. Your professional experience and claims history also play a significant role; a clean record suggests a disciplined approach to risk management. Modern insurers are also implementing stricter guidelines for infrastructure. For instance, many carriers now refuse to write new policies for roofs older than 15 to 20 years. Implementing specific safety protocols can also drive down costs:

To ensure your business remains compliant and cost-effective, you can request a comprehensive coverage audit to identify hidden savings and close dangerous protection gaps.

Since 1987, AMCO.NET LLC has provided a stable anchor for the Houston business community. We've witnessed the evolution of the local market, from the expansion of suburban retail hubs to the revitalization of urban corridors. This historical perspective allows us to offer more than just a policy; we provide a system-level solution for retail store insurance Houston that accounts for decades of regional risk data. You aren't treated as a mere data point in a national algorithm. Instead, you're a neighbor whose operational continuity is vital to our city's economy. Our consultative approach focuses on identifying the specific technical details of your business to ensure no vulnerability is overlooked.

Our status as an independent agency is a strategic asset for our clients. Unlike captive agents who are restricted to a single carrier's underwriting appetite, we maintain a diverse portfolio of insurance providers. This independence means we shop the market on your behalf to find the optimal balance between comprehensive protection and fiscal efficiency. Whether you need specialized retail liability or commercial trucking insurance Houston for your logistics fleet, our team analyzes multiple quotes to ensure your coverage is technically sound and competitively priced. We prioritize transparency, providing clear explanations of why certain carriers are better suited for your specific industry niche.

We understand that Houston’s zoning and local business regulations can be complex. A national chain often lacks the granular knowledge required to navigate the specific insurance requirements of different Houston districts. Our expertise in General Liability Insurance allows us to tailor limits for diverse store types, from high-traffic apparel outlets to specialized hardware suppliers. This local insight ensures that your retail store insurance Houston meets every legal and lease-related obligation without unnecessary overhead. We stay current with the 2026 regulatory landscape, ensuring your business remains compliant as Texas laws evolve.

Efficiency is a core pillar of our service model. We've integrated modern technology to allow for easy online management of your policies via our website and mobile app. We recognize that in the retail sector, time is a critical resource. Our commitment to fast turnaround times for certificates of insurance ensures that you can sign leases or finalize vendor contracts without administrative delays. We focus on providing long-term support rather than just a one-time transaction, acting as your professional partner through every renewal and claim. Request a free retail insurance quote from AMCO.NET today. and let our experienced team build a resilient foundation for your business's future.

Building operational resilience in the Houston market requires a proactive approach to your insurance architecture. By consolidating core protections into a Business Owners Policy and addressing specific environmental threats like flash flooding, you create a stable foundation for sustained growth. The 2026 regulatory environment offers greater transparency for policyholders; however, navigating these technical shifts effectively requires a partner who understands the local landscape. Selecting the right retail store insurance Houston ensures that your inventory and legal standing remain protected against the unique volatility of the Gulf Coast.

AMCO.NET LLC has served the Houston business community since 1987, providing the professional stability needed to manage complex insurance portfolios. As an independent broker, we shop multiple carriers to find the most competitive rates and comprehensive terms for our neighbors. Our commitment to A+ personalized customer support ensures you have a dedicated expert to guide you through every decision. Protect your Houston storefront with a custom retail insurance quote from AMCO.NET. Establishing a secure future for your store begins with a precise, data-driven strategy today.

Texas state law doesn't mandate general business liability insurance for most private retailers. However, you're legally required to carry commercial auto insurance if your business uses vehicles for deliveries or supply runs. Most commercial landlords in the Houston area also require proof of general liability coverage as a condition of your lease agreement to mitigate their own risk exposure during your tenancy.

The cost of retail store insurance Houston depends on your specific risk profile, inventory value, and location. As of 2026, the average annual premium for a Business Owner's Policy in Texas is approximately $877. Factors such as proximity to high-risk flood zones or urban high-traffic areas will influence your final quote. Obtaining a tailored assessment is the most accurate way to determine your exact operational expenses.

Standard commercial property insurance policies typically exclude damage caused by rising water or flash flooding. While your policy may cover wind and hail damage from a hurricane, you must secure a separate flood insurance policy to protect your physical assets from water-related perils. This distinction is critical for Houston retailers, as a significant number of flood claims originate from properties outside of designated high-risk zones.

A Business Owner's Policy (BOP) is a consolidated insurance package that bundles general liability and commercial property insurance into a single contract. This structure is more cost-effective than purchasing separate policies and ensures there are no coverage gaps between your liability protection and asset coverage. It provides a comprehensive safety net for small to mid-sized retail operations managing significant physical inventory and foot traffic.

Yes, e-commerce businesses based in Houston require specific protections even without a traditional brick-and-mortar storefront. Your policy should focus on product liability and cyber insurance to protect against data breaches and digital disruptions. If you maintain a home office or warehouse for inventory, you'll also need commercial property coverage, as standard homeowners' policies often exclude business-related equipment and stock held for sale.

You can lower your premiums by implementing robust risk management protocols and upgrading your store's physical security. Installing monitored alarm systems, automatic fire sprinklers, and maintaining a claims-free history are primary factors that underwriters consider for discounts. Additionally, choosing a higher deductible can reduce your monthly premium, provided your business has the necessary liquidity to cover the increased out-of-pocket costs during a claim.

If a customer is injured on your premises, your general liability insurance manages the resulting financial and legal consequences. This coverage pays for the injured party's medical expenses and covers your legal defense costs if a lawsuit is filed. Promptly documenting the incident and contacting your agent ensures that the claim process begins immediately, protecting your business from prolonged litigation and potential reputational damage.

Standard retail policies often exclude theft committed by employees unless you add a specific endorsement for employee dishonesty or crime insurance. This coverage protects your business from financial losses resulting from fraudulent acts, embezzlement, or the theft of physical inventory by staff members. It's a vital addition for retailers with multiple employees or high-value stock where internal monitoring and oversight are technically complex.