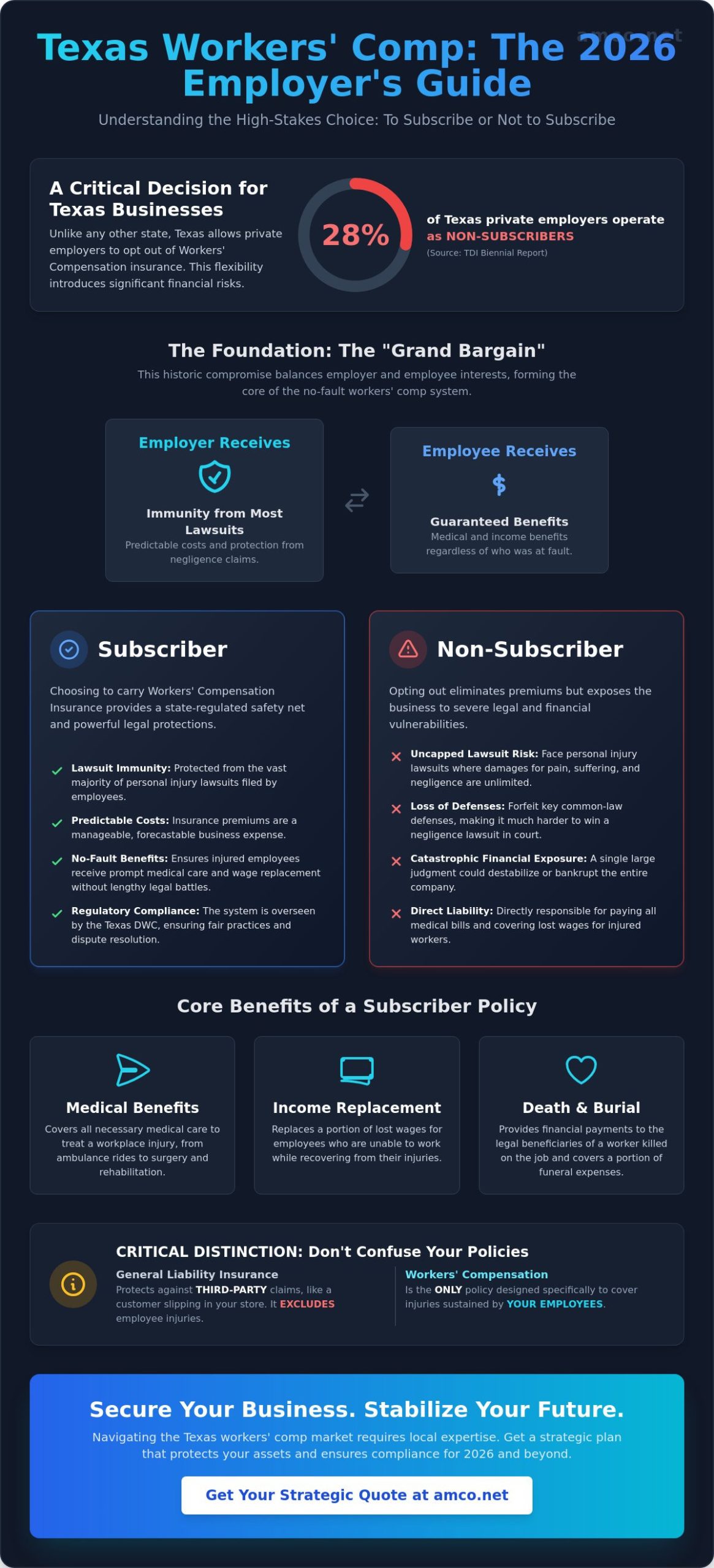

Did you know that as of the most recent Texas Department of Insurance (TDI) biennial report, nearly 28% of private employers in the state operate as non-subscribers, leaving them vulnerable to uncapped personal injury lawsuits? While the flexibility of the Texas system offers choices, it also introduces significant financial risks that can destabilize even the most robust operations. Managing Workers Compensation Insurance requires more than just paying premiums; it demands a strategic understanding of how to protect your assets from the rising costs of workplace injuries. We recognize that for local businesses, especially in demanding sectors like trucking or manufacturing, the fear of unpredictable litigation and complex annual audits is a constant concern.

This 2026 guide offers the professional clarity you need to master these complexities and secure your company's future. You'll gain actionable insights into cost saving strategies that align with current TDI regulations and learn how to maintain legal protection against employee lawsuits. We'll outline the specific steps to stabilize your insurance expenses and ensure your business remains compliant and profitable throughout the coming year. By focusing on long term stability rather than short term fixes, you can transform your insurance policy from a burden into a reliable safety net.

Workers Compensation Insurance functions as a no-fault system designed to provide medical care and income replacement for employees injured on the job. This framework originated from a legislative compromise known as the "Grand Bargain." Under this agreement, workers receive guaranteed benefits without needing to prove employer negligence. In return, employers receive immunity from most personal injury lawsuits. To understand the broader context of Workers' compensation in the United States, it's helpful to look at how these laws evolved to balance economic stability with worker safety. Texas codified its version of this system with the passage of the Workers' Compensation Act in 1913.

To better understand how this system protects your business and staff, watch this brief overview from Texas Mutual:

Texas stands apart from the other 49 states. It's the only jurisdiction where private employers can choose not to carry coverage. These businesses are called "non-subscribers." While opting out might seem like a cost-saving measure, it strips away the legal protections of the Grand Bargain. Non-subscribers face significant financial risk because they can be sued by injured employees for negligence, and they lose traditional legal defenses like "contributory negligence."

The Texas Department of Insurance, Division of Workers' Compensation (DWC) regulates the industry to ensure the system remains fair and functional. They monitor insurance carriers, health care providers, and employers to maintain compliance. When disputes arise regarding benefits or medical necessity, the DWC provides a formal resolution process. Employers have strict reporting duties; for instance, you must file the Employer's First Report of Injury (DWC Form-001) by the 8th day of the following month after a worker's injury results in more than one day of lost time. The DWC serves as the primary regulatory authority ensuring that Texas businesses comply with state-mandated reporting and benefit standards.

Many business owners mistakenly assume a General Liability Insurance policy covers staff injuries. It doesn't. General liability protects against third-party claims, such as a customer slipping on a wet floor. It specifically excludes injuries to your own employees. Relying on liability policies leaves a massive gap in your risk management strategy. Additionally, Surety Bonds serve a different financial purpose entirely. They act as a three-party guarantee for contractual performance rather than providing medical or wage benefits for injured workers. Workers Compensation Insurance remains the only reliable way to manage the specific costs associated with workplace accidents and occupational diseases.

Workers Compensation Insurance provides a critical safety net that stabilizes both the workforce and the company's financial health. In Texas, this coverage is designed to address the immediate and long-term consequences of workplace injuries. It functions as a "no-fault" system, meaning benefits are paid regardless of who caused the accident, which prevents many costly legal disputes. For an employer, the policy covers everything from the initial ambulance ride to complex surgical procedures and subsequent recovery phases.

Beyond medical care, the policy addresses the human cost of industrial accidents. If a worker loses their life due to a job-related incident, the insurance provides death benefits to legal beneficiaries and covers burial expenses. For those in these hazardous roles seeking additional personal security, Special Risk Term offers specialized life insurance solutions that account for high-risk occupations. Crucially, the workers' comp policy also includes Employer Liability coverage. This part of the policy is essential for risk management because it funds legal defense costs if an employee or their family sues the business for gross negligence, a risk that 15% of Texas employers cited as a primary concern in recent industry surveys.

Texas law mandates coverage for all "reasonable and necessary" medical care related to a workplace injury. This isn't limited to hospital stays; it includes prescriptions, medical equipment, and diagnostic testing. The Texas Department of Insurance oversees these standards to ensure injured workers receive appropriate care. For catastrophic injuries, such as those involving the loss of limb or severe burns, the "lifetime medical benefits" rule ensures the insurer pays for related treatments for the rest of the employee's life. If an employee can't return to their previous role, vocational rehabilitation benefits help them train for new positions within the workforce.

Income benefits are calculated based on the employee's Average Weekly Wage (AWW), which is the average amount earned during the 13 weeks prior to the injury. Temporary Income Benefits (TIBs) replace approximately 70% to 75% of lost wages while the worker recovers. Once a doctor determines the worker has reached Maximum Medical Improvement (MMI), they receive an impairment rating. This rating dictates the duration of Impairment Income Benefits (IIBs). Under Texas statutes, TIBs generally end after 104 weeks, though the transition to IIBs or Supplemental Income Benefits (SIBs) ensures continued support for those with permanent limitations.

Ensuring your facility meets safety standards is the first step in reducing these claims. Maintaining a secure environment is part of a complete industrial solution that protects your team and your long-term profitability. Safeguarding your physical assets against Texas's extreme weather events with adequate Commercial Property Insurance is an equally important layer of your overall business protection strategy.

Texas remains unique in the United States as the only state where private employers can choose whether to carry Workers Compensation Insurance. This choice, known as non-subscription, allows companies to bypass the state-regulated system. While the initial appeal lies in avoiding premium costs, the long-term financial exposure often outweighs any short-term savings. According to the Texas Department of Insurance guide to workers' compensation, employers who opt out must still report their non-subscriber status and workplace injuries to the state. Failing to provide coverage doesn't remove the employer's liability; it changes the legal landscape entirely.

The most dangerous consequence of opting out is the loss of common-law defenses in a personal injury lawsuit. In a standard legal environment, an employer might argue that an employee's own negligence contributed to their injury. As a non-subscriber, you lose this "contributory negligence" defense. You also cannot claim that the employee assumed the risk of a dangerous job or that a coworker caused the accident. If the employee proves even 1% of the employer's negligence, the employer may be held liable for 100% of the damages. In 2026, litigation trends in Austin and San Antonio show a marked increase in jury awards for workplace injuries. A single catastrophic event can easily bankrupt a small to mid-sized firm when these legal protections are absent.

Large corporations in Dallas and Houston typically choose to be subscribers because the state system provides statutory immunity. This means employees generally cannot sue their employer for negligence, regardless of the injury's severity. Predictable premium costs and administrative ease make subscription a strategic business decision for risk management. Conversely, non-subscribers often turn to alternative occupational accident plans. These private policies might seem cheaper, but they frequently include benefit caps and don't provide the same legal shield as Workers Compensation Insurance. They leave the business's assets vulnerable to unlimited court judgments. A comprehensive risk management strategy should also account for third-party claims by pairing workers' comp with a robust General Liability Insurance policy for Texas business owners to close any remaining coverage gaps.

Approximately 80% of the Texas payroll is covered by subscribers because the legal immunity and financial certainty provided by the state-regulated system offer a more stable foundation for long-term industrial growth.

Such stability is a key asset when it comes time to value or sell your company. In the North Texas market, Bravo Kilo Advisors works with business owners to ensure their operational strengths are reflected in a professional appraisal and strategic exit plan.

Determining the exact cost of Workers Compensation Insurance requires an understanding of three primary variables: your industry classification, your total gross payroll, and your historical safety record. In Texas, the Department of Insurance (TDI) monitors rate filings, but individual carriers set their own prices based on these factors. The standard formula follows a simple logic: (Class Code Rate x [Payroll / 100]) x Experience Modifier = Total Premium. For 2026, Texas remains a competitive market, yet businesses in high-risk sectors must be diligent in their reporting to avoid unnecessary surcharges.

The National Council on Compensation Insurance (NCCI) assigns specific four-digit codes to every job type. These codes reflect the statistical likelihood of an injury occurring in that role. For instance, commercial trucking insurance Houston clients typically see higher base rates than professional services because of the physical risks associated with logistics and heavy machinery. In 2026, accurate classification is your best defense against overpayment.

Your Experience Modifier, or E-Mod, is a multiplier that rewards or penalizes your business based on claims history. A 1.0 rating is considered the industry average. If your E-Mod is 0.85, you're receiving a 15% discount on your Workers Compensation Insurance. Conversely, a 1.20 rating means you're paying a 20% penalty. This figure is calculated using a rolling three-year window, excluding the most recent year.

Proactive safety is the most effective way to lower this number. Implementing a formal "return-to-work" program can reduce the "indemnity" portion of a claim, which weighs more heavily on your E-Mod than medical-only claims. Statistics from 2025 show that Texas companies with active safety committees saw a 12% average reduction in claim frequency within 24 months. Focusing on long-term safety culture isn't just about compliance; it's a direct strategy for cost optimization.

Preparing for the annual audit shouldn't be a source of stress. Keep your payroll records, 941 forms, and subcontractor certificates of insurance organized throughout the year to ensure your final premium matches your actual exposure. If you're looking to refine your safety protocols or review your current classification, we can help.

Request a professional insurance audit and consultation today.

AMCO.NET has served as a technical advisor and risk management partner for Texas businesses since 1987. With a physical presence and deep historical data from markets in Houston, Dallas, and San Antonio, we understand the specific challenges of the local regulatory environment. Texas is the only state that allows private employers to opt out of the system, but for those who choose to provide coverage, the complexity of Workers Compensation Insurance requires more than a generic policy. We provide the stability and professional oversight necessary to maintain compliance while protecting your bottom line.

Our expertise is particularly valuable for high-risk Texas industries. We don't rely on a single provider. Instead, we leverage our relationships with multiple specialized carriers to find the most competitive rates for trucking companies, oil field contractors, and construction firms. This multi-carrier approach ensures that even businesses with high experience modifiers can find sustainable coverage options. Our team integrates your workers' comp into a broader business protection plan, aligning it with your general liability and commercial auto policies to eliminate dangerous coverage gaps. For businesses that also need to protect their physical facilities and equipment from Texas's severe weather events, our guide to Commercial Property Insurance in Houston and Texas outlines the critical coverage decisions every business owner should make in 2026. For a broader perspective on managing all your business and personal policies in the region, our comprehensive guide to insurance in Houston, TX covers the full 2026 landscape of coverage options available to local businesses and residents.

Selecting a local insurance company near me provides a level of advocacy that direct carriers simply cannot offer. While a direct insurer represents their own underwriting interests, an independent broker represents you. This distinction is critical during annual premium audits or when a claim is disputed. We act as your professional intermediary, ensuring that job classifications are accurate and that you aren't overpaying for your risk profile.

In specialized logistics hubs like Laredo or energy-intensive regions like Midland, having a dedicated agent who knows the local labor market is a strategic asset. We offer several advantages over direct-to-consumer models:

Securing an accurate Workers Compensation Insurance quote requires precise data. To expedite the process, you'll need your Federal Employer Identification Number (FEIN), a detailed breakdown of your estimated annual payroll, and your current NCCI class codes. If you've had coverage previously, having your "loss runs" from the last three to five years will help us secure the best possible tiering.

Our quoting process is designed for the modern business owner. We combine digital-friendly data collection with the nuanced insight of a human expert. You won't be funneled through an automated call center. Instead, you'll speak with a professional who understands the Texas labor code and the specific risks of your industry. Protect your Texas business and employees with an AMCO Workers' Comp quote today.

Choosing the right coverage isn't just a regulatory checkbox; it's a foundational step for business continuity in 2026. Texas remains the only state where coverage is optional, yet businesses that forgo Workers Compensation Insurance face unlimited legal liability in employee injury lawsuits. Since 1987, our team has specialized in navigating these unique state statutes to shield employers from catastrophic financial loss. Whether you operate in high-risk sectors like construction or manage a large trucking fleet, localized expertise ensures your policy matches your specific risk profile.

With physical offices in Houston, Dallas, and San Antonio, we provide the boots-on-the-ground support necessary to manage claims efficiently. You don't have to navigate these complex 2026 requirements alone. Partnering with a seasoned agency allows you to focus on growth while we handle the technical details of your liability protection. For those who want to eventually leverage that growth into a successful exit, learn more about Bravo Kilo Advisors and their business brokerage expertise.

Get a Fast Workers' Compensation Quote for Your Texas Business

We look forward to securing your company's future together.

Texas remains the only state in the U.S. where private employers can choose not to carry workers compensation insurance. While the Texas Labor Code doesn't mandate coverage for most private businesses, public employers and those entering government contracts must maintain it. Businesses that opt out are classified as nonsubscribers and must file annual notices with the Texas Department of Insurance to remain compliant with state regulations.

Premiums depend on your industry classification and payroll, but the Texas Department of Insurance reported an average premium rate of $0.37 per $100 of payroll in 2023. For a small business in Houston with a $500,000 annual payroll, this equates to roughly $1,850 per year before adjustments. Rates vary significantly between a low-risk office environment and high-risk sectors like industrial packaging or construction. Understanding how these costs fit within your overall insurance in Houston budget is essential for accurate financial planning in 2026.

Employers without coverage lose their common law defenses in personal injury lawsuits, meaning they can't argue the employee was negligent. According to the Texas Department of Insurance, 18% of Texas private employers were nonsubscribers in 2022. These businesses face unlimited financial liability for medical expenses and lost wages if a court finds them even 1% at fault for a workplace injury. It's a significant risk to long term stability. Protecting that stability is a priority for business owners, and Bravo Kilo Advisors can provide the necessary guidance for those looking to evaluate or sell their company in the North Texas region.

Sole proprietors and partners aren't automatically covered under Texas law, but they can elect to include themselves on a policy. You've got to provide written notice to your insurance carrier to secure this coverage. Independent contractors are generally responsible for their own insurance, though 2023 DWC guidelines state that general contractors may be held liable for injuries if they don't ensure their subcontractors have active policies.

Workers' compensation serves as the exclusive remedy for workplace injuries, which generally prevents employees from suing their employer for negligence. This legal protection provides long term security for your business operations. The only exception occurs in cases of gross negligence resulting in a fatal injury, where the Texas Constitution allows surviving family members to seek exemplary damages despite the existence of a policy. For families seeking additional peace of mind, Special Risk Term helps those in high-risk fields secure life insurance even if they have been previously declined.

An audit is a mandatory annual review where the insurer verifies your actual payroll and job classifications against your initial estimates. To prepare, organize your 941 tax forms, payroll records, and subcontractor certificates of insurance from the previous 12 months. Accurate record keeping ensures you don't pay unnecessary premiums and helps maintain the cost optimization of your workers compensation insurance program.

Employers must report any injury that results in more than one day of lost work to the Texas Division of Workers' Compensation using Form DWC-001. You've got 8 days from the date of the injury or the date you were notified to submit this documentation. Failing to meet this 8 day deadline can result in administrative penalties and fines from the state regulatory body, impacting your professional standing.

Workers' compensation provides statutory benefits and full legal immunity from most lawsuits, whereas occupational accident insurance is a private contract with capped benefits. Occupational accident policies don't provide the exclusive remedy protection found in the Texas Labor Code. While private plans might offer lower initial costs, they leave businesses exposed to personal injury litigation that could jeopardize technical continuity and financial security.