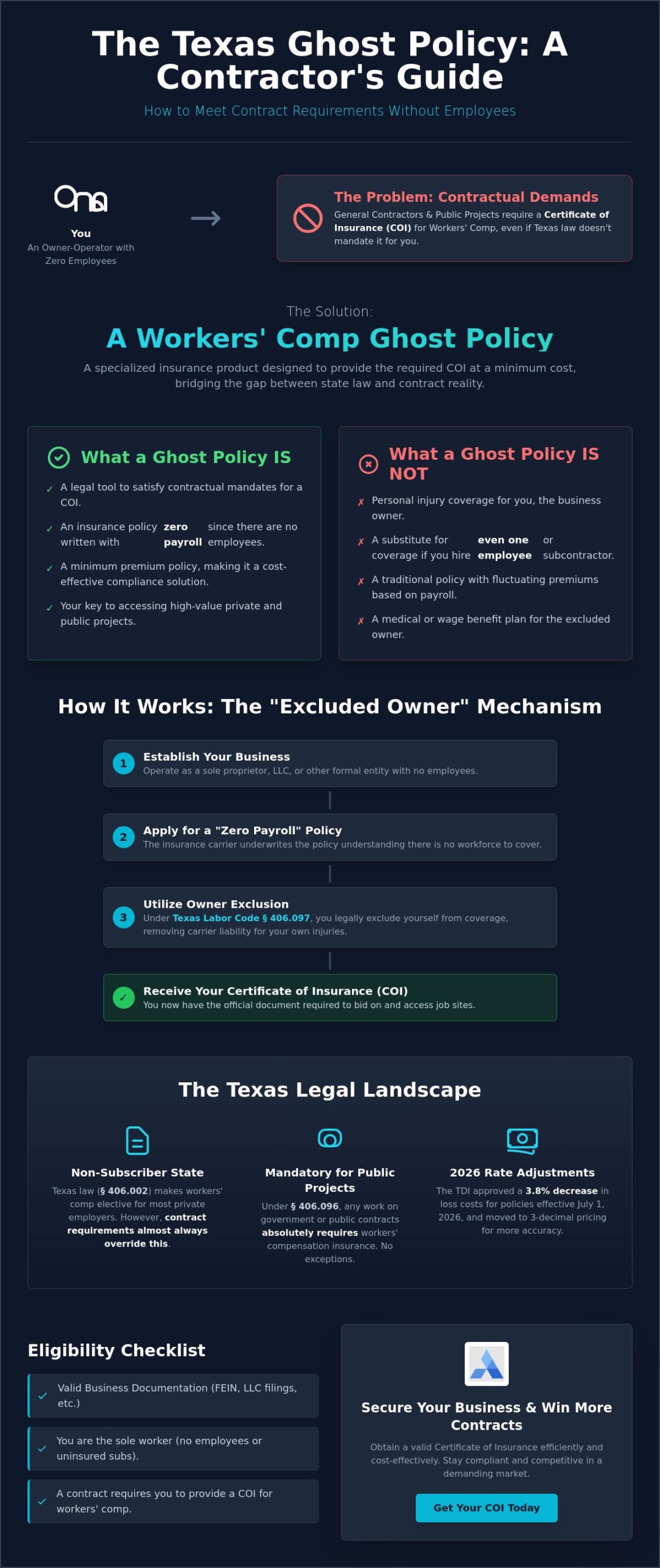

In 2026, the difference between winning a high-value project and being dismissed at the bidding stage often comes down to a single piece of paper you might not technically need for your own protection. You've likely realized that while Texas law generally allows private employers to opt out of coverage, your general contractors view a Certificate of Insurance as a non-negotiable requirement. It's a common frustration to face high premium quotes for traditional policies when you have no employees to cover. This guide demonstrates how to secure a workers comp ghost policy Texas to satisfy these rigid contract demands while keeping your insurance overhead at a minimum.

Securing this specific endorsement allows you to bridge the gap between Texas's flexible regulations and the strict liability standards of modern job sites. We'll explore the legal framework of owner exclusions under Labor Code § 406.097 and how the July 1, 2026, rate adjustments impact your bottom line. You'll learn the exact process for obtaining a valid COI quickly, ensuring your business remains compliant and competitive without paying for coverage you don't require. This systematic approach provides the technical background and functional steps necessary to maintain your professional standing in a demanding market.

A workers comp ghost policy Texas is a specialized insurance arrangement designed for business owners who have no employees but require proof of coverage to secure contracts. While the broader Workers' compensation system is typically designed to provide medical and wage benefits to staff, this policy serves a purely administrative function. It provides a valid Certificate of Insurance (COI) without the high costs associated with standard payroll-based policies. This allows sole proprietors to meet the stringent safety and liability standards required by modern project owners.

Unlike traditional coverage, a ghost policy carries a "zero payroll" rating because it specifically excludes the owner from any benefits. This distinction is critical for independent contractors who operate alone. The insurance carrier issues the policy with the understanding that they won't pay out claims, as there is no covered workforce. It acts as a bridge between the business owner's need for contract eligibility and the insurance carrier's need for a defined risk profile. It solves the compliance gap efficiently.

To better understand this concept, watch this helpful video:

This policy type differs significantly from traditional workers' comp intended for businesses with staff. In a standard setup, premiums fluctuate based on the actual payroll and the risk classification of the employees. With a ghost policy, the risk is static and minimal because the carrier is essentially providing a certificate rather than active medical coverage. It's a strategic tool for maintaining professional standing without the financial burden of full-scale insurance.

The term "ghost" refers to the fact that the policy exists legally on paper but provides coverage for zero individuals. Under Texas Labor Code § 406.097, a sole proprietor or corporate officer can be legally excluded from coverage through a specific endorsement. This exclusion removes the carrier's liability for the owner's potential workplace injuries. These policies are generally written as minimum premium policies because there is no actual payroll to calculate against.

Texas is a "non-subscriber" state where workers' comp is generally elective under Labor Code § 406.002. However, private contract requirements often override this elective freedom, making coverage mandatory for site access. The Texas Department of Insurance (TDI) regulates these filings and approved a 3.8% decrease in loss costs for policies starting on or after July 1, 2026. TDI also moved to a three-decimal place calculation for rates to ensure higher pricing precision. For a contractor, this means the workers comp ghost policy Texas remains the most efficient way to satisfy a contract while staying within the legal framework.

While Texas law provides the flexibility of non-subscription for most private employers, the commercial marketplace operates on much stricter standards. For an independent contractor or owner-operator in Houston or Dallas, the decision to opt out of coverage isn't just a legal choice. It's often a barrier to entry. Most project owners and general contractors view the absence of a Certificate of Insurance (COI) as an unacceptable liability risk. Obtaining a workers comp ghost policy Texas allows you to bypass this barrier by providing the specific documentation required to set foot on a professional job site.

The necessity becomes even more apparent when bidding on public projects. Under Texas Labor Code § 406.096, any contractor working on a government or public contract must have workers' compensation insurance. This is a mandatory requirement that cannot be waived. Without a policy in place, your bid will likely be disqualified regardless of your technical expertise or pricing. A ghost policy ensures you remain eligible for these lucrative municipal and state-level opportunities while keeping your operational costs predictable. It's a strategic investment in your firm's growth and professional credibility.

General contractors in Texas face significant financial risks when hiring uninsured subcontractors. If a subcontractor is injured and lacks coverage, the GC's own insurance carrier may be held responsible for the claim. This often leads to "uninsured subcontractor" surcharges during the GC's annual premium audit. To avoid these costs, GCs strictly require a COI from every vendor. A workers comp ghost policy Texas closes this insurance gap. It provides the GC with the peace of mind that your business is formally accounted for within the workers' compensation system, even if you are the only person on the policy.

In the logistics sector, owner-operators frequently work under lease agreements with larger motor carriers. These carriers typically require proof of workers' compensation to satisfy their own safety and compliance departments. While many drivers utilize occupational accident insurance for personal protection, a ghost policy is often the only document that satisfies the formal "workers' comp" line item in a contract. If you are managing a fleet or operating as a solo driver, coordinating this with your commercial trucking insurance Houston ensures you meet all regulatory and contractual obligations simultaneously.

Protecting the hiring party from liability is a fundamental aspect of modern business relationships. By maintaining a policy, you demonstrate that you understand the operational risks of your industry. If you need assistance navigating these requirements, you can consult with a specialist to find the right balance of compliance and cost efficiency for your specific trade.

The operational framework of a workers comp ghost policy Texas relies on a specific legal maneuver known as an owner exclusion. While the policy document itself looks like a standard workers' compensation agreement, it includes a formal endorsement that removes the business owner from the carrier's liability. This mechanism is what allows the policy to be rated at zero payroll. The insurance carrier provides a valid policy number and maintains a professional file, but they do so with the explicit agreement that no benefits will be paid to the individual named on the exclusion form. This results in the generation of a Certificate of Insurance (COI) that satisfies the most rigid contract requirements.

A significant misunderstanding persists regarding the protection these policies provide. The primary misconception is that a ghost policy offers medical or wage replacement benefits for the owner if they're injured on a job site. It doesn't. This policy is strictly a compliance instrument. If you hire a temporary helper or a day laborer even for a single afternoon, the policy's nature changes. During a premium audit, the carrier will identify that payroll was paid and adjust your costs accordingly. While an injury to that temporary worker might be covered, you as the owner remain permanently excluded from the policy's benefits.

The exclusion endorsement is the cornerstone of this arrangement in the Texas market. By filing this form, the sole proprietor or corporate officer confirms they're opting out of the policy's benefits. This legal step is what triggers the minimum premium rating because the carrier's exposure is theoretically zero. This policy exists for compliance, not personal health protection. It provides the necessary documentation to enter a job site without the financial burden of a standard policy. It's the most professional way to handle the gap between state law and private contract demands.

Despite the exclusion of the owner, the policy still serves a vital function for the business entity. It acts as a safety net for statutory employees. These are individuals whom the state might deem your employees even if you consider them independent contractors. If a claim is filed against your business by an uninsured subcontractor or a temporary worker, the policy provides legal defense costs. This protection ensures that the business entity itself isn't bankrupted by legal fees or unexpected liability claims. It's a fundamental layer of security that maintains the integrity of your professional operations.

Establishing eligibility for a workers comp ghost policy Texas requires a precise verification of your business structure and workforce. The primary qualification is that the entity must have zero employees. This definition includes not only full-time staff but also part-time, seasonal, or casual laborers. If you utilize any form of payroll for workers, you're ineligible for a ghost policy and must seek a traditional policy instead. Once you've confirmed your solo status, the process moves into the documentation phase.

You'll need to gather essential business credentials to proceed with an application. This typically includes your Federal Employer Identification Number (FEIN), any "Doing Business As" (DBA) filings, or LLC and incorporation paperwork. These documents verify the legal existence of your business and provide the carrier with the necessary data for underwriting. Following this, you must complete the Texas-specific owner exclusion forms. These documents formally notify the carrier that you're waiving your right to benefits. Once the minimum premium is paid, the carrier issues the Certificate of Insurance (COI) that allows you to start work.

The annual audit is a standard procedure for every workers' compensation policy in the state, including those with zero payroll. Carriers conduct these audits to ensure that the initial payroll estimates remain accurate throughout the policy term. To maintain your status and avoid unexpected premium increases, you must provide clear evidence of zero payroll. This involves submitting tax documents or ledger reports that show no wages were paid to employees. It's equally important to keep detailed records of all 1099 payments made to subcontractors. If these subcontractors don't have their own insurance, the auditor may attempt to charge their labor against your policy.

The pricing for a workers comp ghost policy Texas is dictated by "Minimum Premiums" established by individual carriers. These rates are influenced by National Council on Compensation Insurance (NCCI) class codes, which categorize the risk level of your specific trade. For example, a clerical consultant typically faces lower base rates than an oilfield subcontractor in Midland or a structural contractor in Houston. Regional risk factors and the specific nature of your operations determine where your business falls within the carrier's pricing structure. Effective July 1, 2026, the TDI approved a 3.8% average decrease in loss costs, which may influence the competitive landscape for these minimum premium policies.

If you're ready to secure your compliance documentation and bid on larger contracts, request a quote today to find a policy tailored to your specific industry class code.

With more than 35 years of operational history in the Houston and broader Texas insurance markets, AMCO.NET provides the stability and specialized knowledge required to navigate complex compliance requirements. We don't just offer products; we deliver integrated system solutions that protect your commercial interests. Our team maintains established relationships with "A" rated carriers that understand the technical nuances of a workers comp ghost policy Texas. This ensures that the Certificate of Insurance you receive is backed by a reputable institution and will be accepted by any general contractor or government entity in the state.

The regional differences between Houston, Dallas, and San Antonio business environments require a provider who understands local job site standards. We specialize in bundling Workers Compensation Insurance with other essential commercial coverages to streamline your administrative overhead. This holistic view of your risk profile allows us to provide direct support during mandatory policy audits, ensuring your records are presented clearly to maintain your zero-payroll status. We also manage your COI renewals automatically, so you never lose site access due to an expired document.

Time is a critical factor when a contract is on the line. We provide fast turnaround times for contractors who need to satisfy insurance requirements immediately to begin work. Our digital infrastructure, including the AMCO app, allows for easy management of your documents and policy details directly from the field. You can Request your Workers’ Comp Ghost Policy quote from AMCO.NET to secure the professional standing your business deserves. We remain committed to your long term success through consistent support and industry leading expertise.

Navigating the intersection of Texas labor laws and private project requirements doesn't have to be a financial burden for solo operators. By utilizing a workers comp ghost policy Texas, you secure the necessary documentation to access restricted job sites while maintaining your status as a lean, efficient operation. This strategic approach ensures you aren't paying for coverage you legally exclude yourself from, allowing you to allocate those resources back into your business growth and equipment. It provides the technical bridge between elective state regulations and the mandatory standards of high-value contracts.

Establishing this foundation requires a partner who understands the specific operational risks of the Houston construction and trucking sectors. AMCO.NET has been serving Texas businesses since 1987, providing access to A+ Rated Insurance Carriers that specialize in these unique compliance tools. We ensure your documentation is technically sound and ready for any audit or project bid. Get a Fast Workers’ Comp Ghost Policy Quote from AMCO.NET and position your business for the most lucrative contracts available in 2026. Your professional credibility is the key to long-term stability and market success.

A workers comp ghost policy Texas is entirely legal and operates under the authority of Texas Labor Code § 406.097. This specific statute provides the mechanism for business owners to exclude themselves from coverage through a formal endorsement. While Texas is a non-subscriber state, this policy serves as a recognized method for solo contractors to maintain a professional standing with insurance carriers while meeting the rigid liability standards of the commercial marketplace.

A ghost policy doesn't provide medical or wage replacement benefits for the business owner. Because you must sign a legal exclusion form to obtain this policy, you're effectively waiving your right to collect benefits from the carrier. The policy's function is purely administrative, designed to generate proof of insurance for contract compliance. You should maintain separate health or occupational accident insurance if you need personal protection for work-related injuries.

The cost of this policy is determined by the "minimum premium" set by the insurance carrier rather than a percentage of payroll. Since there's no covered workforce, carriers charge a flat base rate to maintain the policy and provide the Certificate of Insurance. These rates vary depending on your specific industry classification and the risk profile of your trade. Carriers in the Texas market establish these minimums to cover their administrative and legal defense costs.

You can't maintain a ghost policy if you employ any staff, including part-time or casual laborers. This insurance solution is strictly reserved for business entities with zero payroll. If you hire a helper for even a few days, your policy must be converted to a traditional workers' compensation plan. Carriers verify your payroll status during the mandatory annual audit, and failing to report employees can lead to significant premium adjustments and legal complications.

The primary difference lies in the payroll rating and the scope of coverage. A traditional policy is calculated based on employee wages and provides active benefits to the workforce. Conversely, a workers comp ghost policy Texas carries a zero payroll rating and excludes the owner from all benefits. While a traditional policy protects employees, a ghost policy is a strategic tool used by solo contractors to satisfy the documentation requirements of general contractors and project owners.

Securing a Certificate of Insurance typically takes between 24 and 48 hours once all business documentation is submitted. The process involves verifying your legal entity status and completing the required owner exclusion forms. Because these policies are standardized for solo operators, the underwriting timeline is significantly shorter than for complex payroll-based plans. This speed is essential for contractors who need to meet immediate bidding deadlines or secure site access on short notice.

Most general contractors in Texas accept a ghost policy because it provides a valid Certificate of Insurance and a policy number. The GC's primary concern is avoiding uninsured subcontractor surcharges during their own premium audits. By providing a valid COI, you demonstrate that your business is formally registered within the workers' compensation system. This document satisfies the liability requirements of most private contracts and public projects in major cities like Houston and Dallas.

If you hire an employee after obtaining a ghost policy, you're required to notify your insurance carrier immediately. The policy must be updated to include payroll, which will transition it into a traditional workers' compensation plan. If you wait until the annual audit to disclose this change, the carrier will backdate the premiums based on the wages paid. Failing to report new hires can also leave your business exposed to significant liability if an injury occurs before the policy is updated.