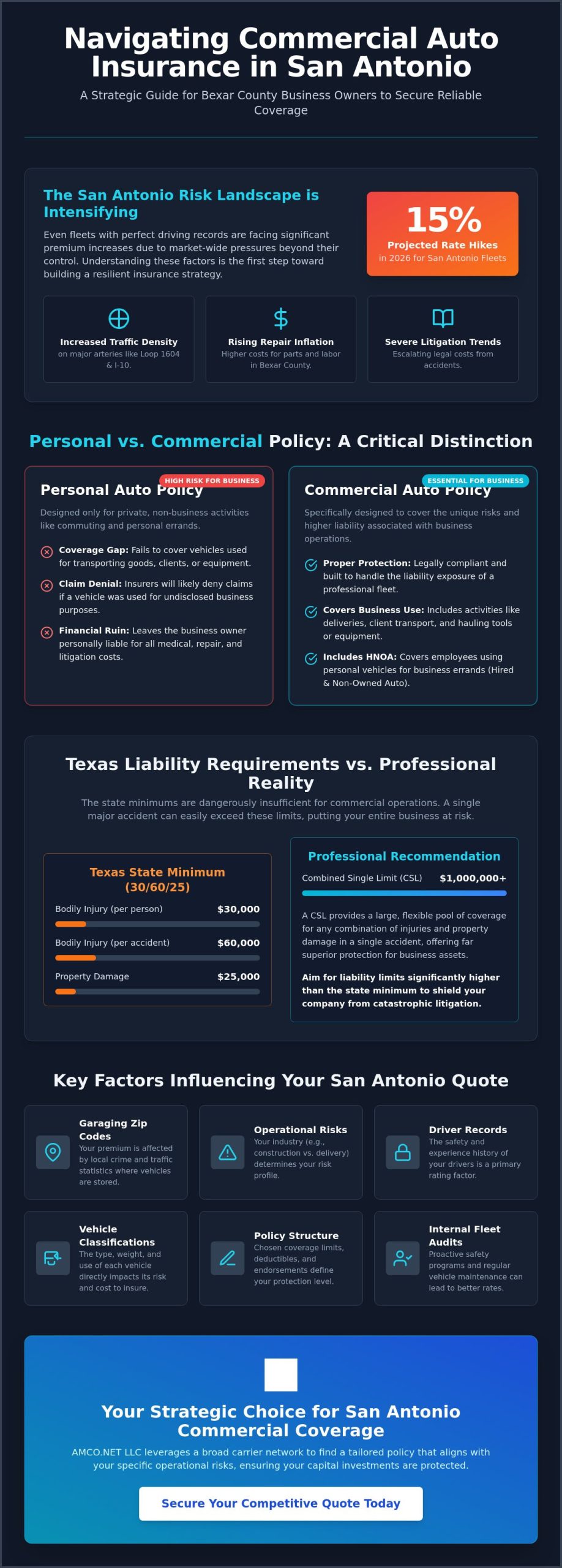

Did you know that even San Antonio fleets with spotless driving records are facing insurance rate hikes of up to 15% in 2026? As litigation severity and repair inflation climb across Bexar County, securing accurate commercial auto insurance quotes San Antonio business owners can rely on has become a complex financial necessity. It's frustrating to maintain a safe operation only to see premiums rise due to regional market pressures you can't control.

We recognize that protecting your enterprise requires more than just meeting the Texas state minimum liability of 30/60/25. This guide provides a professional framework to help you secure competitive quotes while ensuring your assets remain protected under the latest regulatory standards. We'll examine the impact of the new HB 2067 transparency law, analyze the recent TAIPA rate adjustments, and outline the specific steps required to eliminate dangerous coverage gaps in your commercial policy.

Commercial auto insurance is a specialized legal contract designed to protect vehicles used for business operations. It differs fundamentally from personal auto insurance because it addresses the distinct risks associated with corporate activities, such as transporting goods, hauling equipment, or carrying passengers for a fee. Understanding the Necessity of Commercial Auto Insurance is the first step for any Bexar County business owner looking to secure accurate commercial auto insurance quotes San Antonio providers offer. A personal policy simply isn't built to handle the liability exposure of a professional fleet.

The risk landscape in San Antonio is particularly demanding. With ongoing massive infrastructure projects and increasing traffic density on major arteries like Loop 1604 and I-10, the probability of road incidents has climbed. When a vehicle is engaged in business tasks, the financial stakes of an accident are significantly higher than in a private setting. This environment makes it essential to distinguish between personal use and commercial necessity before a claim occurs.

To better understand this concept, watch this helpful video:

Operating without the correct policy classification can lead to severe legal and financial consequences. The Texas Department of Insurance sets strict standards for policy definitions. If an insurer determines that a vehicle was being used for undisclosed business purposes at the time of a collision, they'll likely deny the claim. This leaves the business owner personally responsible for medical bills, vehicle repairs, and potential litigation costs, which can easily bankrupt a small enterprise.

Business activities that trigger the need for commercial coverage include making deliveries, transporting clients, or hauling heavy tools and materials. For San Antonio contractors and service providers, the vehicle is often a mobile workshop; this usage requires a commercial designation. There's also a critical nuance known as Hired and Non-Owned Auto (HNOA) coverage. This is essential if your employees ever use their personal vehicles for business errands, such as visiting a job site in Stone Oak or picking up supplies in the Pearl District, as it protects the business from liability if they're involved in an accident.

Texas law mandates minimum liability limits of 30/60/25, which translates to $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. While these figures satisfy the legal baseline, they're often insufficient for commercial entities. A single multi-vehicle accident in a high-traffic San Antonio corridor can quickly surpass these limits. Many professionals prefer a Combined Single Limit (CSL) approach, which provides a flexible, larger pool of coverage for any combination of injuries or property damage. Texas businesses should aim for liability limits significantly higher than the state minimum to ensure corporate assets remain shielded from catastrophic litigation.

When you request commercial auto insurance quotes San Antonio agents provide, you should evaluate how these limits interact with your specific industry risks. Choosing the right coverage foundation today prevents a total loss of business continuity tomorrow.

Understanding the Key Coverage Components in a San Antonio Commercial Auto Policy ensures that your business doesn't just meet a legal requirement but actually survives a major incident. When you request commercial auto insurance quotes San Antonio agents provide, the quote's structure depends on several specific layers of protection. These components work together to shield your business from the financial fallout of accidents, theft, or environmental damage.

Bodily Injury and Property Damage Liability form the primary pillars of any professional policy. They pay for other people's medical expenses or vehicle repairs if your driver is at fault in a collision. Without sufficient limits, a single incident on a busy stretch of I-35 could expose your company's entire cash reserve to legal claims. Physical Damage Coverage is equally vital for protecting your own assets. San Antonio's unpredictable weather, ranging from sudden hailstorms to localized flash flooding, makes comprehensive and collision coverage essential for preserving your capital investment.

In high-density urban zones like Bexar County, Uninsured and Underinsured Motorist Coverage is a prudent addition. It steps in when the other party lacks sufficient insurance to cover your damages. Additionally, Medical Payments and Personal Injury Protection (PIP) help cover immediate medical costs for your drivers and passengers, regardless of who caused the accident. This ensures your team receives care without waiting for lengthy legal determinations.

San Antonio's diverse economy requires more than a one-size-fits-all approach. Logistics and transport firms often require Inland Marine or Cargo insurance to protect high-value goods moved across Texas. For the construction and HVAC sectors, loading and unloading coverage is essential to address risks that occur while moving equipment from the vehicle to a job site. You might also consider rental reimbursement and downtime coverage to ensure that a single damaged vehicle doesn't halt your daily revenue stream. You can evaluate these specialized coverage options with a professional broker to see which fits your specific operational model.

The deductible you choose acts as a primary lever for managing your fixed costs. There's a direct, inverse relationship between your out-of-pocket deductible and your monthly premium. Selecting a $2,500 deductible instead of a $1,000 deductible will significantly lower the annual cost of a standard San Antonio commercial fleet quote, but it requires higher immediate liquidity in the event of a claim. It's about finding the right balance between daily cash flow and long-term risk tolerance.

A professional insurance quote is the result of a precise risk calculation, not a random estimate. When you request commercial auto insurance quotes San Antonio providers generate, they analyze several variables specific to your local operations. These factors determine the stability of your premiums and the long term viability of your coverage. Understanding these levers allows you to better manage your fixed operational costs.

The "Garaging Zip Code" is a primary factor. A fleet parked in a high traffic or high crime district in the city center faces different actuarial risks than one stored in a lower density area like Helotes or Somerset. Insurers also prioritize vehicle classification. Light duty trucks and service vans carry different risk profiles than heavy duty commercial haulers. These classifications often align with federal Factors Influencing Commercial Auto Insurance Quotes, which dictate higher coverage floors for heavier equipment and specialized cargo.

Your radius of operation is another critical lever. Local San Antonio routes within a 50 mile radius generally attract more competitive rates than long haul transport crossing state lines. Finally, the human element cannot be ignored. Driver Motor Vehicle Records (MVRs) remain a significant cost driver. A single speeding ticket or at fault accident on a driver's record can inflate your premium, emphasizing the need for rigorous internal hiring standards.

Local infrastructure directly impacts accident frequency. Constant congestion on I-10 and I-35 contributes to higher collision rates, which insurers price into every Bexar County policy. Central Texas also presents unique environmental risks. Seasonal weather, including severe hail and flash flooding, leads to frequent comprehensive claims. Additionally, local crime statistics for vehicle theft in specific industrial zones can influence the cost of protecting your physical assets.

Industry risk ratings create significant variance in your final quote. A plumbing fleet carrying standard tools is rated differently than a unit transporting hazardous materials or heavy machinery. If your business operates 24/7, your risk profile increases compared to fleets that only run during standard daylight hours. For those moving goods between major Texas hubs, commercial trucking insurance Houston insights provide a valuable perspective on the long haul risks that also apply to San Antonio operators navigating the I-10 corridor.

Securing the most competitive commercial auto insurance quotes San Antonio providers offer requires a methodical approach to data presentation. Carriers don't just look at your industry; they look at how you manage your specific risks. A proactive internal audit of your fleet and driver list is the first step in this process. By identifying and addressing potential red flags before they reach an underwriter, you position your business as a lower risk, which often translates to more favorable pricing.

The power of bundling remains one of the most effective strategies for cost reduction. Combining your commercial auto policy with Business Liability Insurance or a Business Owner's Policy (BOP) often unlocks multi-policy discounts that aren't available for standalone coverage. Additionally, leveraging modern technology like telematics and safety programs provides concrete evidence of your commitment to safety. Carriers appreciate seeing GPS tracking or dash cam data because it suggests a lower frequency of claims, making your business more attractive during the underwriting process.

In the fragmented Texas insurance market, getting multiple quotes is essential. Carrier appetites for specific industries can shift quarterly, meaning the provider that was most competitive last year might not be the best fit today. Comparing several options ensures you aren't overpaying for a risk profile that another carrier might value more highly.

To avoid delays and ensure your commercial auto insurance quotes San Antonio agents provide are accurate from the start, you should prepare a comprehensive data package. Having this information ready prevents the "sticker shock" that occurs when initial estimates are revised after a full background check. Your package should include:

Timing is a critical, yet often overlooked, factor in premium pricing. You should ideally begin the quoting process at least 30 days before your current policy renewal date. Last minute requests can lead to higher premiums because carriers may perceive a lack of planning as a general risk indicator. Consulting with an insurance company near me allows you to tap into local expertise and identify which carriers have the strongest appetite for your specific industry in the current quarter. If you're ready to optimize your coverage and reduce fixed costs, you can request a professional quote analysis today to see how these strategies impact your bottom line.

AMCO.NET LLC has been a cornerstone of the Texas business community since 1987. This long standing history provides a level of stability and expertise that newer, digital only platforms simply can't replicate. When you seek commercial auto insurance quotes San Antonio businesses need for long term security, you aren't just looking for a price; you're looking for a risk management partner. Our role as an independent brokerage allows us to bypass the limitations of captive agencies. Instead of pushing a single product, we access a vast network of highly rated carriers to find the specific policy that aligns with your unique operational requirements.

This independent advantage is crucial in the 2026 market. As we've discussed throughout this guide, rising premiums and shifting regulations like HB 2067 require a flexible, data driven approach. AMCO.NET LLC doesn't rely on impersonal call center interactions. Our clients receive personalized service from specialists who understand the nuances of the Bexar County industrial landscape. Whether you're managing a logistics fleet or a specialized HVAC service, your account is handled by professionals who prioritize technical accuracy and policy continuity over sales volume.

To complement this personal touch, AMCO.NET LLC has integrated advanced technology into our daily workflow. The dedicated mobile application allows business owners to manage their policies, access certificates of insurance, and track claims in real time from any job site. This blend of heritage and modern technology ensures your coverage remains as efficient and agile as the rest of your operations.

The team at AMCO.NET LLC possesses a deep understanding of local regulations and the specific traffic pressures of the I-10 and I-35 corridors. We know that a delay in obtaining a certificate of insurance can stall a project or prevent a vehicle from hitting the road. That's why we've streamlined the process for generating the commercial auto insurance quotes San Antonio professionals require to be both fast and accurate. We don't just provide a number; we provide ongoing support that includes regular policy reviews to ensure you aren't paying for redundant coverage or leaving high value assets exposed to Central Texas weather risks.

Initiating a consultation with an AMCO.NET LLC commercial specialist is a straightforward, professional process. During your initial risk assessment, we'll review your fleet data, driver MVRs, and current policy limits to identify potential areas for optimization and bundling. This data driven approach ensures that the final proposal reflects the true risk profile of your enterprise, allowing for more competitive pricing from our carrier network. You can follow this link to get your commercial auto insurance quote today and begin the process of securing your business's future on Texas roads.

Securing your enterprise for the road ahead requires more than a reactive approach to rising premiums. As we've examined, the intersection of Bexar County traffic patterns, evolving Texas legislation, and precise vehicle classification defines your true risk profile. By moving beyond the minimum state requirements and adopting a data-first strategy, you ensure that your operations remain resilient against the unpredictable variables of the Central Texas market.

AMCO.NET LLC has provided this level of strategic oversight to Texas business owners since 1987. As an independent brokerage, we offer the technical expertise and carrier access necessary to secure the most competitive commercial auto insurance quotes San Antonio professionals can obtain. With our dedicated mobile application and personalized advisory services, your policy management becomes a streamlined component of your business growth rather than an administrative burden.

Request Your Professional San Antonio Commercial Auto Quote from AMCO.NET LLC to begin a comprehensive review of your fleet’s risk management strategy. We're ready to help you navigate the complexities of 2026 and beyond with professional precision.

Yes, Texas law mandates that all vehicles used for business purposes carry minimum liability coverage. For most commercial vehicles, the state requires the 30/60/25 limit, which includes $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. However, federal regulations or specific cargo types, such as hazardous materials, often require significantly higher limits to maintain legal compliance.

The cost of coverage depends on your specific industry risk, vehicle type, and employee driving records. A small business operating a single service van will face different premiums than a logistics company with heavy duty haulers. Factors such as your garaging zip code within Bexar County and your total radius of operation are primary variables that underwriters use to determine your final premium.

Personal auto policies in Texas almost always exclude coverage for business related activities. If you use a personal vehicle for deliveries, transporting clients, or hauling professional equipment, your insurer will likely deny any claims resulting from an accident. Obtaining commercial auto insurance quotes San Antonio providers offer is the only way to ensure your business assets are protected during professional operations.

To ensure technical accuracy, you'll need to provide Vehicle Identification Numbers (VINs) for all units and full license information for every driver. You should also prepare your business's official loss run reports for the past three to five years. Providing your current policy's declarations page is also helpful, as it allows for a precise comparison of existing limits and deductibles against new proposals.

A standard policy typically covers the vehicle itself and liability for accidents, but it doesn't protect the contents. To insure tools, specialized machinery, or cargo while in transit, you'll need an Inland Marine endorsement or a separate cargo policy. This is a critical distinction for contractors and service providers who carry high value equipment between different San Antonio job sites.

Your Motor Vehicle Record (MVR) is one of the most significant factors in determining your premium. Insurers view speeding tickets, at fault accidents, or other violations as indicators of high future risk. When generating commercial auto insurance quotes San Antonio underwriters scrutinize the history of every listed driver, so maintaining a clean fleet record is essential for securing the most competitive rates.

Commercial policies are highly scalable and are available for both single vehicles and large fleets. Whether you're a sole proprietor with one delivery van or a growing enterprise with dozens of units, the underwriting process focuses on your specific business use. The risk assessment remains thorough regardless of the number of vehicles, ensuring that your individual or fleet coverage is tailored to your needs.

You should conduct a professional policy review at least 30 days before your annual renewal. Market conditions in Central Texas fluctuate, and carrier appetites for certain industries can shift. It's also prudent to request new commercial auto insurance quotes San Antonio agents provide whenever you add vehicles, hire new drivers, or change your primary service radius to ensure your coverage remains optimized.