Could maintaining an insurance policy for a vehicle you don't even own be the most strategic financial move you make this year? For many residents in the DFW metroplex, securing non-owner car insurance Dallas is not just a legal formality but a calculated step to protect personal assets and ensure future insurability. You probably recognize the frustration of paying high daily liability rates at rental counters or the anxiety that comes with borrowing a friend's vehicle, especially when Texas laws regarding driver responsibility are so stringent.

This guide provides a professional analysis of how these specialized policies bridge the gap between vehicle ownership and legal road access. We'll demonstrate how a non-owner policy helps you reinstate a Texas driver's license through SR-22 filings and maintains your continuous coverage history to secure lower premiums in the long term. By the end of this article, you'll understand the technical requirements of the 30/60/25 state minimums and how to mitigate the risks associated with the 14% of uninsured drivers currently on our roads.

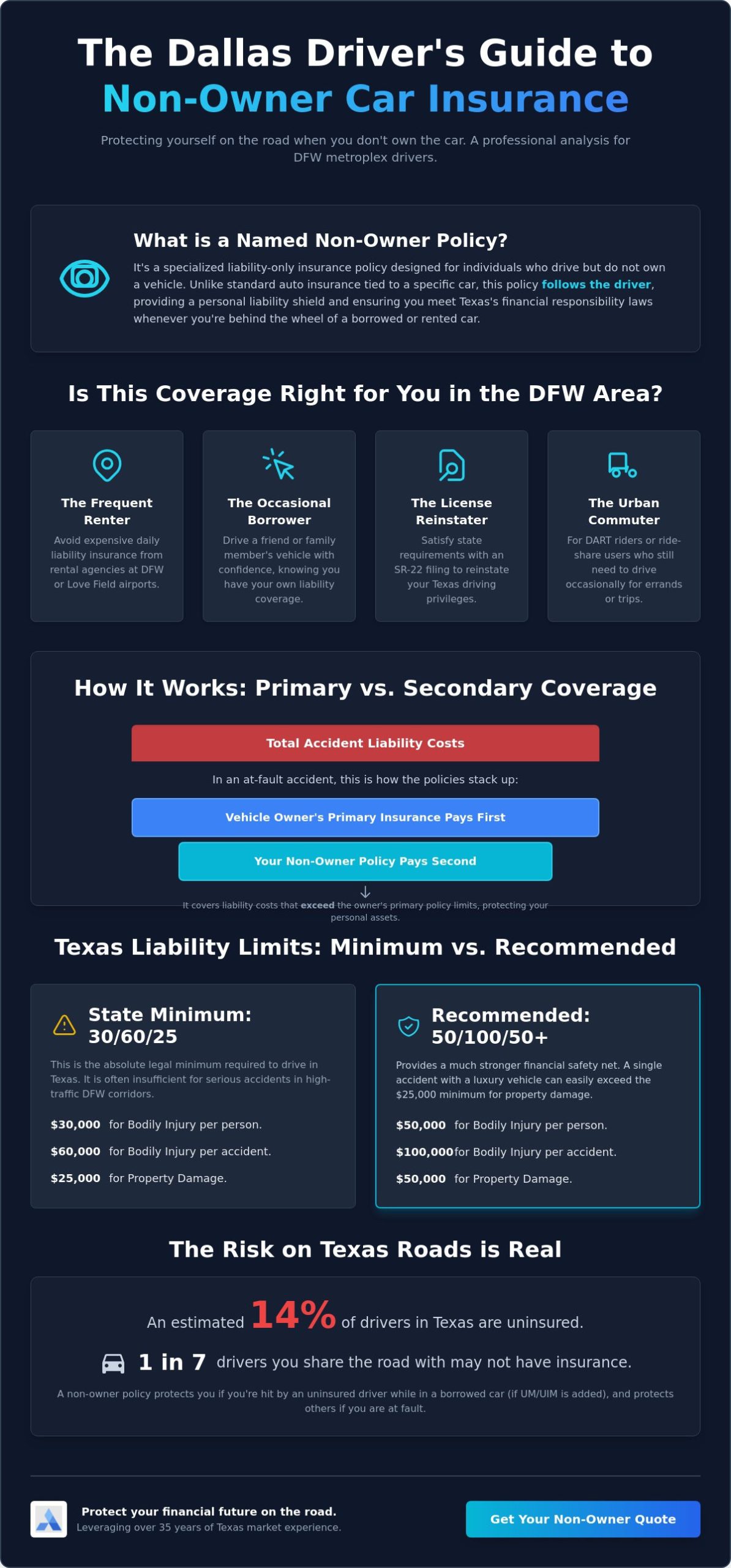

Non-owner car insurance Dallas is a specialized liability-only policy designed for individuals who don't own a vehicle but require legal authorization to drive. Under Texas insurance law, this is technically referred to as a "Named Non-Owner" policy. Unlike standard personal auto coverage that's tied to a specific Vehicle Identification Number, this policy follows the individual driver. This ensures compliance with the Texas Motor Vehicle Safety Responsibility Act, which requires all operators to maintain financial responsibility. To understand the broader context of these protections, it's helpful to first grasp the fundamental principles of What is Car Insurance? and how it allocates risk.

To better understand how this specific policy type integrates into your financial planning, watch this helpful video:

This coverage typically serves as a secondary layer of protection. If you're involved in an accident while driving a borrowed car, the vehicle owner's primary policy pays out first. Your non-owner car insurance Dallas policy then covers any remaining costs that exceed those primary limits. It's a strategic tool for maintaining a continuous insurance history, which is a critical factor for insurers when determining your future premiums. AMCO.NET LLC helps drivers navigate these technical layers to ensure their personal assets remain protected.

A non-owner policy is strictly focused on liability. Bodily Injury coverage manages medical expenses and legal fees for other parties if you're at fault. Property Damage coverage handles the costs for repairs to other vehicles or structures. It's vital to note the specific exclusion; these policies don't cover damage to the vehicle you are currently operating or your own medical injuries. It's a professional shield for your finances, not the physical asset you've borrowed.

Texas law mandates a 30/60/25 minimum, which provides $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. In the high-traffic corridors of North Texas, these minimums are often insufficient. A single collision involving a modern luxury vehicle can easily surpass $25,000 in property damage. We frequently recommend limits of 50/100/50 to provide a more robust safety net. AMCO.NET LLC analyzes your specific risk profile to determine the most cost-effective balance between compliance and comprehensive asset protection.

Dallas drivers often find themselves in situations where they're behind the wheel of a vehicle they don't personally own. Whether you're a DART commuter who occasionally borrows a family member's truck for weekend errands or a business traveler arriving at DFW International, the legal requirement for insurance remains unchanged. For these individuals, non-owner car insurance Dallas provides a portable liability shield. It's a strategic alternative to the high daily rates charged at airport rental kiosks, offering consistent protection that travels with the driver rather than staying with a specific vehicle. This is particularly useful for residents of high-density areas like Uptown or Deep Ellum who rely on ride-sharing but still drive on occasion.

For those navigating the complexities of license reinstatement, this coverage is often a mandatory component of the legal process. The Texas Department of Insurance outlines specific financial responsibility requirements that must be met to clear suspensions. In these cases, the policy acts as the foundation for an SR-22 filing. It proves to the state that you're covered even if you don't have a car registered in your name. Even if you're a dedicated public transit user, you might occasionally borrow a friend's vehicle. Relying solely on the owner's policy is a risk; if an accident occurs and damages exceed their limits, your personal assets could be targeted in a lawsuit. AMCO.NET LLC provides the secondary layer of protection needed to mitigate these unpredictable financial exposures.

License suspensions in Texas often stem from driving without insurance or accumulating multiple traffic violations. To regain your driving privileges, the Texas DPS requires an SR-22 certificate. This isn't a separate type of insurance but a filing attached to your policy. AMCO.NET LLC specializes in these technical requirements, providing same-day electronic filing to the state. This efficiency ensures you can return to the road legally without administrative delays. Maintaining non-owner car insurance Dallas is a strategic choice here because any lapse triggers an immediate notification to the DPS, which can lead to a secondary suspension and further legal complications.

Insurance carriers view drivers with gaps in their history as higher risks. If you sell your car and wait several months to buy another without maintaining a policy, your future premiums will likely increase. By holding a non-owner policy during this transition, you establish a record of continuous coverage. This proactive strategy signals to insurers that you're a responsible driver. Over time, this builds a positive profile that translates into substantial savings on auto insurance when you eventually return to vehicle ownership. AMCO.NET LLC acts as a consultant in this process, ensuring your status remains favorable and you avoid the high-risk labels often applied to those with coverage gaps.

Understanding the technical hierarchy of claims is fundamental to risk management for any driver in North Texas. In the insurance industry, the standard protocol dictates that coverage follows the vehicle, making the car owner’s policy the primary source of protection in the event of an accident. However, relying exclusively on a friend's policy creates a significant financial vulnerability. If you are operating a borrowed vehicle and cause an accident, your non-owner car insurance acts as a secondary shield. It only activates once the primary policy’s limits are fully exhausted. Without this backup, any damages exceeding the owner’s coverage become your personal financial responsibility.

Dallas County courts frequently see litigation involving motor vehicle accidents where damages far exceed state minimums. If a judgment is rendered against you, your personal savings, future wages, and other assets are at risk. A non-owner car insurance Dallas policy provides the necessary legal defense and additional liability limits to prevent such catastrophic outcomes. This is particularly relevant given the "Permissive Use" trap. Some restrictive policies in Texas exclude coverage for anyone not explicitly named on the document, meaning you could be driving completely uninsured without even knowing it. Maintaining your own policy ensures you are protected regardless of the fine print in someone else's contract.

Consider the high-density traffic on I-635, where multi-vehicle collisions are common. If you are found at fault in a chain-reaction accident involving three modern vehicles, a $25,000 property damage limit will likely be consumed by the first bumper and sensor array you impact. Your non-owner policy provides the excess coverage needed to settle these claims professionally. When a standard $30,000 bodily injury limit meets a $100,000 hospital bill for a single injured party, the resulting $70,000 deficit becomes a debt you must personally resolve unless you have secondary coverage in place. This scenario demonstrates why state minimums are often insufficient for the realities of Dallas driving.

For professionals who frequently utilize rental services at DFW or Love Field, these policies offer a clear economic advantage. Daily liability rates at rental counters often range from $15 to $30, whereas an annual non-owner policy provides nationwide protection for a fraction of that cumulative cost. This strategic approach ensures you have consistent liability limits regardless of which rental fleet you are using. For those who frequently travel between major Texas hubs, understanding the broader regional differences is helpful, as detailed in our guide to Car Insurance in Houston, TX: The 2026 Complete Driver’s Guide. This regional perspective helps you build a comprehensive insurance strategy that covers you across the entire state.

Pricing for non-owner car insurance Dallas is determined through a technical assessment of actuarial data specific to the North Texas region. Unlike standard policies that factor in the replacement value of a specific vehicle, these premiums are calculated primarily on the driver's risk profile and the geographic "Dallas Factor." This factor includes the statistical frequency of liability claims and the local litigation environment within specific zip codes. For instance, drivers operating in high-density zones like the Design District or near the North Tollway may encounter different baseline rates than those in lower-traffic suburbs due to the increased probability of a multi-vehicle interaction. AMCO.NET LLC analyzes these regional variables to provide a transparent view of how your location influences your total cost of coverage.

The inherent cost efficiency of these policies stems from the exclusion of physical damage coverage. Because the insurer is not responsible for the comprehensive or collision repair costs of a high-value asset, the administrative baseline for the policy is significantly lower than a traditional auto plan. Drivers can further optimize their expenditures by leveraging professional discounts, such as those for safe driving records or paperless billing. If you currently maintain business liability insurance or other commercial products, our advisors can often identify account-wide efficiencies that reduce the financial burden of maintaining your personal driving privileges.

Your historical performance on Texas roads serves as the primary benchmark for underwriting. While a clean record allows for entry into the most competitive pricing tiers, an SR-22 requirement shifts the driver into a non-standard risk category. This transition involves more than just a one-time filing fee; it reflects a change in how carriers perceive the likelihood of a future liability claim. AMCO.NET LLC acts as an independent consultant in this space, comparing multiple non-standard carriers to ensure that even drivers with challenging histories receive the most equitable rates available in the DFW market. Consistent maintenance of this policy is the most effective method for eventually returning to preferred risk status.

Determining the appropriate coverage level requires a cost-benefit analysis of your personal assets versus the premium increase. While the 30/60/25 state minimum is the most affordable entry point, the price adjustment to move toward "Asset Protection" levels like 100/300/100 is often marginal when compared to the exponential increase in legal security. We also emphasize the importance of Uninsured/Underinsured Motorist (UM/UIM) endorsements. Given the high volume of uninsured operators in the metroplex, this add-on ensures your medical expenses are covered if an uninsured party causes an accident while you are in a borrowed vehicle. For technical details on how these limits satisfy state mandates, refer to our What is SR-22 Insurance in Texas? Houston Driver's Guide.

Selecting the right partner for non-owner car insurance Dallas requires a balance of local market knowledge and technical proficiency. We recognize that insurance isn't merely a monthly expense but a critical component of your personal risk management strategy. For residents across the DFW metroplex, our agency provides the stability of a physical presence combined with the reach of an established industry leader. We focus on delivering precise solutions that align with the specific liability needs of North Texas drivers, ensuring you never pay for coverage you don't actually need.

Operational efficiency defines our approach to the independent agency model. Unlike "captive" agents who are restricted to a single carrier's products, we maintain relationships with a diverse network of insurance providers. This allows us to shop the market on your behalf, comparing different underwriting criteria to find the most competitive rates for your unique profile. Whether you're a frequent traveler at DFW International or a local professional maintaining continuous coverage history, we provide the choice and transparency that big-box insurers often lack.

Our status as a local expert means we have a deep understanding of Dallas County requirements and the Texas DPS administrative processes. We specialize in the complexities of SR-22 filings, providing the technical support necessary to help you reinstate your driver's license without unnecessary friction. We handle the paperwork and electronic submissions, allowing you to focus on your professional and personal commitments while we manage your legal compliance.

Long-term stability is a hallmark of our service, with over 35 years of experience serving the Texas market. Since 1987, we've helped thousands of drivers manage shifting state regulations and evolving insurance landscapes. This historical perspective allows us to provide advisory services that go beyond simple price quotes. We understand how to navigate the nuances of Texas insurance law to find affordable solutions even for high-risk drivers who have been turned away by other agencies. Our commitment to professional integrity ensures that every policyholder receives personalized attention and a strategy tailored to their specific financial goals.

Modern drivers require flexibility and speed. Our quote process is designed for efficiency, allowing you to secure a non-owner car insurance Dallas policy through our online platform or mobile app in minutes. If your situation requires immediate road access, we offer same-day coverage options and instant filing capabilities to satisfy legal mandates. For those who prefer a face-to-face consultation, our local offices provide the expert guidance you need to make an informed decision. You can learn more about the value of local partnerships in our guide on Insurance Company Near Me: Finding the Best Local Expertise in Texas for 2026. Contact us today to secure your financial future and maintain your legal right to drive.

Securing a non-owner policy is a proactive measure that protects your personal assets while ensuring you remain compliant with Texas law. We have analyzed how these policies function as a secondary shield during major accidents and why they are essential for maintaining a continuous insurance history. By addressing the specific requirements of Dallas County, you can avoid the high costs of rental counter insurance and the legal risks of driving without a verified liability profile. Choosing non-owner car insurance Dallas provides the flexibility you need without the overhead of vehicle ownership.

AMCO has been serving Texas drivers since 1987, offering A+ rated customer service and the local expertise required to navigate complex regulations. Whether you need same-day SR-22 filing or immediate coverage binding, our team is ready to provide the professional support your situation demands. Get your fast and affordable Dallas non-owner insurance quote from AMCO today! Maintaining your legal right to drive is a vital component of your professional mobility, and we are here to ensure that your coverage remains seamless and secure.

No, this coverage isn't legally mandatory for every resident who doesn't own a vehicle. However, it becomes a requirement if the Texas Department of Public Safety mandates an SR-22 filing following a license suspension or specific traffic convictions. Even without a mandate, many drivers maintain a policy to prevent a lapse in coverage, which helps secure lower premiums when they eventually purchase a vehicle.

Generally, no. Most non-owner car insurance Dallas policies specifically exclude vehicles owned by household members or cars that are available for your regular use. These policies are designed for occasional use of vehicles owned by individuals outside your immediate residence. If you regularly drive a roommate's or relative's car, you should be added as a named driver on their primary auto policy instead.

Yes, CDL holders can obtain a personal non-owner policy to protect their personal driving record or satisfy state-mandated filing requirements. It's important to understand that this policy only applies to the operation of personal vehicles and doesn't extend to commercial activities or the operation of heavy equipment. It serves as a personal liability shield while you're off the clock and driving a borrowed passenger vehicle.

No, non-owner insurance is strictly a liability-only product. It covers bodily injury and property damage you cause to others, but it doesn't provide collision or comprehensive protection for the vehicle you're driving. When renting a car at DFW, you'll still need to rely on the rental company's Loss Damage Waiver (LDW) or your credit card's secondary rental coverage to protect the vehicle's physical body.

AMCO provides same-day electronic filing to the Texas Department of Public Safety. Once your policy is bound and the premium is processed, our systems transmit the certificate of financial responsibility immediately. This digital integration minimizes administrative delays, allowing you to proceed with the license reinstatement process as quickly as the state's processing times allow.

You'll need to contact your agent to convert your coverage into a standard owner's policy. A non-owner car insurance Dallas policy is invalid for any vehicle registered in your name or owned by you. Converting the policy ensures your new asset is protected with the necessary comprehensive and collision coverage while maintaining the continuous insurance history you've built.

No, personal non-owner policies explicitly exclude any commercial use, including ride-sharing or delivery services. Operating as a TNC driver requires specialized commercial endorsements or a dedicated business policy. Relying on a non-owner policy for professional driving will lead to denied claims and potential policy cancellation due to the high-risk nature of commercial transit.

No, you cannot use a non-owner policy for vehicle registration. The Texas Department of Motor Vehicles requires proof of insurance that specifically lists the Vehicle Identification Number (VIN) of the car being registered. Since non-owner policies don't attach to a specific vehicle, they don't meet the state's technical requirements for title or registration purposes.