Did you know that Texas non-subscribers lose nearly all legal defenses in a workplace injury lawsuit, including the ability to argue an employee’s own negligence? In Austin’s 2026 economic environment, many business owners view coverage as an optional expense, yet a single claim can result in uncapped liability. Securing robust workers compensation insurance Austin is no longer just a regulatory consideration; it’s a critical component of risk management and long-term financial stability for your organization.

You likely recognize that managing rising medical costs, which saw a 2.7% increase in conversion factors this year, requires a more sophisticated approach than simply paying premiums. This article provides a comprehensive framework to help you manage local risks, navigate the 2026 State Average Weekly Wage updates, and implement strategies to lower your experience modifier score. We'll examine the technical details of the DWC claims process and identify how to achieve full legal protection while maintaining operational efficiency. By the end of this guide, you’ll have a clear roadmap for finding cost-effective coverage that aligns with the specific safety requirements of the Central Texas market.

What if opting out of workers' comp actually costs your business more than the premiums ever would? Many Austin employers believe that non-subscription offers a simple way to reduce overhead, but this choice often leads to uncapped legal liability in personal injury lawsuits. This guide provides the technical clarity you need to find the most cost-effective workers compensation insurance Austin while ensuring your business remains protected against unpredictable litigation. We'll examine the NCCI premium formula, the legal nuances of the Texas "Grand Bargain," and the specific safety requirements for the local tech and construction industries.

You'll learn about the financial mechanics of premiums, including how your industry’s class code and experience modifier impact your bottom line. We analyze the critical differences between subscription and non-subscription, focusing on the loss of legal defenses for those who opt out. The guide also details industry-specific risk management for Austin’s diverse economy, from remote work ergonomics in tech to high-hazard construction protocols. Finally, we explain the advantage of partnering with AMCO.NET as an independent agency, leveraging over 35 years of expertise to shop multiple carriers and navigate the complex 2026 Texas insurance landscape.

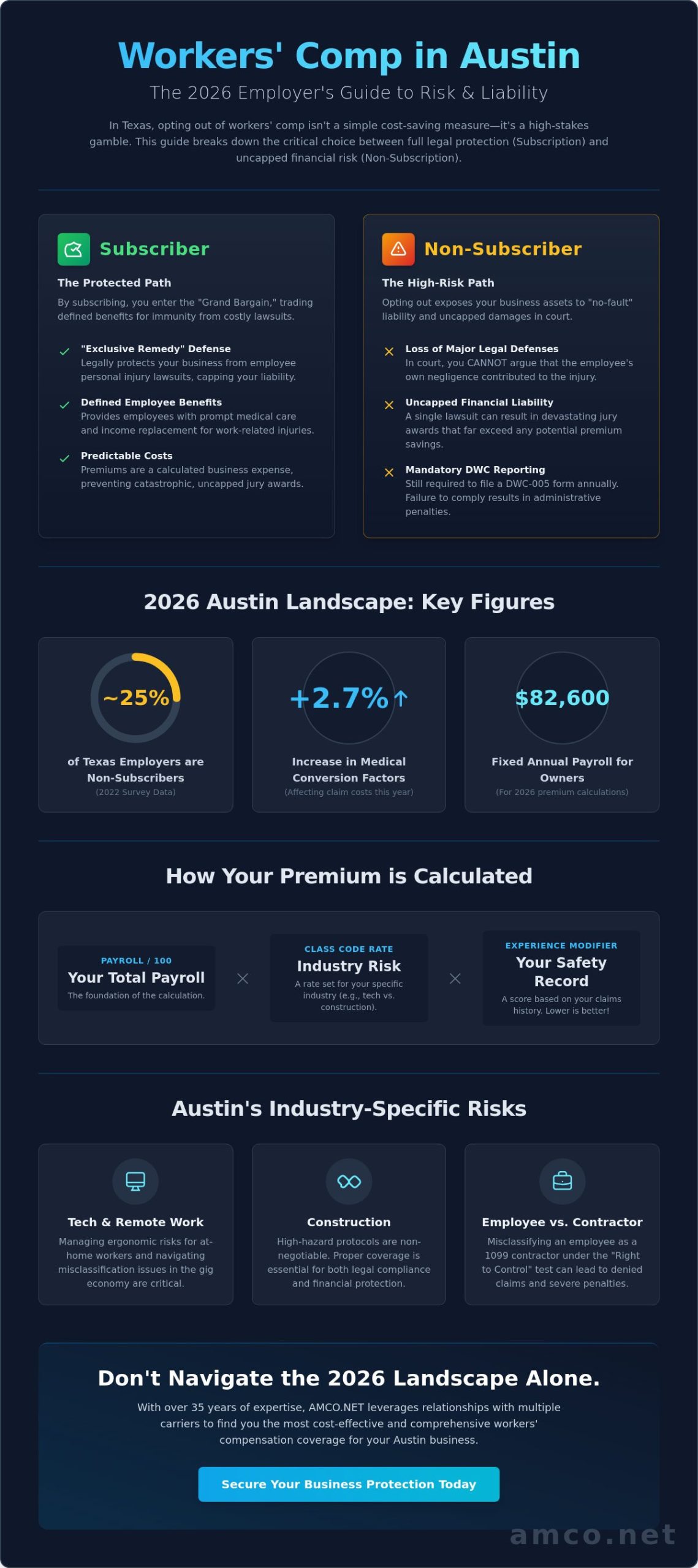

In the Texas Department of Insurance (TDI) framework, workers’ compensation serves as a specialized insurance system providing medical benefits and income replacement to employees injured on the job. Unlike every other state, Texas allows private employers to opt out of this system, a status known as "non-subscription." While this flexibility exists, choosing to secure workers compensation insurance Austin remains a foundational decision for most established firms because it establishes the "exclusive remedy" defense. This legal protection prevents employees from suing their employer for personal injury damages, effectively trading defined benefits for immunity from unpredictable litigation.

To understand how these state-level regulations fit into the broader national context, it’s helpful to view the U.S. workers' compensation system as a "grand bargain" between labor and management. In Austin’s competitive labor market, this bargain ensures that workers receive prompt medical care while business owners avoid the threat of uncapped jury awards. For those who choose to be non-subscribers, the risks are stark. Approximately 25% of Texas employers were non-subscribers as of a 2022 survey, and these entities face "no-fault" liability. In a lawsuit, a non-subscriber cannot argue that the employee was negligent or that a coworker caused the accident, leaving the business's assets exposed.

To better understand this concept, watch this helpful video:

The DWC monitors the system to ensure claims are handled fairly and medical networks operate efficiently. As of January 1, 2026, the state replaced the old maintenance tax with a more flexible surcharge system to fund these operations. The assessment rate can now reach up to 2.7% of gross premiums. Every Austin business owner must stay compliant with reporting, specifically the DWC-005 form. This document must be filed annually by non-subscribers to notify the state of their lack of coverage. Failure to file or properly notify employees can result in administrative penalties that erode the perceived savings of opting out.

Determining who requires coverage is a technical process governed by the "Right to Control" test. Texas courts look at whether the employer directs the details of the work, rather than just the end result. In the Austin tech and gig economy, misclassifying a worker as a 1099 contractor when they function as an employee creates significant liability. For 2026, the fixed annual payroll for sole proprietors and partners is set at $82,600 for premium calculation purposes. Managing these classifications accurately is essential to maintaining your workers compensation insurance Austin policy and avoiding costly audit adjustments or denied claims.

Calculating the financial commitment for workers compensation insurance Austin requires understanding a specific mathematical framework. Carriers don't simply assign a flat fee. Instead, they apply a precise formula: (Payroll / 100) x Class Code Rate x Experience Modifier. This structure ensures that your premiums reflect the actual risk and scale of your operations. For 2026, business owners must account for the fixed annual payroll for sole proprietors and partners, which the state has set at $82,600 for premium calculation purposes.

The base of this calculation is the NCCI class code. These codes categorize job duties by their inherent danger. A software developer in a North Austin tech hub will have a significantly lower base rate than a framing contractor. The Texas Department of Insurance, Division of Workers’ Compensation provides the regulatory oversight for these classifications, ensuring that the 11.5% average rate reduction approved for 2025 is applied fairly across the market. However, local market pressures can still influence the final figure you see on a quote.

Austin’s medical market is currently experiencing significant pressure. The 2.7% increase in the Medical Fee Guideline conversion factors, effective January 1, 2026, directly impacts claim severity. Higher hospital and specialist costs in Central Texas mean that even a minor injury can become a substantial financial liability. Accuracy during your annual insurance audit is also vital. Misreporting payroll or failing to update employee classifications can lead to unexpected back-payments that disrupt your cash flow. Your safety record remains the most influential factor, as it determines your experience modifier (e-mod) score.

Implementing a formal "Return-to-Work" program is one of the most effective ways to control long-term costs. By bringing injured employees back in a modified capacity, you reduce the indemnity payments that drive up your e-mod score. Many Texas carriers also offer safety grants and specialized training that can help you mitigate risks before they turn into claims. Leveraging the expertise of an independent agency allows you to perform a multi-carrier search to find the most competitive workers compensation insurance Austin rates. This approach ensures you aren't tied to a single carrier’s appetite for risk, allowing for a more optimized and cost-effective policy structure.

The "Grand Bargain" of workers’ compensation represents a technical trade-off that defines the Texas insurance market. By securing workers compensation insurance Austin, a business owner provides guaranteed medical and income benefits to injured workers. In exchange, the employer receives statutory immunity from personal injury lawsuits. This "exclusive remedy" provision acts as a financial firewall. Without it, your business is vulnerable to the full spectrum of civil litigation, where damages for pain, suffering, and punitive measures are often decided by a jury rather than a structured benefit schedule.

Choosing the Texas non-subscription option might seem like a cost-saving measure on the surface. However, the hidden costs of legal defense for even a single workplace injury can quickly exceed years of premium payments. In 2026, litigation remains a top concern for nearly 60% of industry professionals. For an Austin business, the choice to opt out means losing the ability to settle claims through the DWC’s administrative process, shifting the battleground to the courtroom where legal fees accumulate regardless of the case outcome.

Employee retention also hinges on this decision. Austin's workforce is highly mobile and increasingly risk-aware. Professionals in the tech and hospitality sectors often view formal coverage as a standard benefit. A company that doesn't provide these protections may struggle to attract top-tier talent who prioritize personal financial security.

Non-subscribers lose critical legal protections known as common law defenses. You can't argue that the employee’s own negligence or the negligence of a coworker contributed to the accident. This "all-or-nothing" legal environment means that if you're found even 1% at fault, you may be liable for 100% of the damages. This exposure has the potential to bankrupt a small Austin business following a single catastrophic incident.

Some firms consider Occupational Accident (Occ Acc) plans as a middle ground. These policies cover medical expenses and lost wages but don't provide the legal immunity found in statutory workers’ comp. They often fall short of the comprehensive standards set by the Texas Workers’ Comp Act. Most government entities and primary contractors in Austin require subcontractors to carry full workers compensation insurance Austin to avoid the "no-fault" liability traps associated with private accident plans.

Austin’s economic landscape is diverse, and a one-size-fits-all approach to workers compensation insurance Austin often leaves businesses with significant coverage gaps. While the average premium for a Texas tech company is approximately $34 per month as of April 2026, a framing contractor or a high-volume restaurant faces a completely different risk profile and pricing structure. Aligning your policy with the specific operational hazards of your industry is the only way to ensure the "Grand Bargain" of immunity remains intact during a claim.

For the hospitality and retail sectors, the data shows a pressing need for better risk management. This industry saw a 41% increase in serious reported claims in 2024. Slips and falls remain the primary drivers of these statistics, but modern policies in 2026 are also incorporating coverage for workplace violence and mental health support following traumatic incidents. Similarly, businesses in the logistics sector must carefully coordinate their benefits with commercial trucking insurance to ensure drivers are protected whether they are behind the wheel or on a loading dock.

The rise of distributed teams means your 2026 policy must account for remote employees working from Round Rock, West Lake, or even out of state. Repetitive stress injuries (RSIs) and ergonomic claims are the most common issues in the Silicon Hills startup environment. Insurance carriers are now using AI and predictive analytics to identify early signs of burnout or stress-related claims, which are becoming more prevalent in high-growth environments. Ensuring your policy definition of "workplace" includes home offices is a technical necessity for modern compliance.

In the construction industry, a Certificate of Insurance (COI) is your ticket to the job site. While private employers in Texas can technically opt out of coverage, any company contracting with a government entity in Austin is legally required to carry workers’ comp. This is particularly critical given that framing contractors experienced a 200% increase in serious injury claims recently, with over 55% of those being falls from heights. Managing your Experience Modifier score after such an event requires a proactive safety program and the correct integration of general liability insurance to provide a complete shield against third-party claims.

If you need to verify that your current policy limits meet the specific requirements of an Austin municipal contract, you can request an industry-specific coverage review to identify potential vulnerabilities in your risk management strategy.

Selecting the right workers compensation insurance Austin involves more than just comparing premium numbers. Many carriers have a narrow appetite for risk, which can lead to inflated rates if your industry doesn't fit their standard profile. As an independent agency, AMCO.NET functions as a strategic partner rather than a single-source vendor. We leverage our relationships with a broad network of carriers to find the policy that aligns with your specific operational needs. This broker advantage ensures you aren't limited to the pricing or underwriting restrictions of a single company.

Since 1987, our team has navigated the evolving regulatory environment of the Texas insurance market. This deep-rooted experience allows us to provide insights that extend beyond Austin, covering major economic centers including Houston. In 2026, business owners require modern tools to manage their risk effectively. Our mobile app provides seamless digital management, allowing you to handle payments and generate certificates of insurance (COIs) instantly from any job site. This technological continuity provides the predictability you need to focus on growth.

The annual insurance audit is often a source of stress and unexpected costs for many organizations. We act as a professional liaison between your business and the carrier to ensure your payroll data is classified correctly. Our consultative approach focuses on long-term stability rather than short-term fixes. By helping you implement the safety protocols and return-to-work programs mentioned earlier, we target a lower experience modifier score. This methodical reduction in your risk profile leads to more sustainable premium structures over time, protecting your bottom line from the rising medical costs in Central Texas.

Our 2026-optimized quoting process is designed for technical precision and speed. We understand that workers compensation insurance Austin is often just one piece of a larger risk management puzzle. You can streamline your overhead by exploring bundling options, such as combining your commercial coverage with car insurance or property protection. Contact our local experts today for a comprehensive risk assessment. We'll help you secure a policy that provides full legal protection while maintaining the financial efficiency your business requires to remain competitive.

Managing a business in Austin’s dynamic economy requires a proactive stance on risk. You've seen how the "Grand Bargain" of workers’ compensation provides a critical shield against unpredictable litigation, especially as medical costs and legal complexities continue to rise. Whether you're navigating the high-hazard requirements of a construction site or the ergonomic challenges of a tech startup, the right workers compensation insurance Austin policy is a strategic asset that protects both your employees and your balance sheet. Relying on the Texas non-subscription option leaves your assets exposed to uncapped liability; a risk that professional coverage systematically eliminates.

Since 1987, AMCO.NET has served Texas business owners by providing access to top-rated national and regional carriers. Our specialized experts understand the technical nuances of the trucking and construction industries, ensuring your policy meets every regulatory and contractual demand. You can Get a Workers’ Comp Quote for Your Austin Business today and leverage our independent agency advantage to find the most cost-effective solution. Taking this step ensures your organization remains resilient, compliant, and ready for future growth.

Private employers in Texas aren't legally required to carry this coverage, making it the only state with a truly optional system. However, any business that contracts with a government entity in Austin must maintain a valid policy to comply with state law. While the choice is yours, opting out requires you to file DWC Form-005 annually and notify every employee of your lack of coverage.

Businesses that opt out are classified as non-subscribers and lose their critical common law defenses in court. If an injured worker sues, you can't argue that the employee’s own negligence or a coworker’s actions caused the accident. This exposure often leads to unlimited liability and high legal defense costs that can threaten the financial stability of a small or medium-sized enterprise.

Premiums are calculated using a technical formula that considers your total payroll, industry class codes, and your specific claims history. High-hazard industries like construction naturally face higher base rates than tech-focused firms. To find the most accurate rate for workers compensation insurance Austin, a professional audit of your job classifications and safety protocols is necessary to ensure you aren't overpaying due to misclassification.

Yes, injuries sustained by remote employees are generally covered if they occur within the course and scope of their employment. As Austin’s tech sector continues to embrace distributed work, carriers are increasingly scrutinizing ergonomic and repetitive stress claims from home offices. It's essential to define the workplace clearly in your safety manuals to ensure these claims are managed effectively within your policy framework.

The Experience Modifier, or e-mod, is a numerical multiplier that adjusts your premium based on your company's actual loss history compared to the industry average. A score of 1.0 is the baseline; a lower score results in a premium discount, while a higher score indicates a higher risk profile and increases your costs. Maintaining a rigorous safety culture is the most effective way to lower this score over time.

Generally, no. Workers’ compensation acts as the exclusive remedy for workplace injuries, providing you with statutory immunity from personal injury lawsuits. This legal shield is the primary reason most Austin business owners maintain coverage. The only rare exception involves cases of gross negligence or intentional acts that lead to a fatality, where certain legal protections may be challenged in court.

Employers must report any injury that results in more than one day of lost work to their insurance carrier using DWC Form-001. This report must be filed within eight days of the accident or the date the employer was notified. Your insurance carrier then handles the technical filing with the Division of Workers’ Compensation, ensuring the claim moves through the regulated medical and benefit system.

Sole proprietors, partners, and LLC members aren't automatically covered under Texas law, but they can choose to include themselves in a workers compensation insurance Austin policy. For 2026, the state has set a fixed annual payroll of $82,600 for premium calculation purposes for these individuals. Including yourself in the coverage ensures access to medical benefits and income replacement if a workplace injury prevents you from managing your operations.