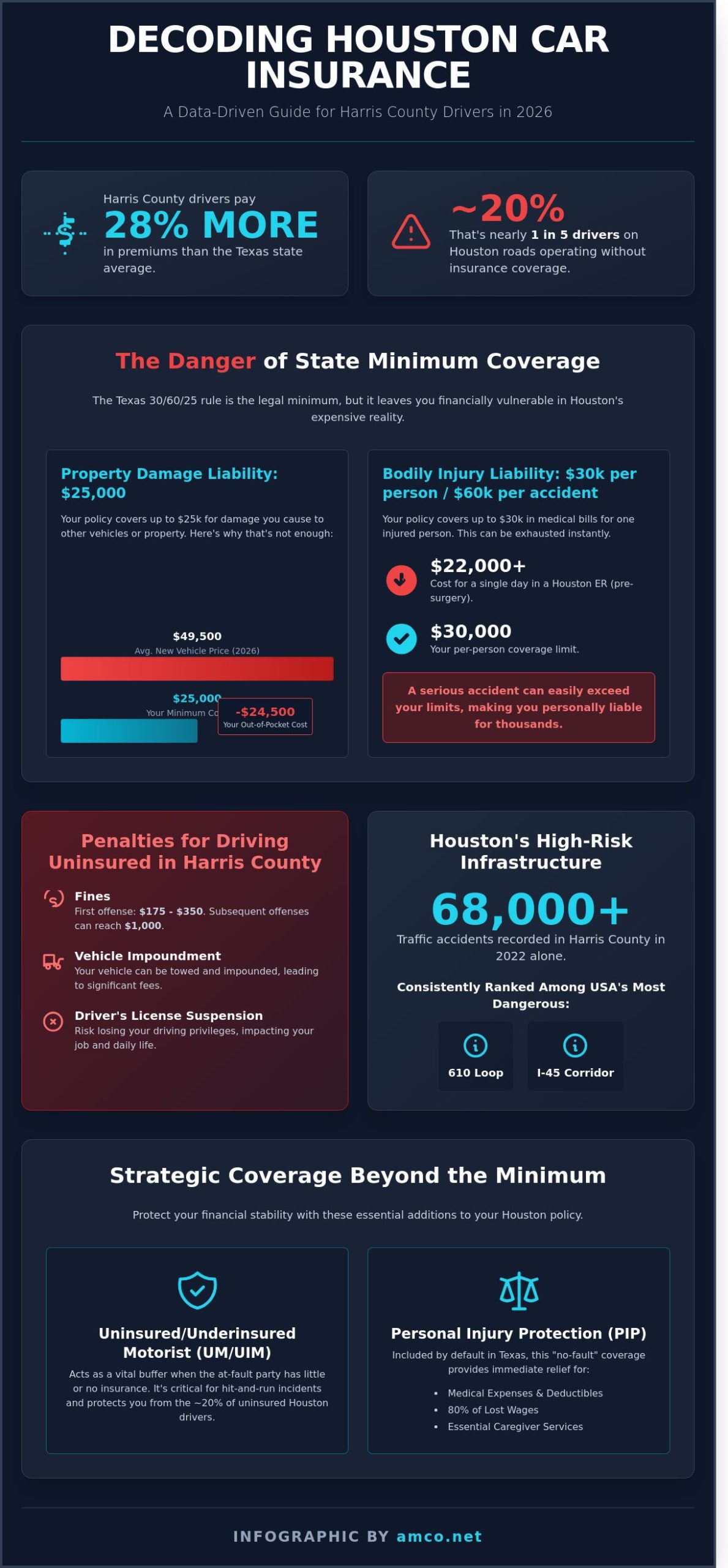

Did you know that drivers in Harris County currently pay premiums that are 28% higher than the Texas state average? Securing affordable car insurance houston has become a complex technical challenge rather than a simple administrative task. You likely feel the pressure of these rising costs, especially when data shows nearly 20% of motorists on local roads operate without any coverage. It's a logical concern for any driver who prioritizes financial stability and road safety in an increasingly volatile market.

You deserve a policy that balances cost-efficiency with uncompromising protection. This 2026 guide delivers a data-driven framework to help you secure competitive rates while ensuring your vehicle is shielded from specific local risks like the flash flooding seen in recent seasons. We'll clarify the technical distinctions between Personal Injury Protection and Medical Payments, identify the most efficient providers in the 713 and 832 area codes, and outline a robust claims strategy that guarantees long-term continuity for your daily commute.

Texas law requires every driver to maintain a minimum level of financial responsibility to operate a motor vehicle on public roadways. For professionals and residents seeking car insurance houston, the baseline is the 30/60/25 liability rule. This formula represents the absolute floor for Texas legal compliance. While these figures satisfy the statutory requirements, they often prove insufficient for the high-density traffic environments found on the Katy Freeway or the 610 Loop. The Texas Department of Insurance oversees the industry by monitoring rate filings and ensuring companies maintain enough capital to pay out claims, but they don't set the specific rates for individual drivers.

Operating a vehicle without valid coverage in Harris County leads to immediate and documented legal repercussions. First-time offenders typically face fines between $175 and $350. Subsequent violations can result in fines reaching $1,000, vehicle impoundment, and the suspension of your driver's license. Houston law enforcement utilizes real-time database access to verify insurance status during routine stops, making the risk of driving uninsured a significant threat to your professional mobility and financial stability. These same requirements apply to all motor vehicles, including those who need motorcycle insurance in Houston and Texas, where riders face even greater exposure to uninsured motorists on busy highways.

The 30/60/25 rule breaks down into three specific categories of coverage. Bodily injury liability is currently set at $30,000 per person and $60,000 per accident. In the 2026 medical climate, where a single day in a Houston emergency room can cost upwards of $22,000 before surgery or specialized imaging, these limits are dangerously low. If you're at fault in a multi-vehicle collision, a $60,000 total cap leaves you personally liable for any medical costs that exceed that amount.

Property damage coverage is capped at $25,000 under the state minimum. This figure is particularly risky given that the average price of a new vehicle in 2026 is approximately $49,500. If you collide with a late-model truck or an electric vehicle, a $25,000 policy will not cover the full replacement or repair cost. The gap between your coverage and the actual damage becomes your personal debt, which can lead to the seizure of non-exempt assets or long-term wage garnishment. For a broader understanding of how these statewide rules affect drivers beyond Harris County, our Texas auto insurance guide for 2026 provides a detailed analysis of requirements, costs, and localized risk factors across the state.

Texas insurance contracts include Personal Injury Protection (PIP) by default. It's an "opt-out" coverage, which means you must reject it in writing if you choose not to carry it. PIP differs from standard health insurance because it provides immediate "no-fault" relief. It covers medical expenses, 80% of lost wages, and essential caregiver services without requiring a determination of who caused the accident. For those navigating car insurance houston options, we recommend retaining PIP coverage. It serves as a critical bridge for immediate liquidity, ensuring you can cover deductibles and lost income while the broader liability claims are processed through the legal system.

Houston's infrastructure presents unique operational challenges for every driver. The 610 Loop and the I-45 corridor consistently rank among the most dangerous stretches of highway in the United States. In 2022, the Texas Department of Transportation recorded over 68,000 traffic accidents in Harris County alone. While meeting Texas minimum insurance requirements is a legal necessity for registration, it rarely provides sufficient protection against the complexities of a car insurance houston policy. Relying on basic liability leaves significant gaps in your financial security, especially when considering the high density of heavy commercial traffic and unpredictable weather patterns. The presence of numerous commercial trucking operations on major corridors like I-10 requires specialized risk assessment, which is why many fleet operators rely on commercial trucking insurance Houston providers to manage their complex liability exposures.

Data from the Insurance Research Council indicates that approximately 14% of Texas drivers operated vehicles without insurance in 2019. In a metropolitan area as vast as Houston, this translates to a high probability of encountering an uninsured driver during your daily commute. UM/UIM coverage acts as a vital buffer when the at-fault party lacks the resources to cover your damages. This is particularly critical for hit-and-run incidents on busy freeways where identifying the other driver is often impossible. Choosing this supplement prevents you from paying thousands of dollars out of pocket for medical bills or vehicle repairs that weren't your fault.

Distinguishing between Collision and Comprehensive coverage is vital for risk management in the Gulf Coast region. While Collision covers impact-related damage, Comprehensive addresses environmental and non-collision risks. In neighborhoods like Meyerland or Kingwood, flash flooding remains a persistent threat; during Hurricane Harvey in 2017, an estimated 500,000 vehicles were damaged by rising water. Comprehensive is the only coverage for non-accident vehicle loss. Without this specific protection, a sudden storm or a high-water event could result in a total financial loss of your automotive assets. Understanding how these components work together is essential, which is why reviewing a detailed breakdown of full coverage car insurance in Texas can help you structure a policy that truly protects against Houston's unique risks.

Supplementing your policy with either Medical Payments (MedPay) or Personal Injury Protection (PIP) adds another layer of security. PIP is generally the preferred choice for Houston professionals because it covers 80% of lost wages and essential services in addition to medical expenses. MedPay is more limited, focusing strictly on medical bills regardless of fault. Analyzing these options with a expert consultant allows you to build a policy that ensures both physical and financial continuity after an incident. Balancing these technical details is the only way to achieve true long-term stability on Houston's roads.

Securing competitive car insurance houston rates requires a systematic analysis of technical variables rather than a cursory search for the lowest sticker price. In 2026, insurance carriers utilize complex algorithms where your zip code, credit score, and driving history act as the primary metrics for risk assessment. Data from the first quarter of 2025 shows that drivers with a credit score above 740 typically see a 15% reduction in premiums compared to those in the "fair" range. Precision in your application is vital; even minor discrepancies in reported annual mileage can lead to premium adjustments during the underwriting process.

The "Broker Advantage" represents a strategic necessity for Houston residents. Relying on a single carrier's quote limits your market visibility and ignores the volatility of regional pricing. An independent broker can access proprietary rating systems from 15 or more carriers simultaneously. This often identifies cost-saving opportunities that direct-to-consumer platforms miss. When evaluating car insurance quotes houston drivers can rely on, working with a local expert who understands Harris County's specific risk data gives you a measurable advantage over using national comparison tools alone. If your driving history includes major infractions, you might be required to file for SR-22 insurance in Texas, which necessitates a specialized comparison of high-risk providers to maintain legal compliance.

Commute length also dictates your risk profile. Houston drivers averaging 30 miles daily on I-10 face higher exposure to accidents than those with a 5-mile commute. Reducing your annual mileage below the 10,000-mile threshold can trigger a low-mileage discount of approximately 12% with most major Texas underwriters.

Premiums fluctuate significantly between neighborhoods based on localized risk data. Living in 77002 (Downtown) often results in higher base rates due to traffic density and a 20% higher rate of property-related claims compared to suburban areas. In contrast, 77015 (North Shore) might see different Comprehensive premium adjustments based on local theft statistics. To mitigate these costs, focus on secure, off-street parking. Installing a GPS-based recovery system can reduce the Comprehensive portion of your bill by 5% to 8%.

Consolidating your insurance portfolio provides a reliable path to cost optimization. Bundling car insurance houston with homeowners insurance in Texas often yields a 15% discount across all policies. Telematics programs, which track braking and acceleration through mobile apps, offer potential savings of 10% to 30%. While some drivers express privacy concerns, the financial return is measurable for those with consistent, predictable driving habits. Houston-based professionals and alumni from institutions like the University of Houston or Rice University often qualify for exclusive group rates through specific regional underwriters. For a broader perspective on how rising premiums are affecting all policy types across the region, the comprehensive guide to insurance in Houston for 2026 provides valuable industry insights on cost optimization strategies for both personal and commercial coverage.

Drivers in Harris County may encounter legal requirements that complicate their search for affordable coverage. The most common hurdle is the SR-22 certificate. An SR-22 is a financial responsibility form filed by an insurance provider with the Texas Department of Public Safety (DPS). It serves as official verification that a driver maintains the state-mandated 30/60/25 liability limits. It is vital to understand that an SR-22 is a filing, not a type of insurance policy.

The Texas DPS typically mandates this filing for specific high-risk scenarios. These include a DWI conviction under Texas Penal Code Chapter 49, driving with an invalid license, or a second conviction for failing to maintain valid car insurance houston within a two-year period. According to Texas law, most drivers must maintain this financial responsibility filing for two continuous years from the date of their conviction. If the policy lapses for even one day during this timeframe, the insurer is legally required to notify the state, which results in an immediate driver's license suspension.

Reinstating a suspended license involves a multi-step administrative process. Drivers must first pay a $100 reinstatement fee to the DPS and obtain the SR-22 certificate from an authorized carrier. While the actual cost of adding the filing to a policy is low, ranging from $15 to $25, the impact on the premium is significant. High-risk drivers often see their annual rates increase by 35% to 50% because the filing signals a higher statistical likelihood of future claims. Professional agencies help manage this transition by identifying carriers that offer the lowest surcharges for these specific filings. For comprehensive guidance on navigating these complex requirements, our detailed SR-22 insurance Texas guide provides step-by-step instructions for Houston and regional drivers.

When a driving record includes multiple at-fault accidents or serious moving violations, "preferred" insurance companies may deny coverage altogether. This necessitates a move to the non-standard insurance market. These carriers specialize in high-risk placement, offering a path for drivers to remain legal while they rehabilitate their records. Independent agencies are better equipped for this task than "captive" agents because they can compare quotes across dozens of non-standard providers simultaneously. Over a period of 36 to 60 months of clean driving, most individuals can successfully migrate back to standard or preferred tiers, significantly reducing their long-term costs.

Selecting a partner for car insurance houston requires looking beyond the lowest premium. It involves finding an agency that understands the 29.4-minute average commute time in the metro area and the specific risks of the 610 Loop. Local agents recognize that driving patterns in neighborhoods like Montrose differ significantly from those in the Energy Corridor. This regional knowledge ensures your coverage limits actually reflect the risks you face daily on Texas highways.

Understanding the difference between captive agents and independent brokers is essential for cost optimization. Captive agents are employees of a single insurance company and can only offer that company's specific products. Independent brokers access a broad network of multiple carriers. This independence allows them to compare rates and find the most efficient policy for your budget. When searching for an insurance company near me with specialized Texas expertise, AMCO.NET LLC has maintained this independent approach since 1987, providing a stable, expert presence in the Houston community for 37 years.

Digital tools provide efficiency, but they often lack the depth of a face-to-face consultation. When you call a 1-800 number, you're usually speaking to a rotating staff of representatives who don't know your history. A local agent provides claims advocacy, acting as a professional intermediary between you and the insurance carrier during a settlement. This technical support is vital for ensuring you receive a fair payout. For daily management, the AMCO.NET LLC mobile app offers digital ID cards and policy access, combining modern convenience with traditional expert oversight.

Securing a quote is a methodical process that requires specific data to ensure accuracy. You'll need to provide the 17-digit Vehicle Identification Number (VIN) for all cars, the driver's license numbers for every person in your household, and your current policy's declarations page. Having these documents ready allows for a precise comparison of coverage levels and deductibles.

Transitioning to a more reliable provider doesn't have to be complex. You can get a fast and affordable Houston car insurance quote from AMCO.NET LLC through our online portal or by visiting one of our local offices. Our team focuses on long term stability and professional service, ensuring your assets remain protected on every Texas road. Whether you prefer managing your car insurance houston through a mobile app or a physical office, we provide the technical expertise necessary to safeguard your vehicle.

Navigating the complex landscape of 2026 Texas driving regulations requires a strategic approach to risk management. You've seen how standard liability limits often fall short on high-traffic corridors like I-610 or the Sam Houston Tollway. Securing reliable car insurance houston means balancing cost-efficiency with the technical necessity of comprehensive coverage. Whether you're managing an SR-22 filing or optimizing a standard family policy, the goal remains long-term financial continuity and legal compliance. Professional guidance helps you avoid the pitfalls of under-insurance while maintaining a budget that works for your household.

AMCO has served the local community as a trusted partner since 1987. As an A+ rated independent agency, we prioritize technical precision and objective advice over aggressive sales tactics. Our bilingual agents provide personalized support to ensure every driver understands their specific policy architecture. We don't just provide a document; we offer a professional safety framework built on nearly 40 years of industry expertise. You can rely on our stable presence to guide you through every claim and policy renewal with total transparency.

Get Your Free Houston Car Insurance Quote Now

Protect your assets with a partner who understands the local market's unique challenges. We're ready to help you drive with complete confidence today.

The average annual cost for full coverage car insurance in Houston is projected to reach $3,150 by 2026. This figure represents a 4.5% increase from 2024 levels based on historical inflation data from the Bureau of Labor Statistics. Your specific rate depends on factors like your zip code in Harris County and your driving record. Drivers in high-traffic areas often pay 15% more than those in quieter suburbs.

Texas is an "at-fault" state for auto insurance, not a no-fault state. This means the driver responsible for the collision must pay for the other party's damages and medical expenses. Under Texas Transportation Code Chapter 601, the person who causes the accident bears the financial liability. Most drivers carry 30/60/25 liability limits to meet these legal obligations and avoid personal lawsuits. Drivers who want a complete overview of how these fault-based rules interact with statewide coverage requirements can reference our Texas auto insurance requirements and costs guide for 2026 for a structured breakdown of mandatory and optional protections.

Your car insurance covers flood damage only if you've purchased comprehensive coverage. Standard liability-only policies don't provide protection against environmental hazards like the 50 inches of rain seen during Hurricane Harvey. If your vehicle is submerged, comprehensive coverage pays for repairs or the actual cash value of the car minus your deductible. It's a critical addition for Houston residents given the city's flood history.

The minimum car insurance houston drivers must carry is a 30/60/25 liability policy. This includes $30,000 for bodily injury per person, $60,000 for total bodily injury per accident, and $25,000 for property damage. While these are the legal minimums set by the Texas Department of Insurance, they often don't cover the full cost of a major collision. We recommend higher limits to protect your personal assets from litigation.

You can obtain car insurance in Houston with a foreign driver's license through specialized carriers. Texas law allows international visitors and new residents to drive with a valid license from their home country for up to 90 days. Companies like AMCO help drivers navigate this transition by finding insurers that accept international driving records. You'll likely need to provide a passport and a certified copy of your foreign driving history.

You can lower your rates in Harris County by completing a Texas-approved defensive driving course to earn a 10% discount. Installing telematics devices that track safe driving habits can reduce premiums by up to 30% for qualifying motorists. Additionally, bundling your homeowners insurance in Texas and car insurance houston policies typically saves clients 15% annually. Maintaining a credit score above 700 also helps secure the most competitive regional rates available.

Driving without insurance in Houston results in a first-time fine between $175 and $350. Subsequent offenses can lead to fines up to $1,000 and the immediate suspension of your driver's license. The state may also impound your vehicle, costing you $20 per day in storage fees. You'll likely be required to file an SR-22 certificate for three years, which significantly increases your monthly premiums and limits your carrier options.

AMCO provides expert assistance with SR-22 filings for Houston drivers who've had their licenses suspended or revoked. We process these financial responsibility forms electronically with the Texas Department of Public Safety to ensure your driving privileges are restored quickly. Our team analyzes your specific situation to find the most cost-effective high-risk policy available. We've helped over 5,000 local drivers navigate the complex SR-22 process since our founding.